You might also like

- The Four Walls: Live Like the Wind, Free, Without HindrancesFrom EverandThe Four Walls: Live Like the Wind, Free, Without HindrancesRating: 5 out of 5 stars5/5 (1)

- Amalgamation of CompaniesDocument8 pagesAmalgamation of CompaniesVikram NaniNo ratings yet

- The Indian Partnership Act, 1932Document17 pagesThe Indian Partnership Act, 1932Engineer100% (1)

- Part II Audit ProjecDocument36 pagesPart II Audit ProjecSagar Zine100% (1)

- Project On HDFC BankDocument67 pagesProject On HDFC BankAarti YadavNo ratings yet

- NRI Banking StudyDocument55 pagesNRI Banking StudyJayanti KappalNo ratings yet

- Impact of GST On WholesellerDocument59 pagesImpact of GST On Wholesellermovie latest kadamNo ratings yet

- Difference Between Cash Flow and Fund Flow StatementDocument3 pagesDifference Between Cash Flow and Fund Flow StatementAtul ManiNo ratings yet

- Money Market in India: A Project Report ONDocument35 pagesMoney Market in India: A Project Report ONLovely SharmaNo ratings yet

- Depository System in IndiaDocument10 pagesDepository System in Indiababloorabidwolverine100% (2)

- Innovations in InsuranceDocument47 pagesInnovations in InsuranceDouglas StoneNo ratings yet

- A Presentation On HR Policies : Singh Ankit Jitendra Sristi Biswas Vivek KumarDocument9 pagesA Presentation On HR Policies : Singh Ankit Jitendra Sristi Biswas Vivek KumarAnkit SinghNo ratings yet

- A Case Study On The Corporate Social Responsibility of The Selected Indian CompaniesDocument55 pagesA Case Study On The Corporate Social Responsibility of The Selected Indian CompaniesRohit KerkarNo ratings yet

- Leadership Styles in BankingDocument17 pagesLeadership Styles in BankingPriyanshi TalesraNo ratings yet

- ON "A Study On Investment Pattern of Women Investors In: DissertationDocument50 pagesON "A Study On Investment Pattern of Women Investors In: DissertationKrishna Sharma100% (1)

- Project Report On Reliance MoneyDocument88 pagesProject Report On Reliance MoneyShivani100% (1)

- Mergers and Acquisitions DeterminantsDocument148 pagesMergers and Acquisitions Determinantsraunak_19871981No ratings yet

- MAIN PPT Stock Exchange of India - pptmATDocument42 pagesMAIN PPT Stock Exchange of India - pptmATAnkit Jain100% (1)

- Amalgamation of Firms ProjectDocument5 pagesAmalgamation of Firms ProjectkalaswamiNo ratings yet

- Allahabad BankDocument103 pagesAllahabad BankPiyush Gehlot0% (1)

- Role of Banks in Working Capital ManagementDocument59 pagesRole of Banks in Working Capital Managementswati29mishra100% (6)

- Unit - 3 Credit SyndicationDocument7 pagesUnit - 3 Credit SyndicationPraveen KumarNo ratings yet

- Black Book 05Document68 pagesBlack Book 05vishal vhatkarNo ratings yet

- Bombay Mercantile Co-Operative Bank LTDDocument78 pagesBombay Mercantile Co-Operative Bank LTDaadil shaikhNo ratings yet

- Role and Importance of COPRA, 1986Document11 pagesRole and Importance of COPRA, 1986Mugdha Tomar100% (1)

- Project ReportDocument53 pagesProject ReportAbhishek MishraNo ratings yet

- Advertising, Sales, Promotion, and Public RelationsDocument24 pagesAdvertising, Sales, Promotion, and Public RelationsShaukat Ali KhanNo ratings yet

- Assessing Tax for Firms and PartnershipsDocument18 pagesAssessing Tax for Firms and PartnershipsOrko AbirNo ratings yet

- Corporate GovernanceDocument50 pagesCorporate GovernanceYash BiyaniNo ratings yet

- Avinash Purohit FINACIAL REPORTDocument93 pagesAvinash Purohit FINACIAL REPORTAvi PurohitNo ratings yet

- Taxation of Charitable Trusts and OrganizationsDocument50 pagesTaxation of Charitable Trusts and OrganizationsDhrutiNo ratings yet

- A Study On Receivable Management & Its ImpactDocument70 pagesA Study On Receivable Management & Its Impactlmbhagya100% (2)

- Merchant Banking in IndiaDocument61 pagesMerchant Banking in IndiarimpyanitaNo ratings yet

- Management of Working CapitalDocument9 pagesManagement of Working CapitalKushal KaushikNo ratings yet

- Working Capital at SbiDocument65 pagesWorking Capital at SbiRahul ShrivastavaNo ratings yet

- Perception of Customers Shriram Transport Finance PROJECT REPORT MBA MARKETINGDocument70 pagesPerception of Customers Shriram Transport Finance PROJECT REPORT MBA MARKETINGShumayla Khan100% (1)

- Leverage Analysis of Maruti Suzuki India LtdDocument47 pagesLeverage Analysis of Maruti Suzuki India LtdRavi ShankarNo ratings yet

- CRM Complete ProjectDocument61 pagesCRM Complete ProjectPratik GosaviNo ratings yet

- Banking Sector Reforms in IndiaDocument8 pagesBanking Sector Reforms in IndiaJashan Singh GillNo ratings yet

- Sbi Mutual FundDocument44 pagesSbi Mutual FundUtkarsh NolkhaNo ratings yet

- Loans & Advances Study at Ujjivan BankDocument75 pagesLoans & Advances Study at Ujjivan Banksachin mohanNo ratings yet

- Name: Sangeeta Kumari ROLL NO:1051-15-407-085 T0Pic: Compartatives Study On Ulip'S in The Insurance MarketDocument68 pagesName: Sangeeta Kumari ROLL NO:1051-15-407-085 T0Pic: Compartatives Study On Ulip'S in The Insurance Marketkavya srivastavaNo ratings yet

- Consumerism: "It Is The Shame of The Total Marketing Concept." - Peter F. DuckerDocument20 pagesConsumerism: "It Is The Shame of The Total Marketing Concept." - Peter F. DuckerdfchandNo ratings yet

- Importance of Insurance To ConsumersDocument7 pagesImportance of Insurance To ConsumersChandan Srivastava0% (1)

- A Study On Awareness of Merchant Banking PDFDocument56 pagesA Study On Awareness of Merchant Banking PDFShweta SharmaNo ratings yet

- Banking LawDocument51 pagesBanking LawAnanya Bunny MohapatraNo ratings yet

- Uma Industry Assets and Liabilities MGTDocument80 pagesUma Industry Assets and Liabilities MGTKirthi KshatriyasNo ratings yet

- NBFC FinalDocument100 pagesNBFC FinalDivyangi WaliaNo ratings yet

- Axix Bank Cash MangementDocument21 pagesAxix Bank Cash MangementMd WasimNo ratings yet

- Ibc FinalsDocument51 pagesIbc FinalsMALKANI DISHA DEEPAKNo ratings yet

- Full Project NewDocument66 pagesFull Project NewSandra sunnyNo ratings yet

- Abhishek Kumar IsbsDocument45 pagesAbhishek Kumar IsbsAbhishek Kumar100% (1)

- Customer Satisfaction Insurance Products of ICICI PrudentialDocument71 pagesCustomer Satisfaction Insurance Products of ICICI Prudentialkarthik_shabby15No ratings yet

- A Study On Deposit Mobilization With Reference To Indian Overseas Bank, Velachery byDocument44 pagesA Study On Deposit Mobilization With Reference To Indian Overseas Bank, Velachery byvinoth_17588No ratings yet

- Project On Dividend PolicyDocument50 pagesProject On Dividend PolicyMukesh Manwani100% (3)

- Chapter - 1: Meaning and DefinitionDocument12 pagesChapter - 1: Meaning and DefinitionShilpa S RaoNo ratings yet

- Amalgmation, Absorbtion, External ReconstructionDocument9 pagesAmalgmation, Absorbtion, External Reconstructionpijiyo78No ratings yet

- AmalgamationDocument41 pagesAmalgamationZooNo ratings yet

- 5) Amalgamation of CompaniesDocument82 pages5) Amalgamation of CompaniesShiv ShivNo ratings yet

- 74719bos60485 Inter p1 cp13Document92 pages74719bos60485 Inter p1 cp13Aniruddh SoniNo ratings yet

- EDUCATION Success solutions care mission vision services frameworkDocument7 pagesEDUCATION Success solutions care mission vision services frameworkkhuranaamanpreet7gmailcomNo ratings yet

- Special Classes for 1st to MBA with Crash Courses & Individual AttentionDocument1 pageSpecial Classes for 1st to MBA with Crash Courses & Individual Attentionkhuranaamanpreet7gmailcomNo ratings yet

- Aman Unit 4Document81 pagesAman Unit 4khuranaamanpreet7gmailcomNo ratings yet

- Aman Unit 4Document50 pagesAman Unit 4khuranaamanpreet7gmailcomNo ratings yet

- Summer Training ReportDocument21 pagesSummer Training Reportkhuranaamanpreet7gmailcomNo ratings yet

- Collective BargainingDocument27 pagesCollective Bargainingkhuranaamanpreet7gmailcomNo ratings yet

- Long Division Step-by-Step SolutionsDocument2 pagesLong Division Step-by-Step Solutionskhuranaamanpreet7gmailcomNo ratings yet

- Payment of Gratuity Act 1972Document15 pagesPayment of Gratuity Act 1972khuranaamanpreet7gmailcomNo ratings yet

- Trade UnionDocument8 pagesTrade Unionkhuranaamanpreet7gmailcomNo ratings yet

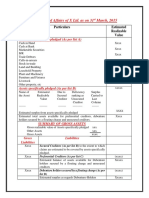

- Statement of AffairsDocument2 pagesStatement of Affairskhuranaamanpreet7gmailcom100% (1)

- Statement of Affairs-1Document5 pagesStatement of Affairs-1khuranaamanpreet7gmailcomNo ratings yet

- Holding and Subsidiary Companies Consolidated Balance SheetDocument33 pagesHolding and Subsidiary Companies Consolidated Balance Sheetkhuranaamanpreet7gmailcomNo ratings yet

- 4 Memorandum of AssociationDocument38 pages4 Memorandum of Associationkhuranaamanpreet7gmailcom100% (1)

- IFRS Study MaterialDocument687 pagesIFRS Study MaterialBin Saadun78% (9)

- ReSA CPA Review Batch 42 Audit Problems SolutionsDocument12 pagesReSA CPA Review Batch 42 Audit Problems SolutionsMellaniNo ratings yet

- Corporate AccountingDocument111 pagesCorporate AccountingYashas KrishnaNo ratings yet

- AFARDocument41 pagesAFARAlican, JerhamelNo ratings yet

- PFRS For Small Entities 1 PDFDocument43 pagesPFRS For Small Entities 1 PDFRojohn ValenzuelaNo ratings yet

- Business Combination: Expense ImmediatelyDocument7 pagesBusiness Combination: Expense ImmediatelyKristel SumabatNo ratings yet

- Change in Profit Sharing Ratio Among The Existing PartnersDocument15 pagesChange in Profit Sharing Ratio Among The Existing Partnersvajoj90546No ratings yet

- Vertical Analysis of Financial Statements - Pepsi V CokeDocument2 pagesVertical Analysis of Financial Statements - Pepsi V CokeCarneades33% (3)

- Chapter 1 - Test Bank Advanced Accounting BakerDocument12 pagesChapter 1 - Test Bank Advanced Accounting Bakergilli1tr100% (4)

- Afar BuscombDocument22 pagesAfar BuscombMo Mindalano MandanganNo ratings yet

- ADV ACC TBch05Document21 pagesADV ACC TBch05hassan nassereddineNo ratings yet

- FMGT 7121 Module 6 - 8th EditionDocument11 pagesFMGT 7121 Module 6 - 8th EditionhilaryNo ratings yet

- Audit of Cash and ReceivablesDocument21 pagesAudit of Cash and ReceivablesAiko E. Lara100% (2)

- Key AnswerDocument27 pagesKey AnswerMelvin Lee Felipe GarbinNo ratings yet

- AFAR Summary Lecture (10 May 2021)Document30 pagesAFAR Summary Lecture (10 May 2021)Joanna MalubayNo ratings yet

- Chapter 15 Test Bank Partnerships - Formation, Operations, and Changes in Ownership InterestsDocument22 pagesChapter 15 Test Bank Partnerships - Formation, Operations, and Changes in Ownership InterestsOBC LingayenNo ratings yet

- Advanced Accounting 2Document9 pagesAdvanced Accounting 2Elmin ValdezNo ratings yet

- IAS 38 Intangible AssetsDocument29 pagesIAS 38 Intangible AssetsSherif MohamedNo ratings yet

- Accounts AmalgamationDocument6 pagesAccounts AmalgamationscarunamarNo ratings yet

- P4-1: Consolidated Financials for Pea Corp and Subsidiary Sen CorpDocument21 pagesP4-1: Consolidated Financials for Pea Corp and Subsidiary Sen Corpnancy tomanda100% (1)

- Balance Sheet: Alexei Alvarez Drobush, CFA, FRM Fabricio Chala, CFA, FRMDocument43 pagesBalance Sheet: Alexei Alvarez Drobush, CFA, FRM Fabricio Chala, CFA, FRMJhonatan Perez VillanuevaNo ratings yet

- Commerce, Bengali and English For 12 WbseDocument306 pagesCommerce, Bengali and English For 12 WbseDI S HANo ratings yet

- WORKSHEET ON ACCOUNTING FOR PARTNERSHIP Retirement and Death Board QuestionsDocument14 pagesWORKSHEET ON ACCOUNTING FOR PARTNERSHIP Retirement and Death Board QuestionsAhmedNo ratings yet

- Balance Sheet Related ConceptsDocument6 pagesBalance Sheet Related ConceptsNaga NagendraNo ratings yet

- This Study Resource WasDocument5 pagesThis Study Resource WasJyasmine Aura V. AgustinNo ratings yet

- Group Project ConsolidationDocument15 pagesGroup Project ConsolidationSyahrul Amirul100% (1)

- AFA Tut 3Document19 pagesAFA Tut 3Đỗ Kim ChiNo ratings yet

- Solution To Chapter 15Document9 pagesSolution To Chapter 15Ismail WardhanaNo ratings yet

- Chapter 1 Accounting For Business Combinations SolmanDocument10 pagesChapter 1 Accounting For Business Combinations SolmanKhen FajardoNo ratings yet

- 12 Acc Admission Partner Im3Document13 pages12 Acc Admission Partner Im3Piyush SrivastavaNo ratings yet