You might also like

- Chapter 13 Summary: SP8-13: Further Considerations When RatingDocument2 pagesChapter 13 Summary: SP8-13: Further Considerations When RatingPython ClassesNo ratings yet

- Full 100 Marks Insurance Project (Blackbook) For Bachelor of Banking & Insurance and BMS. I Do Not Own It.Document50 pagesFull 100 Marks Insurance Project (Blackbook) For Bachelor of Banking & Insurance and BMS. I Do Not Own It.KáúśtúbhÇóólNo ratings yet

- Answers - Chapter 4Document3 pagesAnswers - Chapter 4Nazlı YumruNo ratings yet

- Next 4Document10 pagesNext 4Nurhasanah Asyari100% (1)

- Insurance Accounting and Finance: Lecture#4 by Dr. Muhammad UsmanDocument8 pagesInsurance Accounting and Finance: Lecture#4 by Dr. Muhammad UsmanNoor MahmoodNo ratings yet

- Accounting Standards Saudi Arabia InsuranceDocument8 pagesAccounting Standards Saudi Arabia InsurancecateNo ratings yet

- Discussion Paper v33 FinalDocument38 pagesDiscussion Paper v33 FinalPrince KumarNo ratings yet

- Answer Key Answer Key: Bansw 1 1 October 2014 5:37 PMDocument40 pagesAnswer Key Answer Key: Bansw 1 1 October 2014 5:37 PMCharbelSaadéNo ratings yet

- What Are Your Hedging Options?: Executive SummaryDocument3 pagesWhat Are Your Hedging Options?: Executive SummarytrevinooscarNo ratings yet

- Derivatives NotesDocument4 pagesDerivatives NotesSoumyaNairNo ratings yet

- Chapter One The Legal Perspective: Appropriate Profit Margins in Property & Casualty Insurance RatesDocument12 pagesChapter One The Legal Perspective: Appropriate Profit Margins in Property & Casualty Insurance RatesHuy Vu ChiNo ratings yet

- Summary Aboody, Barth and Kasznik, JAR, 2004Document7 pagesSummary Aboody, Barth and Kasznik, JAR, 2004jrkruijs001No ratings yet

- Valuation of Life Insurance Companies in IndiaDocument11 pagesValuation of Life Insurance Companies in IndiaVersha KaushikNo ratings yet

- Optimal Designation of Hedging Relationships Under FASB Statement 133Document13 pagesOptimal Designation of Hedging Relationships Under FASB Statement 133postscriptNo ratings yet

- ACCO 20083 Chapter 3 ReviewerDocument7 pagesACCO 20083 Chapter 3 ReviewerVincent Luigil AlceraNo ratings yet

- Uniformity and Disclosure, Billy & SaikouDocument15 pagesUniformity and Disclosure, Billy & Saikoudian kusumaNo ratings yet

- Journal of Accountancy March 2013Document8 pagesJournal of Accountancy March 2013hhpdenverNo ratings yet

- InterestRate HedgingDocument4 pagesInterestRate HedgingPablo TrianaNo ratings yet

- Cast Study - GM MotorsDocument9 pagesCast Study - GM MotorsAbdullahIsmailNo ratings yet

- IFRS17 Considerations Health InsurersDocument4 pagesIFRS17 Considerations Health Insurersjester lawNo ratings yet

- Progressive Final PaperDocument16 pagesProgressive Final PaperJordyn WebreNo ratings yet

- PUB OECD TransferPricing Guidance 0723 PDFDocument4 pagesPUB OECD TransferPricing Guidance 0723 PDFTRYNo ratings yet

- General Insurance Business UnderwritingDocument8 pagesGeneral Insurance Business UnderwritingMukesh LalNo ratings yet

- Synergy Limitation ParadoxDocument32 pagesSynergy Limitation ParadoxtheswingineerNo ratings yet

- Internal Loss FinancingDocument4 pagesInternal Loss Financingvivek0% (1)

- Understanding Australian Accounting Standards 1st Edition Loftus Solutions ManualDocument28 pagesUnderstanding Australian Accounting Standards 1st Edition Loftus Solutions Manualdarkishacerose5jf100% (20)

- Baker McKenzie - Bloomberg - OECD Transfer Pricing Guidelines - 4 - 8 - 20Document11 pagesBaker McKenzie - Bloomberg - OECD Transfer Pricing Guidelines - 4 - 8 - 20Sen JanNo ratings yet

- Accounting For Derivatives - FAS 133 PDFDocument4 pagesAccounting For Derivatives - FAS 133 PDFSayyed Mohammed AshuNo ratings yet

- M.VOC. (I&FM) Semester: Ii Chapter - 4 Financial Aspects of Business Interruption InsuranceDocument18 pagesM.VOC. (I&FM) Semester: Ii Chapter - 4 Financial Aspects of Business Interruption InsuranceRanjit TalpadaNo ratings yet

- FE Case StudyDocument4 pagesFE Case StudyMohammad Sameer AnsariNo ratings yet

- Underwriting and Ratemaking: Why Underwriting? What Is Its Purpose?Document27 pagesUnderwriting and Ratemaking: Why Underwriting? What Is Its Purpose?vijaijohn100% (1)

- SP7 - Chapter 1 SummaryDocument3 pagesSP7 - Chapter 1 Summaryvivek mittalNo ratings yet

- Everything About HedgingDocument114 pagesEverything About HedgingFlorentinnaNo ratings yet

- Suggestions of Core Group On Distribution Framework - 10112023Document6 pagesSuggestions of Core Group On Distribution Framework - 10112023insurancekatariaNo ratings yet

- Insurance AccountingDocument34 pagesInsurance Accountingrcpgeneral100% (1)

- An Evaluation of Merger and Aquisition On The Insurance Company On The Nigerian EconomyDocument70 pagesAn Evaluation of Merger and Aquisition On The Insurance Company On The Nigerian EconomySoyannwo Fiyinfolu100% (2)

- Limitations of The MFRS 119Document2 pagesLimitations of The MFRS 119HidayahFauzi100% (1)

- InsuranceDocument7 pagesInsurancesarvesh.bhartiNo ratings yet

- ACCOUNTING PRINCIPLES AND PRACTICES in INSURANCE COMPANIESDocument4 pagesACCOUNTING PRINCIPLES AND PRACTICES in INSURANCE COMPANIESSifat TarannumNo ratings yet

- Underwriting Cycles in The Property - Casualty Insurance IndustryDocument67 pagesUnderwriting Cycles in The Property - Casualty Insurance Industrynitin238No ratings yet

- Seminar Report ON Corporate Hedging Process & Techniques Submitted To: Sir. Yasin Zia Submitted By: Zahid Hussain 2009-Ag-65 MBA (R) FinanceDocument12 pagesSeminar Report ON Corporate Hedging Process & Techniques Submitted To: Sir. Yasin Zia Submitted By: Zahid Hussain 2009-Ag-65 MBA (R) FinanceZahid HussainNo ratings yet

- Derivatives & Structured Products - SBR 1: Case: Rethinking Saizeriya's Currency Hedging StrategyDocument6 pagesDerivatives & Structured Products - SBR 1: Case: Rethinking Saizeriya's Currency Hedging StrategyPooja JainNo ratings yet

- Clark 6Document55 pagesClark 6thisisghostactualNo ratings yet

- Mergers and AcquisitionsDocument79 pagesMergers and Acquisitions匿匿100% (1)

- Analysis and InterpretationDocument36 pagesAnalysis and Interpretationpratikmehra18No ratings yet

- Proposed Changes in Insurance Accounting RulesDocument3 pagesProposed Changes in Insurance Accounting Rulesharis gunawanNo ratings yet

- Examination: Subject CT2 Finance and Financial Reporting Core TechnicalDocument8 pagesExamination: Subject CT2 Finance and Financial Reporting Core TechnicalMohit TharejaNo ratings yet

- GX Ifrs17 What Does It Mean For YouDocument12 pagesGX Ifrs17 What Does It Mean For YouZaid KamalNo ratings yet

- Other Liabilities Measurement IssuesDocument6 pagesOther Liabilities Measurement Issuesgenius_blueNo ratings yet

- Article: A. View As A BBF StudentDocument10 pagesArticle: A. View As A BBF StudentDonnaFaithCaluraNo ratings yet

- Script 2Document11 pagesScript 2aa4e11No ratings yet

- Overview of ValuationDocument5 pagesOverview of ValuationIvory ClaudioNo ratings yet

- Key RatiosDocument5 pagesKey RatiosShreevathsaNo ratings yet

- Insurance 1Document28 pagesInsurance 1Anant SharmaNo ratings yet

- Profit Split MethodDocument5 pagesProfit Split MethodStähli Lukas100% (1)

- FRS & J.P. Morgan London Whale CaseDocument10 pagesFRS & J.P. Morgan London Whale CasedecalgosNo ratings yet

- FSF Principles For Sound Compensation Practices: Financial Stability ForumDocument18 pagesFSF Principles For Sound Compensation Practices: Financial Stability Forumatos10No ratings yet

- PWC Captive InsuranceDocument13 pagesPWC Captive InsurancehvikashNo ratings yet

- Chapter 8 - Operations of Insurance CompaniesDocument11 pagesChapter 8 - Operations of Insurance CompaniesFrancis Gumawa100% (1)

- 8 Retained Earnings and Quasi-ReorganizationDocument5 pages8 Retained Earnings and Quasi-ReorganizationNasiba M. AbdulcaderNo ratings yet

- Chapter24 Cashflowstatements2008Document21 pagesChapter24 Cashflowstatements2008Marium Rafiq100% (2)

- R03.7 Guidance For Standard VDocument18 pagesR03.7 Guidance For Standard VBảo TrâmNo ratings yet

- Its Earning That Count SummaryDocument115 pagesIts Earning That Count SummaryTheda VeldaNo ratings yet

- Dr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsDocument2 pagesDr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsmariaNo ratings yet

- FM Unit IDocument15 pagesFM Unit ILakshmi RajanNo ratings yet

- Affidavit of Loss Stock and Transfer BookDocument1 pageAffidavit of Loss Stock and Transfer BookA&L Consulting100% (1)

- AMFI Question & AnswerDocument67 pagesAMFI Question & AnswerVirag67% (3)

- Lopez Holdings Corporation - LPZDocument2 pagesLopez Holdings Corporation - LPZJC CalaycayNo ratings yet

- Ac Far Quiz4Document5 pagesAc Far Quiz4Kristine Joy CutillarNo ratings yet

- Talbots Harvard Case AnsDocument4 pagesTalbots Harvard Case AnsChristel Yeo0% (1)

- What Is Auditing: Financial AuditDocument2 pagesWhat Is Auditing: Financial AuditZack EmoNo ratings yet

- Discussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument3 pagesDiscussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoTatianaNo ratings yet

- Income Tax Payment Challan: PSID #: 21114984Document1 pageIncome Tax Payment Challan: PSID #: 21114984Zia Sultan AwanNo ratings yet

- Philippine Bonded Warehouse Services, Inc. Application For Accreditation To CCBW 1415Document3 pagesPhilippine Bonded Warehouse Services, Inc. Application For Accreditation To CCBW 1415Itsfreynk05No ratings yet

- List of Hedge Funds From OdpDocument5 pagesList of Hedge Funds From OdpChris AbbottNo ratings yet

- Indian Capital MarketDocument19 pagesIndian Capital MarketdollieNo ratings yet

- HO 1 - Commercial Law - Corporation Law PDFDocument35 pagesHO 1 - Commercial Law - Corporation Law PDFBerchman MelendezNo ratings yet

- IAS 12 - Income TaxesDocument55 pagesIAS 12 - Income Taxesrafid aliNo ratings yet

- Afisco Insurance Corporation v. CA 302 SCRA 1Document2 pagesAfisco Insurance Corporation v. CA 302 SCRA 1Kayee KatNo ratings yet

- Strategic Management - Midterm Quiz 1Document6 pagesStrategic Management - Midterm Quiz 1Uy SamuelNo ratings yet

- CH 12Document44 pagesCH 12kevin echiverriNo ratings yet

- Aud Prob Compilation 1Document31 pagesAud Prob Compilation 1Chammy TeyNo ratings yet

- CTOS SME Score Report Company SampleDocument9 pagesCTOS SME Score Report Company SampleAdolfo VillaniNo ratings yet

- ERAA Annual Report 2018Document338 pagesERAA Annual Report 2018Irhab khairunisaNo ratings yet

- A Study On Merger and Acquisition in Insurance Industry in IndiaDocument10 pagesA Study On Merger and Acquisition in Insurance Industry in IndiariddhiNo ratings yet

- TOA - 01-CASH AND CASH EQUIVALENTS W - SOLDocument5 pagesTOA - 01-CASH AND CASH EQUIVALENTS W - SOLPachi100% (1)

- Company Info - Print FinancialsDocument5 pagesCompany Info - Print FinancialsVishvajit PatilNo ratings yet

- What Is A Private PlacementDocument3 pagesWhat Is A Private PlacementKritika TNo ratings yet

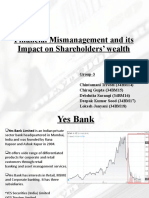

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodNo ratings yet