You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Test Bank For International Macroeconomics, 5e Robert Feenstra, Alan Taylor Test BankDocument22 pagesTest Bank For International Macroeconomics, 5e Robert Feenstra, Alan Taylor Test BankNail BaskoNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- ECON 461 Test 1 Fall 2014Document17 pagesECON 461 Test 1 Fall 2014Umaira925No ratings yet

- Economics Notes From IGCSE AIDDocument50 pagesEconomics Notes From IGCSE AIDAejaz MohamedNo ratings yet

- European Monetary SystemDocument19 pagesEuropean Monetary Systemhakheemvp4809100% (3)

- Public Sector in The North: Driver or Intruder?Document31 pagesPublic Sector in The North: Driver or Intruder?Olga MrinskaNo ratings yet

- Northern Economy in The Next DecadeDocument24 pagesNorthern Economy in The Next DecadeOlga MrinskaNo ratings yet

- Decentralisation in England: How Far Does SNR Take Things Forward, 2008Document15 pagesDecentralisation in England: How Far Does SNR Take Things Forward, 2008Olga MrinskaNo ratings yet

- Structural Economic Change and The EU, 2008Document73 pagesStructural Economic Change and The EU, 2008Olga MrinskaNo ratings yet

- A New Strategic Framework For Regional Policy in Ukraine, 2007Document4 pagesA New Strategic Framework For Regional Policy in Ukraine, 2007Olga MrinskaNo ratings yet

- Science Cities, 2008Document13 pagesScience Cities, 2008Olga MrinskaNo ratings yet

- DevaluationDocument3 pagesDevaluationBibhuti Bhusan SenapatyNo ratings yet

- The Impact of Government Expenditure OnDocument79 pagesThe Impact of Government Expenditure OnKingsley DickensNo ratings yet

- NSS Exploring Economics 5 (3 Edition) : Answers To ExercisesDocument20 pagesNSS Exploring Economics 5 (3 Edition) : Answers To ExercisesKingsley HoNo ratings yet

- Measuring National Customer Satisfaction: Sweden's Pioneering ExperienceDocument17 pagesMeasuring National Customer Satisfaction: Sweden's Pioneering Experienceshahmed999No ratings yet

- Can India Become A $5 Trillion Economy by 2024Document4 pagesCan India Become A $5 Trillion Economy by 2024Atul BishtNo ratings yet

- Carlinsoskice Chapter 2Document40 pagesCarlinsoskice Chapter 2Bruno SiebraNo ratings yet

- The Impact of Poor Governance On FDI BangladeshDocument228 pagesThe Impact of Poor Governance On FDI BangladeshAnisur Rahman FaroqueNo ratings yet

- Marxism DissDocument18 pagesMarxism Dissok bloomerNo ratings yet

- Banking-Industry Specific and Regional Economic Determinants of NPL - Evidence From US StateDocument3 pagesBanking-Industry Specific and Regional Economic Determinants of NPL - Evidence From US StateChinthaka PereraNo ratings yet

- Economic Forecast ColombiaDocument3 pagesEconomic Forecast Colombiasuper_sumoNo ratings yet

- Analyzing The Inflation To Consumer Expenditure in City Mall of Antipolo MarketDocument15 pagesAnalyzing The Inflation To Consumer Expenditure in City Mall of Antipolo MarketDexter CaroNo ratings yet

- A Tale of Four EconomiesDocument3 pagesA Tale of Four EconomiesAnis NajwaNo ratings yet

- Theories of ProfitDocument6 pagesTheories of Profitvinati100% (1)

- Macro Economics 1Document52 pagesMacro Economics 1MERSHANo ratings yet

- Econ1F22Syllabus 1Document3 pagesEcon1F22Syllabus 1Ritchie YangNo ratings yet

- Determinants of Ethiopian Tax RevenueDocument102 pagesDeterminants of Ethiopian Tax RevenueamanualNo ratings yet

- International Parity Conditions You Can TrustDocument51 pagesInternational Parity Conditions You Can Trustrohan100% (1)

- UNIT 01 - Macro EnvironmentDocument24 pagesUNIT 01 - Macro EnvironmentDimu GunawardanaNo ratings yet

- The Contemporary World: 02 Worksheet 1Document3 pagesThe Contemporary World: 02 Worksheet 1Ashley AcuñaNo ratings yet

- Determination of Income and Multiplier EffectDocument6 pagesDetermination of Income and Multiplier EffectDhanushka RajapakshaNo ratings yet

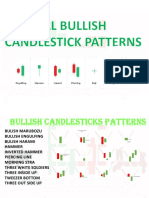

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Document25 pagesAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarNo ratings yet

- Spania - Stistica 2019: Show All StatisticsDocument8 pagesSpania - Stistica 2019: Show All StatisticsarthurqasNo ratings yet

- Principle Econ Chapter 1 PDFDocument28 pagesPrinciple Econ Chapter 1 PDFShaqif Hasan SajibNo ratings yet

- Personal FinanceDocument4 pagesPersonal FinanceAyeshaNo ratings yet

- PDF EngDocument14 pagesPDF EngHimanshu SethNo ratings yet

- 14 Ch36-Six Debates Over Macroeconomic Policy-KeyDocument15 pages14 Ch36-Six Debates Over Macroeconomic Policy-KeyChen JunhaoNo ratings yet