You might also like

- CrytocurrencyDocument7 pagesCrytocurrencySeng Cheong KhorNo ratings yet

- ACCA SBL Chapter 12 Internal ControlDocument15 pagesACCA SBL Chapter 12 Internal ControlSeng Cheong KhorNo ratings yet

- BlockchainDocument4 pagesBlockchainSeng Cheong KhorNo ratings yet

- Sales & MarketingDocument2 pagesSales & MarketingSeng Cheong KhorNo ratings yet

- Akta 652 in EnglishDocument40 pagesAkta 652 in EnglishSeng Cheong KhorNo ratings yet

- ACCA SBL Chapter 1 LeadershipDocument9 pagesACCA SBL Chapter 1 LeadershipSeng Cheong KhorNo ratings yet

- WOU Flyer PDFDocument1 pageWOU Flyer PDFSeng Cheong KhorNo ratings yet

- WOU Flyer PDFDocument1 pageWOU Flyer PDFSeng Cheong KhorNo ratings yet

- ACCA Fundamentals Level Paper F3 Financial Accounting (International) Course Test 2Document16 pagesACCA Fundamentals Level Paper F3 Financial Accounting (International) Course Test 2Seng Cheong KhorNo ratings yet

- ACCA Strategic Business Leader SyllabusDocument25 pagesACCA Strategic Business Leader SyllabusSeng Cheong Khor100% (2)

- The Star Ads PDFDocument1 pageThe Star Ads PDFSeng Cheong KhorNo ratings yet

- Accruals PrepaymentsDocument9 pagesAccruals PrepaymentsSeng Cheong KhorNo ratings yet

- Session 1 - Scope of Governance I-UpdatedDocument73 pagesSession 1 - Scope of Governance I-UpdatedSeng Cheong KhorNo ratings yet

- The Tort Of: TechnicalDocument18 pagesThe Tort Of: TechnicalSeng Cheong KhorNo ratings yet

- F3, Financial Accounting (INT) Study GuideDocument13 pagesF3, Financial Accounting (INT) Study GuideSeng Cheong KhorNo ratings yet

- Advanced Audit and Assurance (International) : Tuesday 8 June 2010Document7 pagesAdvanced Audit and Assurance (International) : Tuesday 8 June 2010Seng Cheong KhorNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

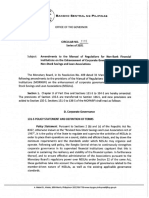

- Amendments To The Manual of Regulations For Non-Bank Financial Institutions On The Enhancement of Corporate Governance Guidelines For NSSLAsDocument25 pagesAmendments To The Manual of Regulations For Non-Bank Financial Institutions On The Enhancement of Corporate Governance Guidelines For NSSLAsHygie AlocodNo ratings yet

- Disini StartUpGuide InteractiveDocument19 pagesDisini StartUpGuide InteractiveDammy VegaNo ratings yet

- Eric Musselman Head BASKETBALL Coach 5.4.17Document23 pagesEric Musselman Head BASKETBALL Coach 5.4.17Reno Gazette JournalNo ratings yet

- The 2008 Constitution of El Consejo AtenistaDocument10 pagesThe 2008 Constitution of El Consejo AtenistaGlenn William AlcalaNo ratings yet

- Chas Realty Vs TalaveraDocument3 pagesChas Realty Vs TalaveraHector Mayel MacapagalNo ratings yet

- Sample Board ResolutionDocument1 pageSample Board ResolutionDats FernandezNo ratings yet

- Annual Report 2010 PDFDocument104 pagesAnnual Report 2010 PDFKhan MohhammadNo ratings yet

- Investment Code (Original) - MASBATE CITY INVESTMENT AND INCENTIVE CODEDocument9 pagesInvestment Code (Original) - MASBATE CITY INVESTMENT AND INCENTIVE CODEgbald100% (1)

- DeclarationDocument1 pageDeclarationChe Mohd FauziNo ratings yet

- By-Laws of CIMTODA Outline GovernanceDocument3 pagesBy-Laws of CIMTODA Outline GovernanceCHARLIE FLORINNo ratings yet

- 2016 06 NorthernsentinelDocument20 pages2016 06 Northernsentinelapi-258759326No ratings yet

- Almarai Annual Report English 2016Document128 pagesAlmarai Annual Report English 2016shjuthani_1No ratings yet

- Security Papers Limited 2018 Annual ReportDocument114 pagesSecurity Papers Limited 2018 Annual ReportBabar AdeebNo ratings yet

- RFBT Quiz No.3Document4 pagesRFBT Quiz No.3Clarice GonzalesNo ratings yet

- Business Organization ReviewerDocument7 pagesBusiness Organization ReviewerRozel L Reyes100% (2)

- Std11 Secretarial PracticeDocument14 pagesStd11 Secretarial PracticeVaril PereiraNo ratings yet

- Aurbach v. Sanitary WaresDocument20 pagesAurbach v. Sanitary WaresSaint AliaNo ratings yet

- Model Constitution for an Agricultural Primary Co-opDocument26 pagesModel Constitution for an Agricultural Primary Co-opdavis salatielNo ratings yet

- Page 6Document1 pagePage 6Ekushey TelevisionNo ratings yet

- 229 Executive Borad Meeting of NHADocument25 pages229 Executive Borad Meeting of NHAHamid NaveedNo ratings yet

- Unit Two Principles of Providing AdminisDocument29 pagesUnit Two Principles of Providing Adminisredwombat8432No ratings yet

- Publication AnnualReport 2018 PDF en MYDocument154 pagesPublication AnnualReport 2018 PDF en MYronasso7No ratings yet

- Paradip Port Employees (Recruitment, Seniority and Promotion) Regulations, 1967Document10 pagesParadip Port Employees (Recruitment, Seniority and Promotion) Regulations, 1967Latest Laws TeamNo ratings yet

- Module 16Document3 pagesModule 16AstxilNo ratings yet

- 15th Annual ReportDocument102 pages15th Annual ReportChandni PatelNo ratings yet

- Ms-4 Combined BookDocument380 pagesMs-4 Combined Bookanandjaymishra100% (1)

- R-037-24 ATTACH CBA LMPD Officers and SergeantsDocument62 pagesR-037-24 ATTACH CBA LMPD Officers and Sergeantsmark.stevensNo ratings yet

- Winner ApplicantDocument35 pagesWinner Applicantvarsha100% (1)

- SEC Case Derivative Suit Diversion Corporate FundsDocument2 pagesSEC Case Derivative Suit Diversion Corporate FundsKen AliudinNo ratings yet

- Preface:: Kumar Mangalam Birla CommitteeDocument4 pagesPreface:: Kumar Mangalam Birla CommitteeShainaazKhanNo ratings yet