You might also like

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceFrom EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinanceRating: 4 out of 5 stars4/5 (9)

- April SBIDocument5 pagesApril SBIRahul kumarNo ratings yet

- State Bank of India Old and New IFSC Code MappingDocument176 pagesState Bank of India Old and New IFSC Code Mappingssagrawal2000No ratings yet

- Customer SatisfactionDocument65 pagesCustomer SatisfactionChandan SrivastavaNo ratings yet

- Industry Profile: Priority Sector Lending & Analysis On Housing FinanceDocument52 pagesIndustry Profile: Priority Sector Lending & Analysis On Housing FinanceManjunath ManjuNo ratings yet

- SBI Banking Products Awareness Study ChartDocument4 pagesSBI Banking Products Awareness Study ChartJiby JohnNo ratings yet

- A Study On Recent Trends of Banking Sector in India: M.Sujatha, N.V Haritha, P. Sai SreejaDocument8 pagesA Study On Recent Trends of Banking Sector in India: M.Sujatha, N.V Haritha, P. Sai Sreejasomprakash giriNo ratings yet

- Overview of Banking IndustryDocument12 pagesOverview of Banking Industrybeena antuNo ratings yet

- Banking Industry Overview: History, Structure and Current ScenarioDocument77 pagesBanking Industry Overview: History, Structure and Current Scenarioprashant mhatreNo ratings yet

- Abstract - Role of Commercial Banks in IndiaDocument8 pagesAbstract - Role of Commercial Banks in Indiasalman.wajidNo ratings yet

- Structure of The Indian Banking Industry: Commercial BanksDocument2 pagesStructure of The Indian Banking Industry: Commercial BanksMayank AhujaNo ratings yet

- Banking System in India - An OverviewDocument32 pagesBanking System in India - An OverviewPraveenNo ratings yet

- Mission Vission and ValuesDocument8 pagesMission Vission and ValuesJiby JohnNo ratings yet

- AXIS ProjectDocument59 pagesAXIS ProjectSalim KhanNo ratings yet

- Indian Banking IndustryDocument12 pagesIndian Banking Industrysimranarora2007No ratings yet

- Banking StructureDocument3 pagesBanking StructureMayank AhujaNo ratings yet

- BankingDocument8 pagesBankingDivya NathNo ratings yet

- Credit Appraisal ProjectDocument109 pagesCredit Appraisal ProjectAshwath KodaguNo ratings yet

- Introduction of Banking SystemDocument10 pagesIntroduction of Banking SystemMasy1210% (1)

- BankDocument9 pagesBankakashgulati007No ratings yet

- BFSI Sector in IndiaDocument3 pagesBFSI Sector in IndiaKenneth GallowayNo ratings yet

- Cooommmercial BanksDocument29 pagesCooommmercial BanksSanjay YadavNo ratings yet

- Banking System in IndiaDocument9 pagesBanking System in IndiaBhavesh LimaniNo ratings yet

- Industry Analysis: Current Trends in The IndustryDocument7 pagesIndustry Analysis: Current Trends in The IndustryAshish GutgutiaNo ratings yet

- Structure of the Indian Banking System Sem IDocument2 pagesStructure of the Indian Banking System Sem IAshitosh ChavanNo ratings yet

- Research Paper - Roles of Commercial Bank in IndiaDocument9 pagesResearch Paper - Roles of Commercial Bank in Indiasalman.wajidNo ratings yet

- Indian Banking System StructureDocument13 pagesIndian Banking System StructureNandhini VirgoNo ratings yet

- Vijaya Bank and Dena Bank Being Merged Into The Bank of BarodaDocument3 pagesVijaya Bank and Dena Bank Being Merged Into The Bank of BarodaJerin VargheseNo ratings yet

- Rural DevelopmentsDocument88 pagesRural DevelopmentsVyom K ShahNo ratings yet

- Banking Practical 1 InformationDocument4 pagesBanking Practical 1 InformationMadhur AbhyankarNo ratings yet

- Economy Banking System in IndiaDocument21 pagesEconomy Banking System in Indiakrishan palNo ratings yet

- Evolution of The Indian Banking IndustryDocument7 pagesEvolution of The Indian Banking IndustryfasahmadNo ratings yet

- Types of Banks: BankingDocument11 pagesTypes of Banks: BankingKaviya KaviNo ratings yet

- The Banking OmbudsmanDocument93 pagesThe Banking OmbudsmanMini sureshNo ratings yet

- Banking Types ExplainedDocument0 pagesBanking Types Explainedsundeep_100No ratings yet

- Role of Indian Commercial Banks in Economic DevelopmentDocument8 pagesRole of Indian Commercial Banks in Economic DevelopmentPride Tutorials Manikbagh RoadNo ratings yet

- Fundamental Analysis of Banking SectorsDocument54 pagesFundamental Analysis of Banking SectorsRajesh BathulaNo ratings yet

- Vtu Darshan 12Document48 pagesVtu Darshan 12subashrao5522No ratings yet

- BankingDocument37 pagesBankingTanya GoelNo ratings yet

- Banking in IndiaDocument13 pagesBanking in IndiaMurahari NANo ratings yet

- Indian BankingDocument4 pagesIndian Bankingrahul vatsyayanNo ratings yet

- Introduction To Banking Sector & SbiDocument106 pagesIntroduction To Banking Sector & Sbiaparajitha lalasaNo ratings yet

- Structure of Banking System in IndiaDocument34 pagesStructure of Banking System in IndiaAyushi SinghNo ratings yet

- Economics ProjectDocument16 pagesEconomics ProjectYashvardhanNo ratings yet

- Banking Structure in IndiaDocument9 pagesBanking Structure in IndiaDhanu BhardwajNo ratings yet

- History of Banking IndustryDocument66 pagesHistory of Banking IndustryJissy ShravanNo ratings yet

- SummaryDocument10 pagesSummaryAditya ShrivastavaNo ratings yet

- Evolution of The Indian Banking IndustryDocument6 pagesEvolution of The Indian Banking IndustryNeha ChandnaNo ratings yet

- Banking Structure in IndiaDocument5 pagesBanking Structure in IndiaCharu Saxena16No ratings yet

- 6 Ispes Fy 2020 FinalDocument25 pages6 Ispes Fy 2020 FinalDhruti GuptaNo ratings yet

- Banks and Bank ManagementDocument6 pagesBanks and Bank ManagementyjgjbhhbNo ratings yet

- Mod 1 BankingDocument59 pagesMod 1 Bankingaikansh jainNo ratings yet

- Banking Sector OverviewDocument34 pagesBanking Sector OverviewteckdivNo ratings yet

- All About Cooperative Banks in India GK Notes For SSC Banking Exams in PDFDocument8 pagesAll About Cooperative Banks in India GK Notes For SSC Banking Exams in PDFramuvindiaNo ratings yet

- Types of Banks Draft/ Types of Banks/ Banking in IndiaDocument4 pagesTypes of Banks Draft/ Types of Banks/ Banking in Indiaamarx292000100% (1)

- Banking & InsuranceDocument79 pagesBanking & InsuranceMonashreeNo ratings yet

- BfsiDocument9 pagesBfsiMohd ImtiazNo ratings yet

- 04 - Chapter 1Document27 pages04 - Chapter 1shantishree04No ratings yet

- Indian Banking System OverviewDocument82 pagesIndian Banking System OverviewSvijayakanthan SelvarajNo ratings yet

- 3rd Chapter IFIMDocument10 pages3rd Chapter IFIMDarshan PanditNo ratings yet

- Banking DetailsDocument9 pagesBanking DetailsModi HaniNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Leter PadDocument2 pagesLeter PadShivuPannurNo ratings yet

- Chapter 3Document28 pagesChapter 3ShivuPannurNo ratings yet

- Chapter 45Document10 pagesChapter 45ShivuPannurNo ratings yet

- Sunil LL LLLLL LLLLL LLLLLDocument44 pagesSunil LL LLLLL LLLLL LLLLLShivuPannurNo ratings yet

- Chapter 4Document73 pagesChapter 4ShivuPannurNo ratings yet

- MCHPT 1Document7 pagesMCHPT 1ShivuPannurNo ratings yet

- Kanaka Letter PadDocument2 pagesKanaka Letter PadShivuPannurNo ratings yet

- Chapter 3Document28 pagesChapter 3ShivuPannurNo ratings yet

- Chapter 1Document5 pagesChapter 1ShivuPannurNo ratings yet

- Chapter 1Document4 pagesChapter 1ShivuPannurNo ratings yet

- Chapter 1Document5 pagesChapter 1ShivuPannurNo ratings yet

- New Microsoft Office Word DocumentDocument1 pageNew Microsoft Office Word DocumentShivuPannurNo ratings yet

- Credit Management IntroductionDocument4 pagesCredit Management IntroductionShivuPannurNo ratings yet

- New Microsoft Office Word DocumentDocument1 pageNew Microsoft Office Word DocumentShivuPannurNo ratings yet

- Merger of SBI Bank With Its AssociatesDocument1 pageMerger of SBI Bank With Its AssociatesNaina BakshiNo ratings yet

- "A Study Mutual FundsDocument103 pages"A Study Mutual FundsMaster PrintersNo ratings yet

- A Comparative Study of Customer Satisfaction of ICICI Bank and SBI BankDocument35 pagesA Comparative Study of Customer Satisfaction of ICICI Bank and SBI BankRuchi YadavNo ratings yet

- Facing InterviewDocument358 pagesFacing InterviewPramod Kumar SrivastavaNo ratings yet

- E02dcindustry News Digest (Issue No. 4)Document63 pagesE02dcindustry News Digest (Issue No. 4)Prafulla TekriwalNo ratings yet

- Black Book Project.Document60 pagesBlack Book Project.Franxx Darling100% (1)

- Head Master: Rupees Fifty Five Thousand Five Hundred and Eighty Three OnlyDocument10 pagesHead Master: Rupees Fifty Five Thousand Five Hundred and Eighty Three Onlyvijay kumarNo ratings yet

- Notifn - No.57.STAFF NURSE PDFDocument22 pagesNotifn - No.57.STAFF NURSE PDFE.n. SreenivasuluNo ratings yet

- KCC Bank: Project Report ONDocument61 pagesKCC Bank: Project Report ONSunny KhushdilNo ratings yet

- Financial Inclusion in IndiaDocument20 pagesFinancial Inclusion in IndiaSameer Singh FPM Student, Jaipuria LucknowNo ratings yet

- 65 State Bank My SoreDocument32 pages65 State Bank My SoreGiridhar Gowda K NNo ratings yet

- Customer Satisfaction at SBIDocument43 pagesCustomer Satisfaction at SBIManeesh SharmaNo ratings yet

- CISS For Cold Storage - Chhattisgarh State Year-Wise DataDocument3 pagesCISS For Cold Storage - Chhattisgarh State Year-Wise DataAshokNo ratings yet

- GAIL Gas Limited: Tender Document For Procurement of Pe Pipes (1 Year Arc)Document219 pagesGAIL Gas Limited: Tender Document For Procurement of Pe Pipes (1 Year Arc)BGL NAGARNo ratings yet

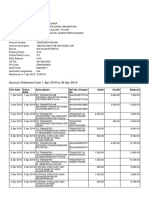

- Account Statement From 1 Oct 2020 To 30 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 1 Oct 2020 To 30 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNITIK BAISOYANo ratings yet

- Comparative Analysis of Capital Structure & Financial Performance of SBI and ICICI BankDocument85 pagesComparative Analysis of Capital Structure & Financial Performance of SBI and ICICI BankSuraj DubeyNo ratings yet

- S.B.I VRSDocument4 pagesS.B.I VRSdhanyamelamNo ratings yet

- A Study On Consumer Awareness and UsageDocument78 pagesA Study On Consumer Awareness and UsageTilluNo ratings yet

- Bms Project MumbaiDocument62 pagesBms Project MumbaiNaim AshrafNo ratings yet

- The ICICI Has Announced The Launch of Mobile Banking Services For Its CustomersDocument2 pagesThe ICICI Has Announced The Launch of Mobile Banking Services For Its CustomersANKIT SINGHNo ratings yet

- 3 March-2020Document24 pages3 March-2020వన మాలిNo ratings yet

- Newzen Mba Finance 2022Document12 pagesNewzen Mba Finance 2022New Zen InfotechNo ratings yet

- Chapter 3Document54 pagesChapter 3koushik kumarNo ratings yet

- SbiDocument2 pagesSbiyaswanthNo ratings yet

- Account Statement From 1 Feb 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceFIRDUS ALINo ratings yet

- Customer SatisficationDocument27 pagesCustomer SatisficationMukesh ManwaniNo ratings yet

- Origin and Evolution of SBIDocument39 pagesOrigin and Evolution of SBINitin AryaNo ratings yet