You might also like

- Sold Short: Uncovering Deception in the MarketsFrom EverandSold Short: Uncovering Deception in the MarketsRating: 3.5 out of 5 stars3.5/5 (3)

- Leading IndicatorDocument26 pagesLeading IndicatoralexanderNo ratings yet

- The Basics Of The Long Ratio BackspreadDocument3 pagesThe Basics Of The Long Ratio BackspreadSpringbok747No ratings yet

- CONOCOPHILLIPS 10-K (Annual Reports) 2009-02-25Document324 pagesCONOCOPHILLIPS 10-K (Annual Reports) 2009-02-25http://secwatch.com100% (2)

- Energy Market Manipulation: Definition, Diagnosis, and DeterrenceDocument20 pagesEnergy Market Manipulation: Definition, Diagnosis, and DeterrenceGlobalEconNo ratings yet

- Pump Polaris SeriesDocument47 pagesPump Polaris SeriesDANIZACHNo ratings yet

- Ewco Alves: NEWCO/OIC Cast Valve Operation & Maintenance ManualDocument22 pagesEwco Alves: NEWCO/OIC Cast Valve Operation & Maintenance ManualSebastian Jerez UrquietaNo ratings yet

- Trial Lecture LNG Refrigeration ProcessesDocument37 pagesTrial Lecture LNG Refrigeration Processesoliver9191No ratings yet

- Chapter1 - Drilling Rig and SystemsDocument166 pagesChapter1 - Drilling Rig and Systemsm.kooshan20100% (1)

- The Pivot Point Squeeze: PurpleDocument8 pagesThe Pivot Point Squeeze: Purpledephie08No ratings yet

- Dynamic Measuremen Training LPGDocument58 pagesDynamic Measuremen Training LPGRomandon RomandonNo ratings yet

- 1500HP FAST MOVING DRILLING RIG TECHNICAL SPECIFICATIONDocument45 pages1500HP FAST MOVING DRILLING RIG TECHNICAL SPECIFICATIONyou seef100% (1)

- Slings-Chains+wir RopesDocument30 pagesSlings-Chains+wir RopestonyNo ratings yet

- ASME Oil Selection For Precision Ball Bearing F2161.5237 1Document15 pagesASME Oil Selection For Precision Ball Bearing F2161.5237 1vyhtran4731100% (1)

- PENG 305 LECTURE NOTES ON DRILLSTRING COMPONENTSDocument30 pagesPENG 305 LECTURE NOTES ON DRILLSTRING COMPONENTSkwesimark100% (1)

- CW ReportDocument6 pagesCW ReportZainab SarfrazNo ratings yet

- Foreign Currency Exposure and Risk ManagementDocument48 pagesForeign Currency Exposure and Risk ManagementChetankumar ChaudhariNo ratings yet

- Derivatives and Commodity ExchangesDocument53 pagesDerivatives and Commodity ExchangesMonika GoelNo ratings yet

- New Microsoft Word DocumentDocument6 pagesNew Microsoft Word DocumentCharmi SatraNo ratings yet

- China Aviation Oil Case StudyDocument11 pagesChina Aviation Oil Case StudyDrake RamoorayNo ratings yet

- Foreign Exchange Risk ManagementDocument5 pagesForeign Exchange Risk Managementpriya JNo ratings yet

- Introduction To Hedging (Notes)Document8 pagesIntroduction To Hedging (Notes)t6s1z7No ratings yet

- WLH Finance CompilationDocument58 pagesWLH Finance CompilationSandhya S 17240No ratings yet

- Foreign Exchange Risk ManagementDocument32 pagesForeign Exchange Risk Managementramagarwal1No ratings yet

- Foreign Exchange Risk Management - International Financial Environment, International Business - EduRev NotesDocument8 pagesForeign Exchange Risk Management - International Financial Environment, International Business - EduRev Notesswatisin93No ratings yet

- Corporate Risk ManagementDocument6 pagesCorporate Risk ManagementViral DesaiNo ratings yet

- Glossary Content M1C4Document10 pagesGlossary Content M1C4Abdullah Al MuttakiNo ratings yet

- 4 March Capstone ProjectDocument28 pages4 March Capstone ProjectCarl BerryNo ratings yet

- The Need For Derivatives: WORK SHEET - Financial DerivativesDocument5 pagesThe Need For Derivatives: WORK SHEET - Financial DerivativesBhavesh RathiNo ratings yet

- PDD - Questionnaire Rajendra - ShahaneDocument2 pagesPDD - Questionnaire Rajendra - ShahaneRRSNo ratings yet

- 9 Derivatives 16 5 12 120819125650 Phpapp02Document21 pages9 Derivatives 16 5 12 120819125650 Phpapp02Surekha AmmuNo ratings yet

- A Proposal For Special Studies (Finance) : Project TitleDocument9 pagesA Proposal For Special Studies (Finance) : Project TitleJay SorathiyaNo ratings yet

- Derivatives Chapter 2 (Introduction To Futures)Document45 pagesDerivatives Chapter 2 (Introduction To Futures)zaryNo ratings yet

- Origin of All Derivatives: Risk Is The Only Constant, Uncertainty Is The Only CertaintyDocument36 pagesOrigin of All Derivatives: Risk Is The Only Constant, Uncertainty Is The Only CertaintyChinmay ShirsatNo ratings yet

- International Financial Management Project Hedging Risk with DerivativesDocument11 pagesInternational Financial Management Project Hedging Risk with DerivativesChetanNo ratings yet

- Topic 2 - Derivatives and Risk ManagementDocument35 pagesTopic 2 - Derivatives and Risk Managementjulius erwin espejoNo ratings yet

- Derivatives Assignment 1Document15 pagesDerivatives Assignment 1ashoo khosla100% (1)

- Economic ExposureDocument7 pagesEconomic ExposureChi NguyenNo ratings yet

- DerivativesDocument9 pagesDerivativesrududu duduNo ratings yet

- Literature Review Currency HedgingDocument8 pagesLiterature Review Currency Hedgingfvf8gc78100% (1)

- Điền từDocument4 pagesĐiền từMai ĐàoNo ratings yet

- Derivatives Lecture Futures ForwardsDocument32 pagesDerivatives Lecture Futures ForwardsavirgNo ratings yet

- Commodity Futures Functioning: Student's Roll No: A16 Student's Reg. No: 11906130Document7 pagesCommodity Futures Functioning: Student's Roll No: A16 Student's Reg. No: 11906130Prateek SehgalNo ratings yet

- Derivatives, Options and Furtures Oct2010Document64 pagesDerivatives, Options and Furtures Oct2010Farah NawazNo ratings yet

- Futures Contracts FinalDocument11 pagesFutures Contracts Finalravi_nyseNo ratings yet

- CH 24Document68 pagesCH 24Rachel LeachonNo ratings yet

- CH 11Document35 pagesCH 11api-241660930No ratings yet

- Corv MaterialDocument9 pagesCorv MaterialEmiraslan MhrrovNo ratings yet

- SN Acme1Document10 pagesSN Acme1Tharun RNo ratings yet

- 8.forwards and FuturesDocument73 pages8.forwards and Futuresfahd98No ratings yet

- Foreign Exchange Exposures - IFMDocument7 pagesForeign Exchange Exposures - IFMDivya SindheyNo ratings yet

- Bhavesh Work Sheet 01 - FDDocument8 pagesBhavesh Work Sheet 01 - FDBhavesh RathiNo ratings yet

- Dr. Sarva's Equity Derivative Course AssignmentDocument7 pagesDr. Sarva's Equity Derivative Course AssignmentPrateek SehgalNo ratings yet

- Derivatives: Futures, Options and Swaps: Transfer Risk From One Person or Firm To AnotherDocument13 pagesDerivatives: Futures, Options and Swaps: Transfer Risk From One Person or Firm To AnothershubhamNo ratings yet

- Capital MarketDocument10 pagesCapital MarketEduar GranadaNo ratings yet

- Derivative MarketsDocument4 pagesDerivative MarketsMorelate KupfurwaNo ratings yet

- Investment Risk APADocument10 pagesInvestment Risk APAMuhammad Ramiz AminNo ratings yet

- Intro to Derivatives MarketsDocument14 pagesIntro to Derivatives MarketsAryaom DasNo ratings yet

- Deepthi - Assignment-Finanacial Fututures PDFDocument4 pagesDeepthi - Assignment-Finanacial Fututures PDFkuldeep singhNo ratings yet

- Long Term Sources of FundsDocument7 pagesLong Term Sources of FundsushaNo ratings yet

- Pyrolysis 1Document3 pagesPyrolysis 1georgiadisgNo ratings yet

- EAC Site Visit 7th April 7Document1 pageEAC Site Visit 7th April 7georgiadisgNo ratings yet

- Hydro Treating CompleteDocument19 pagesHydro Treating CompleteFaiq Ahmad Khan100% (3)

- Cost EstimationDocument29 pagesCost Estimationgeorgiadisg100% (4)

- LNG Project in CyprusDocument8 pagesLNG Project in CyprusgeorgiadisgNo ratings yet

- Approaches To Simulating Distillation and Absorption: Figure 1 Ancient Greek StillDocument2 pagesApproaches To Simulating Distillation and Absorption: Figure 1 Ancient Greek StillVictor VazquezNo ratings yet

- Lecture1 - Introduction To The Oil and Gas IndustryDocument118 pagesLecture1 - Introduction To The Oil and Gas IndustrygeorgiadisgNo ratings yet

- Pyrolysis 1Document3 pagesPyrolysis 1georgiadisgNo ratings yet

- EAC Site Visit 7th April 7Document1 pageEAC Site Visit 7th April 7georgiadisgNo ratings yet

- Hydro Treating CompleteDocument7 pagesHydro Treating CompletegeorgiadisgNo ratings yet

- Approaches To Simulating Distillation and Absorption: Figure 1 Ancient Greek StillDocument2 pagesApproaches To Simulating Distillation and Absorption: Figure 1 Ancient Greek StillVictor VazquezNo ratings yet

- Pyrolysis 1st Report Sep2017 R1aDocument10 pagesPyrolysis 1st Report Sep2017 R1ageorgiadisgNo ratings yet

- Approaches To Simulating Distillation and Absorption: Figure 1 Ancient Greek StillDocument2 pagesApproaches To Simulating Distillation and Absorption: Figure 1 Ancient Greek StillVictor VazquezNo ratings yet

- Basic Operations Distillation & Filtration: Dr. George Georgiadis PHDDocument71 pagesBasic Operations Distillation & Filtration: Dr. George Georgiadis PHDgeorgiadisgNo ratings yet

- FPSO IntroductionDocument121 pagesFPSO Introductiongeorgiadisg100% (2)

- Cost Estimation and ProjectsDocument45 pagesCost Estimation and ProjectsgeorgiadisgNo ratings yet

- DistillationDocument2 pagesDistillationSk. Salahuddin AhammadNo ratings yet

- Process Equipment Cost Estimation PDFDocument78 pagesProcess Equipment Cost Estimation PDFBrenda Davis100% (1)

- Oil Tankers: An Overview of Major Factors Affecting Design, Construction, Pricing and ContractsDocument10 pagesOil Tankers: An Overview of Major Factors Affecting Design, Construction, Pricing and Contractsgeorgiadisg100% (1)

- Prospect evaluation, resource assessment and risking key parametersDocument40 pagesProspect evaluation, resource assessment and risking key parametersgeorgiadisgNo ratings yet

- UOP - Cat PaperDocument0 pagesUOP - Cat Paperbinapaniki6520No ratings yet

- Bitumen ManufactureDocument46 pagesBitumen Manufacturegeorgiadisg100% (2)

- Offshore - Introduction LayoutDocument131 pagesOffshore - Introduction LayoutgeorgiadisgNo ratings yet

- Natural GasDocument25 pagesNatural GasgeorgiadisgNo ratings yet

- Good Operating Techniques Improve Coker YieldDocument2 pagesGood Operating Techniques Improve Coker YieldgeorgiadisgNo ratings yet

- 5 Mass TransferDocument85 pages5 Mass TransfergeorgiadisgNo ratings yet

- Introduction To LNGDocument27 pagesIntroduction To LNGdensandsNo ratings yet

- OG071 Hydrocarbon Production OperationsDocument4 pagesOG071 Hydrocarbon Production OperationsgeorgiadisgNo ratings yet

- Mutiport SpecificationDocument9 pagesMutiport SpecificationgeorgiadisgNo ratings yet

- Drilling TchnologiesDocument42 pagesDrilling TchnologiesgeorgiadisgNo ratings yet

- CH 10 RevisedDocument3 pagesCH 10 RevisedRestu AnggrainiNo ratings yet

- Securitisation Primer and Analysis of A Financial Technique: Andrea Durante November 2010Document25 pagesSecuritisation Primer and Analysis of A Financial Technique: Andrea Durante November 2010Emmanuele Orospies SpadaroNo ratings yet

- SCBDocument22 pagesSCBFazeela RanaNo ratings yet

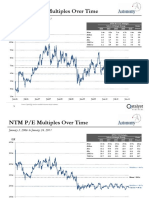

- NTM Revenue Multiples Over Time: Mean 6.8x, 75th Perc 7.6xDocument3 pagesNTM Revenue Multiples Over Time: Mean 6.8x, 75th Perc 7.6xmittleNo ratings yet

- Carlyle Asia Real Estate Partners II, L.P.Document5 pagesCarlyle Asia Real Estate Partners II, L.P.huangyupengNo ratings yet

- Individual Assignment Summer 2019Document3 pagesIndividual Assignment Summer 2019Natalie Godgotme RoseNo ratings yet

- Accounting standards and conceptual frameworkDocument11 pagesAccounting standards and conceptual frameworkAnas Aloyodan60% (5)

- Omkar Speciality ChemicalsDocument16 pagesOmkar Speciality Chemicalssiddhu444No ratings yet

- Wall Street Verdicts Settlements 1Document193 pagesWall Street Verdicts Settlements 1locopr1No ratings yet

- Wohl Cease & DesistDocument35 pagesWohl Cease & DesistTBPInvictus100% (2)

- Eco Wrap SBIDocument3 pagesEco Wrap SBIVaibhav BhardwajNo ratings yet

- What is a Payment System? Key Components, Risks and Major Instruments in the PhilippinesDocument19 pagesWhat is a Payment System? Key Components, Risks and Major Instruments in the PhilippinesMarta MeaNo ratings yet

- D&L Investor Deck 2018 05 30 (MAY 2018)Document55 pagesD&L Investor Deck 2018 05 30 (MAY 2018)zeebugNo ratings yet

- Ejaz Naseer NBP Reprort 2018Document58 pagesEjaz Naseer NBP Reprort 2018Tayyab ali gardaziNo ratings yet

- Start Over, Finish Rich by David Bach - ExcerptDocument20 pagesStart Over, Finish Rich by David Bach - ExcerptCrown Publishing Group36% (14)

- ACCA Paper F9 Mnemonics Revision (Sample Download)Document37 pagesACCA Paper F9 Mnemonics Revision (Sample Download)accountancylad100% (3)

- Performance Comparison of Midcap Mutual FundsDocument103 pagesPerformance Comparison of Midcap Mutual Fundsswatisabherwal100% (3)

- Terms and Conditions EToroDocument42 pagesTerms and Conditions EToroZhess BugNo ratings yet

- Ambit Research Report Turnaround StocksDocument76 pagesAmbit Research Report Turnaround StocksArunddhuti RayNo ratings yet

- What Hedge Funds Really Do An Introduction To Portfolio ManagementDocument148 pagesWhat Hedge Funds Really Do An Introduction To Portfolio ManagementtheEarth100% (8)

- FINAL EXAM TITLEDocument6 pagesFINAL EXAM TITLEPsyche Rizsavi Fontanilla-MamadraNo ratings yet

- Articles of Incorporation of ABC CorporationDocument6 pagesArticles of Incorporation of ABC CorporationvivivioletteNo ratings yet

- 11 Fraud Detection Prevention and Investigation J Aquino Sec PDFDocument77 pages11 Fraud Detection Prevention and Investigation J Aquino Sec PDFLe BlancNo ratings yet

- Darvas Technical Filter Plus PDFDocument32 pagesDarvas Technical Filter Plus PDFAlvinNo ratings yet

- Price Is Everything Fundamental AnalysisDocument16 pagesPrice Is Everything Fundamental AnalysisHeretic87100% (1)

- Procedure For Pricing Bermudans and Callable SwapsDocument18 pagesProcedure For Pricing Bermudans and Callable SwapsalexandergirNo ratings yet

- Best Applicant MemorialDocument44 pagesBest Applicant MemorialPriyanka Priyadarshini0% (1)

- Report - Inefficiency in Operations of CSE, Sri LankaDocument9 pagesReport - Inefficiency in Operations of CSE, Sri LankaDinesh ThevaranjanNo ratings yet

- F9D2Document30 pagesF9D2mysticsoulNo ratings yet