You might also like

- Terms AND Conditions: Simplylife - AeDocument21 pagesTerms AND Conditions: Simplylife - AeVeera ManiNo ratings yet

- Aub Credit Cards T&CDocument16 pagesAub Credit Cards T&CAlberto GaNo ratings yet

- China Bank Credit Card Terms and ConditionsDocument15 pagesChina Bank Credit Card Terms and ConditionsDakuro A EthanNo ratings yet

- Amex Everyday Cardmember Agreement C1d1ecaf78 D6d0af7085 5bb5661feeDocument21 pagesAmex Everyday Cardmember Agreement C1d1ecaf78 D6d0af7085 5bb5661feeSadul RasasaraNo ratings yet

- Managing Your Card With CareDocument33 pagesManaging Your Card With CareLipsin LeeNo ratings yet

- Debit Card TermsDocument2 pagesDebit Card Termssanjay guravNo ratings yet

- HJSKDocument24 pagesHJSKB. SinghNo ratings yet

- Terms & Conditions of SABB Credit CardsDocument12 pagesTerms & Conditions of SABB Credit CardsMuqthar AhammedNo ratings yet

- RBL CC Cardmember AgreementDocument23 pagesRBL CC Cardmember AgreementAlagesan ManoNo ratings yet

- COMELEC Prepaid Card Enrollment Form FINALDocument1 pageCOMELEC Prepaid Card Enrollment Form FINALJuan LorenzoNo ratings yet

- RBL CC Cardmember AgreementDocument37 pagesRBL CC Cardmember AgreementBITI Education Pvt. Ltd.No ratings yet

- Ola TNC and MitcDocument54 pagesOla TNC and MitcManu BhatiaNo ratings yet

- Sample Employee Handbook - National Council of Nonprofits OrganizationDocument13 pagesSample Employee Handbook - National Council of Nonprofits OrganizationKenneth GarciaNo ratings yet

- Bdo TCSDocument7 pagesBdo TCSJohn PitaoNo ratings yet

- Metrobank Card Terms in 40 CharactersDocument13 pagesMetrobank Card Terms in 40 CharactersMark Titus Montoya RamosNo ratings yet

- Card TermDocument26 pagesCard TermAnas AnsariNo ratings yet

- Elite Terms and ConditionDocument22 pagesElite Terms and ConditionciitmNo ratings yet

- AmBank AggrmntDocument12 pagesAmBank AggrmntNoor Hazimah JalaluddinNo ratings yet

- BDO Credit Card Terms and ConditionsDocument7 pagesBDO Credit Card Terms and ConditionsHolly WestNo ratings yet

- Visa International Application FormDocument4 pagesVisa International Application FormJoel_10010No ratings yet

- PNB CCDocument13 pagesPNB CCArim TorrNo ratings yet

- Clip MitcDocument3 pagesClip Mitcshatrudhan bhardwajNo ratings yet

- Bdo Credit Cards Cash Advance Terms and Conditions - Revised As of Oct 2022Document2 pagesBdo Credit Cards Cash Advance Terms and Conditions - Revised As of Oct 2022mikechuasecoNo ratings yet

- CC T&C21122022Document22 pagesCC T&C21122022jeetNo ratings yet

- Pre Paid Cards TC enDocument7 pagesPre Paid Cards TC enAbdulla SameehNo ratings yet

- DC Usage Guide TNC - 30.09.2022Document5 pagesDC Usage Guide TNC - 30.09.2022SowjanyaNo ratings yet

- Terms and Conditions For Bank AL Habib ATM Debit CardDocument7 pagesTerms and Conditions For Bank AL Habib ATM Debit CardTanveer AhmedNo ratings yet

- Terms and Condition Credit Card enDocument25 pagesTerms and Condition Credit Card enaslamNo ratings yet

- Indian Bank Global Credit Card Terms and ConditionsDocument13 pagesIndian Bank Global Credit Card Terms and ConditionsSenthil PrabhuNo ratings yet

- Citi Cardmember TermsDocument44 pagesCiti Cardmember TermsJanmejoy DasNo ratings yet

- MasterCard Prepaid TandCDocument9 pagesMasterCard Prepaid TandCmikeNo ratings yet

- Samba Alkhair Credit Card TermsDocument3 pagesSamba Alkhair Credit Card TermsBilalsalamehNo ratings yet

- AMEX Generic TC Jan2021Document12 pagesAMEX Generic TC Jan2021Genesis MacaleNo ratings yet

- Deposit Card AgreementDocument7 pagesDeposit Card AgreementDavid ValdezNo ratings yet

- Terms and Conditions: Debit CSD T&C-Leaflet - 99X210mm 1 2 3 4 5Document2 pagesTerms and Conditions: Debit CSD T&C-Leaflet - 99X210mm 1 2 3 4 5Abhishek MNNo ratings yet

- APPLY VISA PREPAID CARDDocument2 pagesAPPLY VISA PREPAID CARDShiela HuniNo ratings yet

- Terms and Conditions - Debit Card Issuance & OperationsDocument4 pagesTerms and Conditions - Debit Card Issuance & OperationshemnathNo ratings yet

- Debit Card PolicyDocument8 pagesDebit Card Policycuriousgames24No ratings yet

- Indian Bank Global Credit Card Usage GuideDocument14 pagesIndian Bank Global Credit Card Usage GuideJijithpillaiNo ratings yet

- SBM Onecard Lite TCsDocument28 pagesSBM Onecard Lite TCsRAJ KUMHARENo ratings yet

- HBL DebitCards - Terms and ConditionsDocument40 pagesHBL DebitCards - Terms and ConditionsDonNo ratings yet

- Card MemberDocument130 pagesCard MemberPrem Chand GuptaNo ratings yet

- Paisabazaar Duet CC TNCDocument4 pagesPaisabazaar Duet CC TNCManjunathNo ratings yet

- Quick Cash TNCDocument3 pagesQuick Cash TNCpankaj sharmaNo ratings yet

- BDO Debit Card T&CsDocument6 pagesBDO Debit Card T&CsEjay ReyesNo ratings yet

- Terms and Conditions - UCPB Debit CardDocument2 pagesTerms and Conditions - UCPB Debit Cardsky9213100% (2)

- UBLWiz Application FormDocument2 pagesUBLWiz Application Formsaif_khan1155No ratings yet

- Terms Conditions 1dDocument12 pagesTerms Conditions 1dJose Achicahuala MamaniNo ratings yet

- CR TermsDocument14 pagesCR Termsmaruf.potterNo ratings yet

- Atm Cum Debit Card Application FormDocument2 pagesAtm Cum Debit Card Application FormImran AhmadNo ratings yet

- Terms and Conditions On The Issuance and Use of RCBC Credit CardsDocument15 pagesTerms and Conditions On The Issuance and Use of RCBC Credit CardsGillian Alexis ColegadoNo ratings yet

- Mashreq Millionaire Certificate Key TermsDocument2 pagesMashreq Millionaire Certificate Key TermsKunjemy EmyNo ratings yet

- Terms & ConditionsDocument15 pagesTerms & ConditionsBhavana AliasNo ratings yet

- Citi Credit Card Terms at a GlanceDocument110 pagesCiti Credit Card Terms at a GlanceJ&A Partners JANNo ratings yet

- Corporate Debit Card Application FormDocument3 pagesCorporate Debit Card Application FormMonisha ShanmuNo ratings yet

- Credit Card Terms and Conditions: Info@homecredit - PH)Document8 pagesCredit Card Terms and Conditions: Info@homecredit - PH)Victor Czar AustriaNo ratings yet

- Terms and Conditions (HBL CreditCard)Document92 pagesTerms and Conditions (HBL CreditCard)Muhammad Farukh IbtasamNo ratings yet

- Con tc4Document17 pagesCon tc4Alex IonuțNo ratings yet

- Cardmember PDFDocument131 pagesCardmember PDFAbbas AliNo ratings yet

- Summary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipeFrom EverandSummary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipeNo ratings yet

- Resume: Personal DetailsDocument2 pagesResume: Personal DetailsP Singh KarkiNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part7 PDFDocument1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part7 PDFP Singh KarkiNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part6Document1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part6P Singh KarkiNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part1Document1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part1P Singh KarkiNo ratings yet

- Contractor TipsDocument3 pagesContractor TipsTanmay VegadNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part5Document1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part5P Singh KarkiNo ratings yet

- Outdoor Gear Brand Wildcraft ProfileDocument1 pageOutdoor Gear Brand Wildcraft ProfileP Singh KarkiNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part9 PDFDocument1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part9 PDFP Singh KarkiNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part2Document1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part2P Singh KarkiNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part3Document1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part3P Singh KarkiNo ratings yet

- Clothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part4Document1 pageClothing, Footwear, Bags and Gear Brand in India - Wildcraft - Part4P Singh KarkiNo ratings yet

- Outdoor Clothing, Footwear, Bags and Gear Brand in India - WildcraftDocument1 pageOutdoor Clothing, Footwear, Bags and Gear Brand in India - WildcraftP Singh KarkiNo ratings yet

- About Germany Part8Document5 pagesAbout Germany Part8P Singh KarkiNo ratings yet

- Change Your DNS Servers On Windows - NordVPN Customer SupportDocument7 pagesChange Your DNS Servers On Windows - NordVPN Customer SupportP Singh KarkiNo ratings yet

- PDFSigQFormalRep PDFDocument1 pagePDFSigQFormalRep PDFJim LeeNo ratings yet

- Germany Visit Part 1Document5 pagesGermany Visit Part 1P Singh KarkiNo ratings yet

- Weight Calculation From Available Length Width in MM and Weight in Micron For FilmDocument1 pageWeight Calculation From Available Length Width in MM and Weight in Micron For FilmP Singh KarkiNo ratings yet

- Weight Calculation From Available Length Width in MM and Weight in Micron For FilmDocument1 pageWeight Calculation From Available Length Width in MM and Weight in Micron For FilmP Singh KarkiNo ratings yet

- About Germany Part3Document5 pagesAbout Germany Part3P Singh KarkiNo ratings yet

- About Germany Part9Document4 pagesAbout Germany Part9P Singh KarkiNo ratings yet

- About Germany Part7Document5 pagesAbout Germany Part7P Singh KarkiNo ratings yet

- Change Your DNS Servers On Windows - NordVPN Customer SupportDocument7 pagesChange Your DNS Servers On Windows - NordVPN Customer SupportP Singh KarkiNo ratings yet

- About Germany Part6Document5 pagesAbout Germany Part6P Singh KarkiNo ratings yet

- About Germany Part2Document5 pagesAbout Germany Part2P Singh KarkiNo ratings yet

- About Germany Part5Document5 pagesAbout Germany Part5P Singh KarkiNo ratings yet

- Ratio & Proportion Part 3Document5 pagesRatio & Proportion Part 3P Singh KarkiNo ratings yet

- About Germany Part4Document5 pagesAbout Germany Part4P Singh KarkiNo ratings yet

- Ratio & Proportion Part 2Document5 pagesRatio & Proportion Part 2P Singh KarkiNo ratings yet

- Ratio & Proportion Part 4Document1 pageRatio & Proportion Part 4P Singh KarkiNo ratings yet

- Ratio & Proportion Part 1Document5 pagesRatio & Proportion Part 1P Singh KarkiNo ratings yet

- Corporate Financial Management IntroDocument17 pagesCorporate Financial Management IntroADEYANJU AKEEMNo ratings yet

- Power To Make Rules For Controlling Stock ExchangeDocument3 pagesPower To Make Rules For Controlling Stock ExchangeSambit Kumar PaniNo ratings yet

- Overseas Fund and Share Account ApplicationDocument2 pagesOverseas Fund and Share Account ApplicationMaria Evans MayorNo ratings yet

- Barclays Shiller White PaperDocument36 pagesBarclays Shiller White PaperRyan LeggioNo ratings yet

- Economic Factors Impacting International BusinessDocument29 pagesEconomic Factors Impacting International BusinessRana Ankita100% (1)

- Enhanced Credit Report SummaryDocument9 pagesEnhanced Credit Report Summaryarcman17100% (1)

- TVM Problems SolvedDocument1 pageTVM Problems SolvedKathleenNo ratings yet

- Banking Regulations SummaryDocument20 pagesBanking Regulations SummaryGraceson Binu Sebastian100% (1)

- Foreign BanksDocument9 pagesForeign Banks1986anuNo ratings yet

- Omtex Classes: "The Home of Success"Document4 pagesOmtex Classes: "The Home of Success"AMIN BUHARI ABDUL KHADERNo ratings yet

- Non-Current Liabilities Cheat SheetDocument1 pageNon-Current Liabilities Cheat SheetSarah SafiraNo ratings yet

- APT Literature Review: Arbitrage Pricing TheoryDocument11 pagesAPT Literature Review: Arbitrage Pricing Theorydiala_khNo ratings yet

- Section "A" Very Short Answer Questions) (Attempt All Questions)Document5 pagesSection "A" Very Short Answer Questions) (Attempt All Questions)Ayusha TimalsinaNo ratings yet

- High Tire PerformanceDocument8 pagesHigh Tire PerformanceSofía MargaritaNo ratings yet

- Mini Case 29Document3 pagesMini Case 29Avon Jade RamosNo ratings yet

- UntitledDocument71 pagesUntitledIsaque Dietrich GarciaNo ratings yet

- Pace 215-Project B-Demition 1Document6 pagesPace 215-Project B-Demition 1SELYN DEMITIONNo ratings yet

- Comparing Channel Finance FacilitiesDocument34 pagesComparing Channel Finance FacilitiesSAIMBAhelplineNo ratings yet

- ACBP5122wA1 PDFDocument9 pagesACBP5122wA1 PDFAmmarah Ramnarain0% (1)

- The Most Dangerous Organization in America ExposedDocument37 pagesThe Most Dangerous Organization in America ExposedDomenico Bevilacqua100% (1)

- Compiler Additional Questions For Nov 22 ExamsDocument18 pagesCompiler Additional Questions For Nov 22 ExamsRobertNo ratings yet

- 10b Investment Property PDFDocument40 pages10b Investment Property PDFmEOW SNo ratings yet

- Palak Jindal - Summer Internship ReportDocument40 pagesPalak Jindal - Summer Internship ReportHarsh Kumar100% (2)

- Understanding Balance SheetsDocument40 pagesUnderstanding Balance SheetsHimanshu KashyapNo ratings yet

- SBR Notes by Ali Amir 20-21Document68 pagesSBR Notes by Ali Amir 20-21Mensur Ćuprija100% (1)

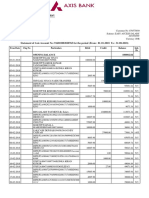

- Statement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Document9 pagesStatement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Saran ManiNo ratings yet

- Econ CH 10Document16 pagesEcon CH 10BradNo ratings yet

- CA - FOUNDATION LT (APRIL BATCH) NOV'23WE-4 QP-keyDocument4 pagesCA - FOUNDATION LT (APRIL BATCH) NOV'23WE-4 QP-keyDhruv AgarwalNo ratings yet

- Sec - C - TVM 2019 - PW, FW, AW, GR, Nom-EffDocument4 pagesSec - C - TVM 2019 - PW, FW, AW, GR, Nom-EffNaveen KumarNo ratings yet

- Xi Pre Final AccountsDocument7 pagesXi Pre Final AccountsDrishti ChauhanNo ratings yet