You might also like

- Bata Stage 3Document4 pagesBata Stage 3samy7541No ratings yet

- Consumer Price Index (CPI)Document8 pagesConsumer Price Index (CPI)samy7541No ratings yet

- Quality Services Theory ExplainedDocument3 pagesQuality Services Theory Explainedsamy7541No ratings yet

- Return On Equity Net Income/Shareholder's EquityDocument3 pagesReturn On Equity Net Income/Shareholder's Equitysamy7541No ratings yet

- Lateral Thinking NotesDocument4 pagesLateral Thinking Notessamy7541No ratings yet

- Problems of SMEDocument16 pagesProblems of SMEsamy7541No ratings yet

- Quality ProductsDocument2 pagesQuality Productssamy7541No ratings yet

- Q1Document1 pageQ1samy7541No ratings yet

- AnalysisDocument4 pagesAnalysissamy7541No ratings yet

- Literature Review EconomicsDocument4 pagesLiterature Review Economicssamy7541No ratings yet

- Definition 2. How Planning Starts 3. Levels of Planning 4. Types of PlansDocument21 pagesDefinition 2. How Planning Starts 3. Levels of Planning 4. Types of Planssamy7541No ratings yet

- Project Financing - Financial Scheme For Long-Term ProjectsDocument11 pagesProject Financing - Financial Scheme For Long-Term Projectssamy7541No ratings yet

- Effect On Revenue Due To Change in PriceDocument3 pagesEffect On Revenue Due To Change in Pricesamy7541No ratings yet

- MaliDocument3 pagesMalisamy7541No ratings yet

- Banking StocksDocument61 pagesBanking Stockssamy7541No ratings yet

- Transactional AnalysisDocument23 pagesTransactional Analysissamy7541No ratings yet

- Share Price of Eicher Motors Over The YearsDocument6 pagesShare Price of Eicher Motors Over The Yearssamy7541No ratings yet

- Stock IndexDocument32 pagesStock Indexsamy7541No ratings yet

- Eicher Motors Limited WordDocument4 pagesEicher Motors Limited Wordsamy7541No ratings yet

- Spartek CeramicsDocument9 pagesSpartek Ceramicssamy7541No ratings yet

- Swot SpartekDocument3 pagesSwot Sparteksamy7541No ratings yet

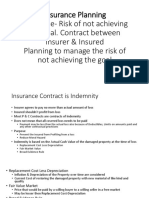

- Insurance PlanningDocument15 pagesInsurance Planningsamy7541No ratings yet

- Havells Acquisition of Lloyds SWOT AnalysisDocument2 pagesHavells Acquisition of Lloyds SWOT Analysissamy7541No ratings yet

- Wealth MGT 2013 QbankDocument2 pagesWealth MGT 2013 Qbanksamy7541No ratings yet

- Indemnity BondDocument2 pagesIndemnity Bondsamy754192% (12)

- List of DocumentDocument1 pageList of Documentsamy7541No ratings yet

- Electronic Performance Management SystemDocument3 pagesElectronic Performance Management SystemRaghu AppuNo ratings yet

- HansDocument19 pagesHanssamy7541No ratings yet

- HRM ConceptsDocument10 pagesHRM Conceptssamy7541No ratings yet

- 12 Economics Notes Micro Ch01 IntroductionDocument9 pages12 Economics Notes Micro Ch01 IntroductionRama NagpalNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Deposit AccountDocument2 pagesDeposit AccountAnonymous ZGcs7MwsLNo ratings yet

- Foundation Model ConstitutionDocument18 pagesFoundation Model ConstitutionMahmoodHassan100% (1)

- Word CV TemplateDocument2 pagesWord CV Templatebima saktiNo ratings yet

- Analyst Assessment Test - 1 (ANSWER)Document4 pagesAnalyst Assessment Test - 1 (ANSWER)Christian CabadonggaNo ratings yet

- Success StoryDocument27 pagesSuccess StoryEr Raghav GuptaNo ratings yet

- Grapevine CommunicationDocument1 pageGrapevine CommunicationPavan KoundinyaNo ratings yet

- Retail KPI formulas and examplesDocument1 pageRetail KPI formulas and examplessugandhaNo ratings yet

- Sales Manager Business Development in Los Angeles CA Resume Kevin JohnstonDocument3 pagesSales Manager Business Development in Los Angeles CA Resume Kevin JohnstonKevinJohnstonNo ratings yet

- 2 Accounting For MaterialsDocument13 pages2 Accounting For MaterialsZenCamandangNo ratings yet

- LERAC M AND E Cash Forecast and Accounts Payable AgingDocument15 pagesLERAC M AND E Cash Forecast and Accounts Payable AgingLERAC AccountingNo ratings yet

- Curriculum Vitae: Raj Kumar Bhattacharjee (Raj)Document15 pagesCurriculum Vitae: Raj Kumar Bhattacharjee (Raj)New Dream TelecomNo ratings yet

- OD125549891478426000Document1 pageOD125549891478426000अमित कुमारNo ratings yet

- B e F U L L y P A I: Basis of The Intellectual Property Law (R.A. 8293, As Amended)Document4 pagesB e F U L L y P A I: Basis of The Intellectual Property Law (R.A. 8293, As Amended)Dred OpleNo ratings yet

- Merck Decision TreeDocument4 pagesMerck Decision Treeparth2k0% (1)

- Roles of MELTC in Deveolping Multi-Modal TransportDocument7 pagesRoles of MELTC in Deveolping Multi-Modal TransporthaumbamilNo ratings yet

- Maintenance Cost Implications On ResidenDocument17 pagesMaintenance Cost Implications On ResidenBarnabas UdehNo ratings yet

- Big CharimanDocument39 pagesBig CharimanUpender BhatiNo ratings yet

- KKC Seller Consignment Contract RevisedDocument3 pagesKKC Seller Consignment Contract Revisedapi-284910984No ratings yet

- Performance ManagementDocument38 pagesPerformance ManagementNatania SitorusNo ratings yet

- SHE Organogram 013Document6 pagesSHE Organogram 013Saif Mohammad KhanNo ratings yet

- MAF302 Formula Sheet: Key Financial ConceptsDocument2 pagesMAF302 Formula Sheet: Key Financial ConceptsWill LeeNo ratings yet

- Midterm PtaskDocument4 pagesMidterm PtaskJanine CalditoNo ratings yet

- TMForum - EtomDocument61 pagesTMForum - EtomJosé EvangelistaNo ratings yet

- Sample Form Legal Opinion LetterDocument2 pagesSample Form Legal Opinion LetterLindsay Mills100% (1)

- Jawapan ACC116 Week 6-Nahzatul ShimaDocument2 pagesJawapan ACC116 Week 6-Nahzatul Shimaanon_207469897No ratings yet

- Week 12 Compulsory Quiz - Attempt Review 2ndDocument5 pagesWeek 12 Compulsory Quiz - Attempt Review 2nd정은주No ratings yet

- Paediatric Consumer Health in The Philippines PDFDocument4 pagesPaediatric Consumer Health in The Philippines PDFMae SampangNo ratings yet

- Atrium Management Corporation v. Court of Appeals, G.R. No. 109491, February 28, 2001 - Personal liability of corporate officers for negligenceDocument2 pagesAtrium Management Corporation v. Court of Appeals, G.R. No. 109491, February 28, 2001 - Personal liability of corporate officers for negligenceAmir Nazri KaibingNo ratings yet

- SivecoDocument27 pagesSivecoAna FiodorovNo ratings yet

- VMware Non Profit Customer DefinitionsDocument2 pagesVMware Non Profit Customer DefinitionsWaru11No ratings yet