You might also like

- JACKSON V AEG Transcripts Michael Joseph Jackson JR (Prince) June 26th 2013 'They're Going To Kill Me,' Michael Jackson Told SonDocument96 pagesJACKSON V AEG Transcripts Michael Joseph Jackson JR (Prince) June 26th 2013 'They're Going To Kill Me,' Michael Jackson Told SonTeamMichael100% (2)

- ASSIGNMENT LAW 2 (TASK 1) (2) BBBDocument4 pagesASSIGNMENT LAW 2 (TASK 1) (2) BBBChong Kai MingNo ratings yet

- Accounting Crossword Puzzle Answer KeyDocument1 pageAccounting Crossword Puzzle Answer KeyFru RyNo ratings yet

- Walmart Research PlanDocument7 pagesWalmart Research PlanErin TurnerNo ratings yet

- Financial Analysis of PSODocument35 pagesFinancial Analysis of PSOSabeen Javaid75% (4)

- Financial Analysis of Pso: Nust School of Electrical Engineering and Computer ScienceDocument35 pagesFinancial Analysis of Pso: Nust School of Electrical Engineering and Computer ScienceRaja WaqarNo ratings yet

- PSO Financial Analysis ReportDocument35 pagesPSO Financial Analysis ReportTaha ZakiNo ratings yet

- About Us: Ratio-AnalysisDocument8 pagesAbout Us: Ratio-AnalysisttsopalNo ratings yet

- SWOT& Financial Data Pakistan Petroleum LimitedDocument13 pagesSWOT& Financial Data Pakistan Petroleum LimitedFarah Nawaz QabulioNo ratings yet

- Psopk: Audit and FinanceDocument22 pagesPsopk: Audit and FinanceAhmed Nafees KhanNo ratings yet

- Pakistan Petroleum LimitedDocument11 pagesPakistan Petroleum Limitedmuazzamjani101100% (1)

- PsoDocument43 pagesPsoHassanj Amal100% (1)

- Financial Management Pso Project ReportDocument72 pagesFinancial Management Pso Project ReportAsim Malik100% (2)

- Assignment OF Banking and Working Capital ON Financial Accounts and Working Capital OF GailDocument9 pagesAssignment OF Banking and Working Capital ON Financial Accounts and Working Capital OF GailSachin Kumar BassiNo ratings yet

- Financial Analysis of Ogdcl and SSGCLDocument24 pagesFinancial Analysis of Ogdcl and SSGCLShahid MehmoodNo ratings yet

- Head Office Lubes Manufacturing Plant: PSO OverviewDocument3 pagesHead Office Lubes Manufacturing Plant: PSO OverviewAnnus SalamNo ratings yet

- POL Oilfields PotentialDocument23 pagesPOL Oilfields PotentialMuhammad Ali KhanNo ratings yet

- Shell Petroleium Company Group 13Document14 pagesShell Petroleium Company Group 13muh.bilaltariq19No ratings yet

- Pakistan Insight - 20200727 - Power Previews - Twofold Earnings, Dividends Expected.Document3 pagesPakistan Insight - 20200727 - Power Previews - Twofold Earnings, Dividends Expected.SHAHZAIB -No ratings yet

- A Proposal To Analyze Financial Statements For 3 Years of Lucky Cement Limited and Attock Cement Pakistan LimitedDocument4 pagesA Proposal To Analyze Financial Statements For 3 Years of Lucky Cement Limited and Attock Cement Pakistan LimitedHina SohailNo ratings yet

- PCTE Group of Institutes, Ludhiana: Mba 2 Semester CDocument9 pagesPCTE Group of Institutes, Ludhiana: Mba 2 Semester CrohanNo ratings yet

- Moil Limited: (A Govt. of India Enterprise) Moil Bhawan, 1-A Katol Road, NAGPUR - 440 013Document9 pagesMoil Limited: (A Govt. of India Enterprise) Moil Bhawan, 1-A Katol Road, NAGPUR - 440 013amits3989No ratings yet

- Ongc Report1111Document35 pagesOngc Report1111shubhraiiseNo ratings yet

- FSA1Document15 pagesFSA1Imran Faisal AlNo ratings yet

- Risk Factors: Oil Price VolatilityDocument3 pagesRisk Factors: Oil Price VolatilityHammad HussainNo ratings yet

- Financial Statement Analysis of Petroleum CompaniesDocument32 pagesFinancial Statement Analysis of Petroleum CompaniesAnoosha AlamNo ratings yet

- Ratio Analysis of Pakistani Oil IndustriesDocument41 pagesRatio Analysis of Pakistani Oil IndustriesArsalan Tahir75% (4)

- BizCon - PSO Report - SM Sun - Sir FaisalDocument23 pagesBizCon - PSO Report - SM Sun - Sir FaisalJuvairia BadarNo ratings yet

- Attock Petroleum Financial Report 2010Document6 pagesAttock Petroleum Financial Report 2010Naveed JavedNo ratings yet

- 17 Jul CilDocument85 pages17 Jul CilPritam BasuNo ratings yet

- Annual Report Suzuki 2014Document104 pagesAnnual Report Suzuki 2014Shabbir UddinNo ratings yet

- KSE Issues ProspectsDocument29 pagesKSE Issues ProspectsMubashir Ali KhanNo ratings yet

- Final Assignment of KaleemDocument12 pagesFinal Assignment of Kaleemaaaliya7777No ratings yet

- Internship Report in PSODocument5 pagesInternship Report in PSOSayyed SofianNo ratings yet

- BPCL History, Products, FinancialsDocument15 pagesBPCL History, Products, FinancialsSristyNo ratings yet

- Financial Analysis of Fu-Wang Ceramic Limited and R.A.K Ceramic LimitedDocument26 pagesFinancial Analysis of Fu-Wang Ceramic Limited and R.A.K Ceramic LimitedAlizay NishatNo ratings yet

- Final Marketing Project On Pakistan State OilDocument34 pagesFinal Marketing Project On Pakistan State OilMaan UsmanNo ratings yet

- Ibrahim Asim 17U00506 Sec AFSA Report SubmissionDocument34 pagesIbrahim Asim 17U00506 Sec AFSA Report Submissiontech damnNo ratings yet

- Petronas Gas AR 2010 Cover-P49Document51 pagesPetronas Gas AR 2010 Cover-P49alice_s_5No ratings yet

- Company BusinessDocument2 pagesCompany BusinessFuzail ShoaibNo ratings yet

- Institute of Business Management financial forecasting model for PSODocument13 pagesInstitute of Business Management financial forecasting model for PSOHussainRazaWasifNo ratings yet

- REPORTDocument36 pagesREPORTPhương ThanhNo ratings yet

- Renuka Sugars PVT LTDDocument22 pagesRenuka Sugars PVT LTDeasyinformationNo ratings yet

- Industrial Analysis of PSODocument8 pagesIndustrial Analysis of PSOAkash AliNo ratings yet

- OGDCL'S Secondary Public Offering - 2007: Term ReportDocument7 pagesOGDCL'S Secondary Public Offering - 2007: Term ReportNoama NaeemNo ratings yet

- GVK Power & Infrastructure Ltd: Undervalued Infrastructure Stock Trading at Single DigitsDocument7 pagesGVK Power & Infrastructure Ltd: Undervalued Infrastructure Stock Trading at Single DigitsBharatNo ratings yet

- BYCO Petroleum LimitedDocument8 pagesBYCO Petroleum Limitedhamza dosaniNo ratings yet

- MNC ReportDocument23 pagesMNC ReportSheriYar KhattakNo ratings yet

- Q1. Define Leasing Companies and How Many Companies Are Working in Pakistan?Document7 pagesQ1. Define Leasing Companies and How Many Companies Are Working in Pakistan?Rashid ShahzadNo ratings yet

- Final Internship Report SummerDocument23 pagesFinal Internship Report SummerSunny Rawlani0% (2)

- About The Company: Indian Railway Indian Ordnance FactoriesDocument11 pagesAbout The Company: Indian Railway Indian Ordnance FactoriesIMRAN ALAMNo ratings yet

- Ministry of Petroleum and Natural Gas & Oidb: Energy Sector Structures, Policies and RegulationsDocument7 pagesMinistry of Petroleum and Natural Gas & Oidb: Energy Sector Structures, Policies and RegulationsNikesh PullurNo ratings yet

- PSO Company ProfileDocument19 pagesPSO Company ProfileAfaq Ahmed0% (1)

- Name List: - Afaque Ahmed Khoso Mashooque Ali Akhter Ali Baber Ali Roll Num: - 2K19/BBAE/12/79/18/38Document13 pagesName List: - Afaque Ahmed Khoso Mashooque Ali Akhter Ali Baber Ali Roll Num: - 2K19/BBAE/12/79/18/38Afaq AhmedNo ratings yet

- Pso FinalDocument15 pagesPso FinalAdeel SajidNo ratings yet

- In Focus: ICI Pakistan: The Upcoming DealDocument2 pagesIn Focus: ICI Pakistan: The Upcoming Dealtrillion5No ratings yet

- Lucky Cement Final Project Report On: Financial Statement AnalysisDocument25 pagesLucky Cement Final Project Report On: Financial Statement AnalysisPrecious BarbieNo ratings yet

- PsoDocument37 pagesPsolittlelite100% (1)

- 1 Introductio1Document3 pages1 Introductio1Faisal Ur Rahman AwanNo ratings yet

- Capital Venture: A Synopsis on Role and PerformanceDocument17 pagesCapital Venture: A Synopsis on Role and PerformanceSurojitJanaNo ratings yet

- Business Development Strategy for the Upstream Oil and Gas IndustryFrom EverandBusiness Development Strategy for the Upstream Oil and Gas IndustryRating: 5 out of 5 stars5/5 (1)

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportFrom EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportNo ratings yet

- Activity Exp June-16Document1 pageActivity Exp June-16Arsal AliNo ratings yet

- Request For Quotation - Supply of Goods v1Document13 pagesRequest For Quotation - Supply of Goods v1Arsal AliNo ratings yet

- Stock 18-02-16Document2 pagesStock 18-02-16Arsal AliNo ratings yet

- List StockDocument4 pagesList StockArsal AliNo ratings yet

- Grade Tracker1Document16 pagesGrade Tracker1Arsal AliNo ratings yet

- Activity Detail (Sale Wise, Profit & Exp) BOR C & W Sale Profit Expense Sale Profit ExpenseDocument4 pagesActivity Detail (Sale Wise, Profit & Exp) BOR C & W Sale Profit Expense Sale Profit ExpenseArsal AliNo ratings yet

- The Evolution of Leadership TheoriesDocument16 pagesThe Evolution of Leadership TheoriesEng Matti Ur RehmanNo ratings yet

- C12 13 LeadershipDocument41 pagesC12 13 LeadershipMukesh KumarNo ratings yet

- Institutional Sales Form Evaluation FormDocument1 pageInstitutional Sales Form Evaluation FormArsal AliNo ratings yet

- A Sample QuotationDocument3 pagesA Sample QuotationArsal AliNo ratings yet

- Soap ManufacturingDocument34 pagesSoap ManufacturingArsal AliNo ratings yet

- EmployeeDocument3 pagesEmployeeArsal AliNo ratings yet

- Surf ExcelDocument29 pagesSurf ExcelArsal AliNo ratings yet

- A Ratio Analysis Report On FINALDocument34 pagesA Ratio Analysis Report On FINALArsal AliNo ratings yet

- Hafiz /nasir Expense Nasir 5500 Shahid 700 Nasir 2000 Nasir 1550 Hafiz 2000Document1 pageHafiz /nasir Expense Nasir 5500 Shahid 700 Nasir 2000 Nasir 1550 Hafiz 2000Arsal AliNo ratings yet

- Task Force Action Plan FormatDocument8 pagesTask Force Action Plan FormatArsal AliNo ratings yet

- Gourmet BakeryDocument12 pagesGourmet Bakeryabdakbar60% (5)

- Reserve Currency Devaluation and Its Impact On The Global EconomyDocument15 pagesReserve Currency Devaluation and Its Impact On The Global EconomyArsal AliNo ratings yet

- Project Outline &: A) Executive Summary: Page #Document31 pagesProject Outline &: A) Executive Summary: Page #Ar Rehman67% (6)

- Shezan Vs GourmetDocument23 pagesShezan Vs GourmetArsal AliNo ratings yet

- Trans JourDocument9 pagesTrans JourLorena SierraNo ratings yet

- Accounting 3.1-3.2-3.3Document16 pagesAccounting 3.1-3.2-3.3Arsal AliNo ratings yet

- Marketing Project by WaqasDocument26 pagesMarketing Project by WaqasWaqas Anwar100% (5)

- Experience LetterDocument1 pageExperience LetterArsal Ali100% (2)

- Annexure IDocument3 pagesAnnexure IArsal AliNo ratings yet

- AcknowledgementDocument44 pagesAcknowledgementArsal AliNo ratings yet

- Customer DetailDocument2 pagesCustomer DetailArsal AliNo ratings yet

- AcknowledgementDocument44 pagesAcknowledgementArsal AliNo ratings yet

- Group Membersather Abdul Jabbar E10Document2 pagesGroup Membersather Abdul Jabbar E10Arsal AliNo ratings yet

- Event Planning Rubric - Alternative Event Project Template Luc PatbergDocument1 pageEvent Planning Rubric - Alternative Event Project Template Luc Patbergapi-473891068No ratings yet

- Dendrite InternationalDocument9 pagesDendrite InternationalAbhishek VermaNo ratings yet

- Exploring Supply Chain Collaboration of Manufacturing Firms in ChinaDocument220 pagesExploring Supply Chain Collaboration of Manufacturing Firms in Chinajuan cota maodNo ratings yet

- Midterm Exam 2Document8 pagesMidterm Exam 2Nhi Nguyễn HoàngNo ratings yet

- Straight Bill of LadingDocument2 pagesStraight Bill of LadingHafizUmarArshad100% (1)

- Michigan LLC Articles of OrganizationDocument3 pagesMichigan LLC Articles of OrganizationRocketLawyer100% (2)

- HR Getting Smart Agile Working - 2014 - tcm18 14105.pdf, 08.07.2018 PDFDocument38 pagesHR Getting Smart Agile Working - 2014 - tcm18 14105.pdf, 08.07.2018 PDFKhushbuNo ratings yet

- Starting Small Family BusinessDocument4 pagesStarting Small Family BusinessMJ BenedictoNo ratings yet

- My Dream Company: Why Join ITC Limited (Under 40 charsDocument9 pagesMy Dream Company: Why Join ITC Limited (Under 40 charsamandeep152No ratings yet

- TATA Family TreeDocument1 pageTATA Family Treemehulchauhan_9950% (2)

- Case 1 - Iguazu Offices Financial ModelDocument32 pagesCase 1 - Iguazu Offices Financial ModelapoorvnigNo ratings yet

- Average Due Date and Account CurrentDocument80 pagesAverage Due Date and Account CurrentShynaNo ratings yet

- WA Payroll Tax 22-23Document1 pageWA Payroll Tax 22-23JMLNo ratings yet

- Action Plan To Control The BreakagesDocument1 pageAction Plan To Control The BreakagesAyan Mitra75% (4)

- Profile of The Indian Consumers 1Document2 pagesProfile of The Indian Consumers 1mvsrikrishna100% (1)

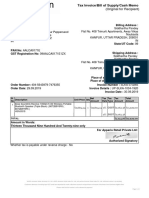

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Satyam SinghNo ratings yet

- Economy in Steel - A Practical GuideDocument30 pagesEconomy in Steel - A Practical Guidechandabhi70No ratings yet

- J H: A E M C S F M: Umping Edges N Xamination of Ovements in Opper Pot and Utures ArketsDocument21 pagesJ H: A E M C S F M: Umping Edges N Xamination of Ovements in Opper Pot and Utures ArketsKumaran SanthoshNo ratings yet

- Formato Casa de La Calidad (QFD)Document11 pagesFormato Casa de La Calidad (QFD)Diego OrtizNo ratings yet

- The Venture Capitalist With A Silicon Valley Solution For Minority Owned BusinessesDocument4 pagesThe Venture Capitalist With A Silicon Valley Solution For Minority Owned BusinessesAngel AlijaNo ratings yet

- FABTEKDocument11 pagesFABTEKKarthik ArumughamNo ratings yet

- Asian Paints document discusses company history and marketing strategiesDocument27 pagesAsian Paints document discusses company history and marketing strategiesHardik Prajapati100% (1)

- 300+ TOP Central Civil Services (Conduct) Rules MCQs and Answers 2022Document1 page300+ TOP Central Civil Services (Conduct) Rules MCQs and Answers 2022Indhunesan Packirisamy100% (2)

- Review MODULE - MATHEMATICS (Algebra-Worded Problems) : Number Problems Age ProblemDocument1 pageReview MODULE - MATHEMATICS (Algebra-Worded Problems) : Number Problems Age ProblemYeddaMIlaganNo ratings yet

- SEC - Graduate PositionDocument6 pagesSEC - Graduate PositionGiorgos MeleasNo ratings yet

- Optimize Supply Chains with Bonded WarehousingDocument8 pagesOptimize Supply Chains with Bonded WarehousingJohannesRöderNo ratings yet