You might also like

- Sometimes in Exam Questions: You Get Given An Impairment Indicator.Document2 pagesSometimes in Exam Questions: You Get Given An Impairment Indicator.sayedrushdiNo ratings yet

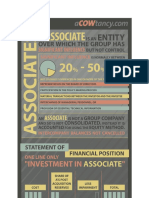

- AssociatesDocument1 pageAssociatessayedrushdiNo ratings yet

- F9 Practice Kit 400 McqsDocument186 pagesF9 Practice Kit 400 Mcqsjarom100% (5)

- Chittagong Tax Bar Membership RegisterDocument187 pagesChittagong Tax Bar Membership RegistersayedrushdiNo ratings yet

- Leave List 2018 Approved by Govet.Document5 pagesLeave List 2018 Approved by Govet.sayedrushdiNo ratings yet

- F7-06 IAS 18 RevenueDocument10 pagesF7-06 IAS 18 Revenuesayedrushdi100% (1)

- F7-01 International Financial Reporting StandardsDocument16 pagesF7-01 International Financial Reporting Standardssayedrushdi100% (1)

- Lease ChartDocument1 pageLease ChartsayedrushdiNo ratings yet

- Website CRMDocument4 pagesWebsite CRMsayedrushdiNo ratings yet

- F7-03 Substance Over FormDocument10 pagesF7-03 Substance Over FormPaiNo ratings yet

- Provisions and contingent liabilities accountingDocument6 pagesProvisions and contingent liabilities accountingsayedrushdiNo ratings yet

- F7-06 IAS 18 RevenueDocument10 pagesF7-06 IAS 18 Revenuesayedrushdi100% (1)

- InvestopediaDocument1 pageInvestopediasayedrushdiNo ratings yet

- Credit Risk ManagementDocument64 pagesCredit Risk Managementcherry_nu100% (12)

- E BookDocument5 pagesE BooksayedrushdiNo ratings yet

- Credit risk management techniquesDocument6 pagesCredit risk management techniquessayedrushdiNo ratings yet

- Credit Risk ManagementDocument64 pagesCredit Risk Managementcherry_nu100% (12)

- Credit risk management techniquesDocument6 pagesCredit risk management techniquessayedrushdiNo ratings yet

- CRM Bangladeh Bank-2015Document54 pagesCRM Bangladeh Bank-2015sayedrushdiNo ratings yet

- Evaluating Credit Risk ModelsDocument23 pagesEvaluating Credit Risk ModelsSaina ChuhNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- ZTBL Internship Report PDFDocument71 pagesZTBL Internship Report PDFmuhammad waseem100% (8)

- Red Ink Flows MateriDocument15 pagesRed Ink Flows MateriVelia MonicaNo ratings yet

- Legal Liability of Cpas: Mcgraw-Hill/IrwinDocument23 pagesLegal Liability of Cpas: Mcgraw-Hill/IrwinWenJiangNo ratings yet

- NGAS: New Government Accounting SystemDocument56 pagesNGAS: New Government Accounting SystemVenianNo ratings yet

- ICAP Disclosure Checklist For Listed CompaniesDocument69 pagesICAP Disclosure Checklist For Listed Companiesmuhammad waqar siddiqui50% (2)

- Review of LiteratureDocument5 pagesReview of LiteraturePOOONIASAUMYA100% (1)

- A Review and Analysis of International Accounting Research in JIAAT 2002 2010 2010 Journal of International Accounting, Auditing and TaxationDocument17 pagesA Review and Analysis of International Accounting Research in JIAAT 2002 2010 2010 Journal of International Accounting, Auditing and TaxationiportobelloNo ratings yet

- Financial Accounting and Reporting StandardsDocument1 pageFinancial Accounting and Reporting StandardsAllysa CapunoNo ratings yet

- Acca - Fia - Cat - Dipifr - Abe:: Join Our Exam-Focused Lecturing Team ForDocument2 pagesAcca - Fia - Cat - Dipifr - Abe:: Join Our Exam-Focused Lecturing Team Forshyam48No ratings yet

- CFAS QUIZ 3 PrelimDocument8 pagesCFAS QUIZ 3 Prelim수지50% (2)

- 11 AmalgmationDocument38 pages11 AmalgmationPranaya Agrawal100% (1)

- 2023mahindrasubsidiary Reportlow Res 1Document3,136 pages2023mahindrasubsidiary Reportlow Res 1M.n KNo ratings yet

- Formative AssessmentsDocument13 pagesFormative AssessmentsJoshNo ratings yet

- Controles SoxDocument22 pagesControles SoxzmeraldiithamNo ratings yet

- Audit Report Exer MC 1920 W Key1Document8 pagesAudit Report Exer MC 1920 W Key1aleachonNo ratings yet

- Pharmexcil DataDocument86 pagesPharmexcil DataRandoNo ratings yet

- Managing Financial Resources and Decisions of Finance Finance Essay (WEB)Document28 pagesManaging Financial Resources and Decisions of Finance Finance Essay (WEB)johnNo ratings yet

- Marketing Case StudyDocument21 pagesMarketing Case StudyShrey KashyapNo ratings yet

- Questions For QuizesDocument3 pagesQuestions For QuizesNovelyn DuyoganNo ratings yet

- 44475bos34356sm Mod3 cp10 PDFDocument44 pages44475bos34356sm Mod3 cp10 PDFVinay GoyalNo ratings yet

- CM Kiem Toan Viet Nam - EngDocument213 pagesCM Kiem Toan Viet Nam - EngDiep NguyenNo ratings yet

- Fasb 69 Oil and Gas DisclosuresDocument44 pagesFasb 69 Oil and Gas DisclosureslmccandlesNo ratings yet

- BBMA3103 Management Accounting I AssignmentDocument17 pagesBBMA3103 Management Accounting I AssignmentKSSNo ratings yet

- Glenmark PDFDocument229 pagesGlenmark PDFSwet ChesterNo ratings yet

- 2018 Report PDFDocument154 pages2018 Report PDFChamodh NethsaraNo ratings yet

- Presentation of Financial Statements (IAS 1)Document30 pagesPresentation of Financial Statements (IAS 1)Ashura ShaibNo ratings yet

- Psa 710Document18 pagesPsa 710xxxxxxxxxNo ratings yet

- Managerial Accounting 13th Edition by Warren Reeve and Duchac Test BankDocument93 pagesManagerial Accounting 13th Edition by Warren Reeve and Duchac Test Bankjosephine100% (25)

- Draft Red Herring Prospectus GuideDocument10 pagesDraft Red Herring Prospectus GuideChidananda SwaroopNo ratings yet

- Financial Statement Analysis Unit 3Document12 pagesFinancial Statement Analysis Unit 3Jiya KothariNo ratings yet