You might also like

- Delays and Disruption Hudson FormulaDocument2 pagesDelays and Disruption Hudson FormulaGordan CelarNo ratings yet

- ASPD 2 Scrapped FinalDocument115 pagesASPD 2 Scrapped FinaliqraNo ratings yet

- Indian Money MarketDocument79 pagesIndian Money MarketParth Shah100% (5)

- Hotel Budget TemplateDocument44 pagesHotel Budget TemplateClarisse30No ratings yet

- Trend Following Strategies in Commodity Markets and The Impact of FinancializationDocument71 pagesTrend Following Strategies in Commodity Markets and The Impact of FinancializationAlexandra100% (1)

- Case Analysis Sheet: Student Name Student SAP ID Student Roll NoDocument3 pagesCase Analysis Sheet: Student Name Student SAP ID Student Roll Nobharat bhushaNo ratings yet

- Pyramid DoorDocument15 pagesPyramid DoorEnnovy Tsu100% (1)

- NPA AnalysisDocument61 pagesNPA AnalysisSabyasachi PandaNo ratings yet

- Finding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesFrom EverandFinding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesNo ratings yet

- Dupont Case Write-UpDocument5 pagesDupont Case Write-UpRaghav AggrawalNo ratings yet

- Jagannath University Report on ICB Capital Management LimitedDocument18 pagesJagannath University Report on ICB Capital Management LimitedShifat ShahriarNo ratings yet

- PNBDocument20 pagesPNBShuchita BhutaniNo ratings yet

- Analyst Report Issued by IIFL (Company Update)Document16 pagesAnalyst Report Issued by IIFL (Company Update)Shyam SunderNo ratings yet

- Bajaj Finance Limited Q2 FY15 Presentation: 14 October 2014Document33 pagesBajaj Finance Limited Q2 FY15 Presentation: 14 October 2014adi99123No ratings yet

- Strategy & Results Update – Q2FY20Document58 pagesStrategy & Results Update – Q2FY20SCNo ratings yet

- Priti Executive SummaryDocument37 pagesPriti Executive SummaryPandey BarunNo ratings yet

- Northern Arc Capital - R-01072019Document10 pagesNorthern Arc Capital - R-01072019vaibhav khandelwalNo ratings yet

- Abans RAC OctDocument3 pagesAbans RAC OctGayashanPereraNo ratings yet

- Axis BankDocument17 pagesAxis BankSourabh GardeNo ratings yet

- Axis BankDocument17 pagesAxis BankSourabh GardeNo ratings yet

- Century Plyboards (India) Limited: Summary of Rated Instruments Instrument Rated Amount (In Crore) Rating ActionDocument8 pagesCentury Plyboards (India) Limited: Summary of Rated Instruments Instrument Rated Amount (In Crore) Rating ActionDeepakNo ratings yet

- HDFC Bank's Financial Performance During CovidDocument21 pagesHDFC Bank's Financial Performance During CovidSasi Samhitha KNo ratings yet

- About IndustryDocument36 pagesAbout IndustryHardik AgarwalNo ratings yet

- Commentary On Q3 FY19 Financial Results IDFCFIRST BankDocument8 pagesCommentary On Q3 FY19 Financial Results IDFCFIRST BankHimanshu GuptaNo ratings yet

- Aryadhan Financial Solutions - R - 18052018 PDFDocument7 pagesAryadhan Financial Solutions - R - 18052018 PDFCH Nitin TyagiNo ratings yet

- 2014 09 Clsa Conference PresentationDocument67 pages2014 09 Clsa Conference PresentationTara Ann CoelhoNo ratings yet

- Ocbc Ar2015 Full Report EnglishDocument232 pagesOcbc Ar2015 Full Report EnglishSassy TanNo ratings yet

- Upd ReprtDocument51 pagesUpd ReprtPankaj MadaanNo ratings yet

- Zinka Logistics Solutions - R-25092020Document8 pagesZinka Logistics Solutions - R-25092020Atiqur Rahman BarbhuiyaNo ratings yet

- Piramal Enterprises LimitedDocument10 pagesPiramal Enterprises LimitedDeepak VermaNo ratings yet

- Rationale - Nabil Bank Limited - January 2022Document6 pagesRationale - Nabil Bank Limited - January 2022Sumit RauniyarNo ratings yet

- Chaitanya Godavari Grameena Bank - Economic Value AddDocument3 pagesChaitanya Godavari Grameena Bank - Economic Value AddPhaniee Kumar VicharapuNo ratings yet

- Ratio Analysis of Bank Alfalah LimitedDocument22 pagesRatio Analysis of Bank Alfalah LimitedAnonymous uDP6XEHs100% (1)

- Banking Finance and Insurance: A Report On Financial Analysis of IDBI BankDocument8 pagesBanking Finance and Insurance: A Report On Financial Analysis of IDBI BankRaven FormourneNo ratings yet

- Happy ForgingsDocument7 pagesHappy ForgingsArshChandraNo ratings yet

- Edelweiss Financial Services Limited: Summary of Rated InstrumentsDocument9 pagesEdelweiss Financial Services Limited: Summary of Rated Instrumentslekha1997No ratings yet

- Goal - A Process of Continuous Improvement - Eliyahu Goldratt (Qwerty80)Document43 pagesGoal - A Process of Continuous Improvement - Eliyahu Goldratt (Qwerty80)Girish GaykawadNo ratings yet

- Uttam WealthDocument22 pagesUttam WealthMOHIT KUMARNo ratings yet

- Financial Analysis of Novatex Customer Performance and ProjectionsDocument3 pagesFinancial Analysis of Novatex Customer Performance and Projectionstalha alamNo ratings yet

- Suggested Answer of Case Study (CS)Document19 pagesSuggested Answer of Case Study (CS)FarhadNo ratings yet

- Internship Report: Bank Alfalah LimitedDocument54 pagesInternship Report: Bank Alfalah LimitedBadshah SalamutNo ratings yet

- Spandana Sphoorty Financial Limited IPO Note-201908050934443167041Document13 pagesSpandana Sphoorty Financial Limited IPO Note-201908050934443167041tanmayNo ratings yet

- 4.1. Background and History: Principal ActivitiesDocument4 pages4.1. Background and History: Principal ActivitiesMujtaba NaqviNo ratings yet

- Annapurna Finance R 10092018Document10 pagesAnnapurna Finance R 10092018NIBOX MEDIA CENTERNo ratings yet

- Financial ProfileDocument1 pageFinancial ProfileSuresh KumarNo ratings yet

- N BP Annual Report 2021Document406 pagesN BP Annual Report 2021ProNo ratings yet

- 247 Customer Private LimitedDocument7 pages247 Customer Private Limitednayabrasul208No ratings yet

- Prime Banks Credit CardDocument9 pagesPrime Banks Credit CardIsmat Jerin ChetonaNo ratings yet

- The Will to Go Beyond: Faysal Bank's 2010 Annual ReportDocument541 pagesThe Will to Go Beyond: Faysal Bank's 2010 Annual ReportAnnie DollNo ratings yet

- DCB Bank Buy Emkay ResearchDocument23 pagesDCB Bank Buy Emkay ResearchGreyFoolNo ratings yet

- Sakthi Finance Limited R 20022020Document9 pagesSakthi Finance Limited R 20022020Elan ChelianNo ratings yet

- Finance For Managers Report - BillDocument13 pagesFinance For Managers Report - BillDavid Luko ChifwaloNo ratings yet

- Internship 1-2Document19 pagesInternship 1-2Unni sajeevNo ratings yet

- Repco Home Finance: Growth Regains Momentum Asset Quality On Strong TurfDocument13 pagesRepco Home Finance: Growth Regains Momentum Asset Quality On Strong TurfFischerNo ratings yet

- Microfinance Private LimitedDocument5 pagesMicrofinance Private LimitedsantoshbsantuNo ratings yet

- Price Waterhouse & Co Chartered Accountants LLPDocument8 pagesPrice Waterhouse & Co Chartered Accountants LLPSuraj KumarNo ratings yet

- Standard Chartered Bank Pakistan Announces Q3 2021 ResultsDocument3 pagesStandard Chartered Bank Pakistan Announces Q3 2021 ResultsAaehan AhmedNo ratings yet

- FCH - Press Release On Rating Upgrade (04-11-2020)Document4 pagesFCH - Press Release On Rating Upgrade (04-11-2020)BhanumathieNo ratings yet

- Canara Bank to Expand Overseas Branch NetworkDocument4 pagesCanara Bank to Expand Overseas Branch NetworkShruti TalikotiNo ratings yet

- Ratings reaffirmed for Nepal Bangladesh Bank LimitedDocument4 pagesRatings reaffirmed for Nepal Bangladesh Bank LimitedBhupEndra AdhikaRiNo ratings yet

- Introduction of BanksDocument4 pagesIntroduction of BanksNoman AnsariNo ratings yet

- Kotak Mahindra Bank Q1 FY18 Earnings Call SummaryDocument24 pagesKotak Mahindra Bank Q1 FY18 Earnings Call Summarydivya mNo ratings yet

- Crisil Yearbook On The Indian Debt Market 2015.unlockedDocument114 pagesCrisil Yearbook On The Indian Debt Market 2015.unlockedPRATIK JAINNo ratings yet

- Barbeque Nation Hospitality LimitedDocument7 pagesBarbeque Nation Hospitality Limitednayabrasul208No ratings yet

- Bewakoof Brands - Financial Analysis DataDocument8 pagesBewakoof Brands - Financial Analysis DataDimple SundraniNo ratings yet

- Oxyzo Annual Report FY 2021 2022Document171 pagesOxyzo Annual Report FY 2021 2022Saubhagya SuriNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- Vitamin D's role in chronic heart failureDocument8 pagesVitamin D's role in chronic heart failureAli AkberNo ratings yet

- Quant Session 2 (CLASSROOM) - 75 Questions - Numbers and Inequalities - SOLUTIONS PDFDocument60 pagesQuant Session 2 (CLASSROOM) - 75 Questions - Numbers and Inequalities - SOLUTIONS PDFamey thakurNo ratings yet

- Prospectus 2013Document96 pagesProspectus 2013Lindsay AbbottNo ratings yet

- Facebook IPO 2012 Prospectus S1 PDFDocument198 pagesFacebook IPO 2012 Prospectus S1 PDFAli AkberNo ratings yet

- DefaultDocument1 pageDefaultAli AkberNo ratings yet

- Walmart Vs AmazonDocument188 pagesWalmart Vs AmazonRYENA111No ratings yet

- Oregon Public Employees Retirement System Aug. 2012 Board Meeting PacketDocument138 pagesOregon Public Employees Retirement System Aug. 2012 Board Meeting PacketStatesman JournalNo ratings yet

- QT Project ReportDocument14 pagesQT Project ReportDevNo ratings yet

- Strategic ManagementDocument17 pagesStrategic ManagementZaib NawazNo ratings yet

- Elasticity of Demand and Total RevenueDocument2 pagesElasticity of Demand and Total RevenueJecka DuyagNo ratings yet

- Stock Valuation: 1 Fundamental Criteria (Fair Value)Document7 pagesStock Valuation: 1 Fundamental Criteria (Fair Value)Siti RachmahNo ratings yet

- Adjusting Journal EntriesDocument11 pagesAdjusting Journal EntriesKatrina RomasantaNo ratings yet

- PetMeds Analysis 2Document10 pagesPetMeds Analysis 2Марго КоваленкоNo ratings yet

- Marketing Research of MiloDocument5 pagesMarketing Research of MiloAsha100% (1)

- Just For Feet Working Capital Management Case Study - Current Ratio, Quick Ratio, Inventory Turnover AnalysisDocument3 pagesJust For Feet Working Capital Management Case Study - Current Ratio, Quick Ratio, Inventory Turnover AnalysisAshim KarNo ratings yet

- Destination Branding Framework: A Theoretical ApproachDocument11 pagesDestination Branding Framework: A Theoretical ApproachAndreea BocaNo ratings yet

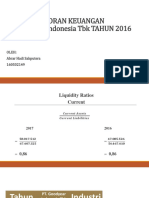

- Analisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Document34 pagesAnalisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Tri AmbarNo ratings yet

- Evaluation of Change in Credit PolicyDocument5 pagesEvaluation of Change in Credit PolicyJhunorlando DisonoNo ratings yet

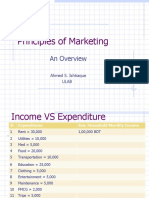

- Principals of Marketing BUS 206Document33 pagesPrincipals of Marketing BUS 206Sahal Bin SaadNo ratings yet

- Saqib MKT 623 Final DraftDocument5 pagesSaqib MKT 623 Final Draftashikur rahmanNo ratings yet

- Rectified Business Project PDFDocument8 pagesRectified Business Project PDFPrem Kumar KarnNo ratings yet

- Market Segmentation and Target MarketDocument2 pagesMarket Segmentation and Target MarketMikaela CatimbangNo ratings yet

- Presented by Minal Neswankar Jivika Thakur Preeti WaghmodeDocument21 pagesPresented by Minal Neswankar Jivika Thakur Preeti WaghmodeJivika ThakurNo ratings yet

- 1.4 Risk+Management:+A+Helicopter+View+风险管理:从一个宏观、全局的角度看Document17 pages1.4 Risk+Management:+A+Helicopter+View+风险管理:从一个宏观、全局的角度看James JiangNo ratings yet

- Managing Brands OvertimeDocument8 pagesManaging Brands OvertimesrirammaliNo ratings yet

- Salary Accounting at Garment CompanyDocument81 pagesSalary Accounting at Garment CompanyPhước NguyễnNo ratings yet

- PRINCIPLES OF MARKETING PPDocument77 pagesPRINCIPLES OF MARKETING PPAvegail Ocampo TorresNo ratings yet