You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Internet Marketing Full Project ReportDocument88 pagesInternet Marketing Full Project Reportaquarius_tarun31% (13)

- Sales & Purchase Contract for Bonny Light Crude OilDocument17 pagesSales & Purchase Contract for Bonny Light Crude OilnurashenergyNo ratings yet

- Winding Up (Liquidation) DraftDocument55 pagesWinding Up (Liquidation) DraftZainab BillaNo ratings yet

- ch05 SM Carlon 5eDocument68 pagesch05 SM Carlon 5eKyleNo ratings yet

- Pricing StrategiesDocument58 pagesPricing StrategiesMark K. Eapen100% (2)

- EVENT Marketing Generates New BusinessDocument26 pagesEVENT Marketing Generates New Businesssuruchi100% (1)

- ACCT500 (16) Answers To Seminar 6Document5 pagesACCT500 (16) Answers To Seminar 6rashid rahmanzada100% (1)

- FlextimeDocument3 pagesFlextimerashid rahmanzadaNo ratings yet

- Maggi Brand Story and Management StrategiesDocument21 pagesMaggi Brand Story and Management Strategiesrashid rahmanzadaNo ratings yet

- 2.authority, Power Is Not LeadershipDocument2 pages2.authority, Power Is Not Leadershiprashid rahmanzadaNo ratings yet

- 2.authority, Power Is Not LeadershipDocument2 pages2.authority, Power Is Not Leadershiprashid rahmanzadaNo ratings yet

- Azerbaijan - Vision 2020 - Development Concept - ENGDocument26 pagesAzerbaijan - Vision 2020 - Development Concept - ENGrashid rahmanzadaNo ratings yet

- ACCT 500.fall 2016.course OutlineDocument9 pagesACCT 500.fall 2016.course Outlinerashid rahmanzadaNo ratings yet

- IMF99Document26 pagesIMF99rashid rahmanzadaNo ratings yet

- Ministry of Agriculture PresentationDocument11 pagesMinistry of Agriculture Presentationrashid rahmanzadaNo ratings yet

- Advantages of Azerbaijan For Foreign InvestorsDocument5 pagesAdvantages of Azerbaijan For Foreign Investorsrashid rahmanzadaNo ratings yet

- Literature ReviewDocument3 pagesLiterature Reviewrashid rahmanzadaNo ratings yet

- Managing Personal Selling & Key AccountsDocument61 pagesManaging Personal Selling & Key AccountsMaruko ChanNo ratings yet

- Warranty Against Hidden Defects of or Encumbrances Upon The Thing SoldDocument2 pagesWarranty Against Hidden Defects of or Encumbrances Upon The Thing SoldartNo ratings yet

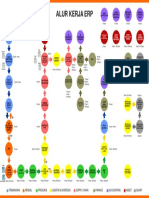

- Alur Kerja Erp: Pemasaran Rendal Produksi Logistik & Ekspedisi Supply Chain Finance Accounting Asset QuaryDocument1 pageAlur Kerja Erp: Pemasaran Rendal Produksi Logistik & Ekspedisi Supply Chain Finance Accounting Asset QuaryMuhammad FairusNo ratings yet

- Managing Managing: Sales Strategies Sales StrategiesDocument15 pagesManaging Managing: Sales Strategies Sales Strategiessaumya_ŠšNo ratings yet

- Globality' Why Companies Are Competing With Everyone From Everywhere For Everything-HandoutDocument4 pagesGlobality' Why Companies Are Competing With Everyone From Everywhere For Everything-HandoutJoseph GarciaNo ratings yet

- Sundaram Clayton Case Study ExcellenceDocument25 pagesSundaram Clayton Case Study ExcellenceSathyanarayana A Engineering MechanicalNo ratings yet

- AR Update and Billing RunDocument2 pagesAR Update and Billing RunLiberty Simeon TangianNo ratings yet

- Temsa Global's product strategy shift and organizational changesDocument5 pagesTemsa Global's product strategy shift and organizational changesfirinaluvina100% (1)

- Apple Company AnalysisDocument7 pagesApple Company AnalysisShahzadraees67% (3)

- G.R. No. L-53590 July 31, 1984 Rosario Brothers Inc. (Manila Cod Department Store) vs. Hon. Blas F. Ople, NLRC, Et Al. Relova, J.Document52 pagesG.R. No. L-53590 July 31, 1984 Rosario Brothers Inc. (Manila Cod Department Store) vs. Hon. Blas F. Ople, NLRC, Et Al. Relova, J.Rozzalie A. GonzalesNo ratings yet

- Forecasting Techniques in Fast Moving Consumer Goods Supply Chain: A Model ProposalDocument11 pagesForecasting Techniques in Fast Moving Consumer Goods Supply Chain: A Model ProposalWahidur RahmanNo ratings yet

- Challenges of E-CommerceDocument5 pagesChallenges of E-CommerceEditor IJTSRDNo ratings yet

- E CRMDocument16 pagesE CRMArjun NandaNo ratings yet

- Accounting DefinationDocument3 pagesAccounting DefinationNooray MalikNo ratings yet

- Advertising Has Become An Integral Part of Our SocietyDocument5 pagesAdvertising Has Become An Integral Part of Our SocietyHardeybeeyea Hardeydeyjjy100% (2)

- Consignment AccountDocument2 pagesConsignment AccountArulmani MurugesanNo ratings yet

- SM SummaryDocument10 pagesSM SummaryHaroon AslamNo ratings yet

- Marketing Strategy For NokiaDocument44 pagesMarketing Strategy For NokiaGurvinder SinghNo ratings yet

- LuxDocument33 pagesLuxshranju0% (1)

- Advertising Report On Radio ListnershipDocument48 pagesAdvertising Report On Radio ListnershipGaurav Kumar0% (1)

- Anamosa - A Reminiscence - Bertha FinnDocument456 pagesAnamosa - A Reminiscence - Bertha FinnAnamosa LibraryNo ratings yet

- Annamalai Univ MBA AssignmentsDocument11 pagesAnnamalai Univ MBA AssignmentssnraviNo ratings yet

- Introduction - The Impact of The Digital Revolution On Consumer BehaviorDocument27 pagesIntroduction - The Impact of The Digital Revolution On Consumer Behavioramitliarliar0% (1)

- Importanttablesforsapsd 130402023650 Phpapp01Document202 pagesImportanttablesforsapsd 130402023650 Phpapp01toralberNo ratings yet