You might also like

- Accounting for Loans and Credit Card OperationsDocument12 pagesAccounting for Loans and Credit Card OperationsMohamed AmirNo ratings yet

- A, B, C - Specialised Accounting - 2Document15 pagesA, B, C - Specialised Accounting - 2محمود احمدNo ratings yet

- Banking System: Commercial BanksDocument15 pagesBanking System: Commercial BanksAAMIR IBRAHIMNo ratings yet

- Current Liabilities ManagementDocument18 pagesCurrent Liabilities ManagementAndrew Usatii100% (2)

- Practice Questions 9Document3 pagesPractice Questions 9Nevaeh LeeNo ratings yet

- CH07Document32 pagesCH07asflkhaf2No ratings yet

- Rupali BankDocument94 pagesRupali BankRingkonAlamNo ratings yet

- Chapter 8-Short Term FinancingDocument41 pagesChapter 8-Short Term FinancingEmmy AzmanNo ratings yet

- ch-1 SummryDocument3 pagesch-1 SummryGiven GivenNo ratings yet

- Sources of Short Term Funds HandoutDocument2 pagesSources of Short Term Funds HandoutRhea llyn BacquialNo ratings yet

- bài ôn tập cho vayDocument6 pagesbài ôn tập cho vayQuynh NguyenNo ratings yet

- Commercial Bank FunctionsDocument29 pagesCommercial Bank FunctionsMahesh RasalNo ratings yet

- Reading Advancing Functions of BankDocument2 pagesReading Advancing Functions of BankKim DungNo ratings yet

- Solution To Case 25 Accounts Receivable Management A Switch in Time Saves Nine What Are The Elements of A Good Credit PolicyDocument8 pagesSolution To Case 25 Accounts Receivable Management A Switch in Time Saves Nine What Are The Elements of A Good Credit Policyanika fierroNo ratings yet

- Termination of Bank-Customer RelationshipDocument5 pagesTermination of Bank-Customer Relationshipmuggzp100% (1)

- Week 5 Business LoansDocument34 pagesWeek 5 Business Loans23-08439No ratings yet

- Short Terrm Financing FinalDocument21 pagesShort Terrm Financing FinalAtika Gando SuriNo ratings yet

- Q 01Document1 pageQ 01Jatin PathakNo ratings yet

- Special Accounts For Banking Firm - M.com (BM) II Sem. - DR - Rajeshri DesaiDocument5 pagesSpecial Accounts For Banking Firm - M.com (BM) II Sem. - DR - Rajeshri DesaiOMARA BMF-2024100% (1)

- FM 1 Short Term FinancingDocument2 pagesFM 1 Short Term FinancingCrizhae OconNo ratings yet

- WC Management Short Term LiabilitiesDocument1 pageWC Management Short Term LiabilitiesMaica Jarie RiguaNo ratings yet

- HO No. 3 - Working Capital ManagementDocument2 pagesHO No. 3 - Working Capital ManagementGrace Chavez ManaliliNo ratings yet

- Working Capital Finance by BanksDocument37 pagesWorking Capital Finance by BanksPavan KumarNo ratings yet

- Debt Farming Report Dec 2011Document10 pagesDebt Farming Report Dec 2011Govan Law CentreNo ratings yet

- Solution:: Notes ReceivableDocument11 pagesSolution:: Notes ReceivableAnonymous 46mMVoNo ratings yet

- Chapter 8 - Short Term FinancingDocument45 pagesChapter 8 - Short Term FinancingCindy Jane Omillio100% (1)

- Lec. 4 - Debit Credit - PRMG 030Document15 pagesLec. 4 - Debit Credit - PRMG 030Ahmad SharaawyNo ratings yet

- 5Document2 pages5Potato MatoNo ratings yet

- PNB Registers 16.7% Growth, Aims Rs 10 Lakh Crore Turnover By2013Document8 pagesPNB Registers 16.7% Growth, Aims Rs 10 Lakh Crore Turnover By2013Anil DhankharNo ratings yet

- ReviewDocument3 pagesReviewEuneze LucasNo ratings yet

- Lecture On Nature of ReceivablesDocument3 pagesLecture On Nature of ReceivablesSara AlbinaNo ratings yet

- General BankingDocument59 pagesGeneral BankingKhaleda AkhterNo ratings yet

- Report On Working Capital Loan (Prime Bank)Document29 pagesReport On Working Capital Loan (Prime Bank)rrashadatt100% (3)

- FindingsDocument5 pagesFindingsafifNo ratings yet

- Functions of Banks I Primary and SecondaryDocument6 pagesFunctions of Banks I Primary and SecondaryAmace Placement KanchipuramNo ratings yet

- © FINANCE TRAINER International Introduction To Bank Management / Page 1 of 25Document25 pages© FINANCE TRAINER International Introduction To Bank Management / Page 1 of 25imic_2007No ratings yet

- Functions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsDocument3 pagesFunctions of Commercial Banks Commercial Banks Perform A Variety of Functions Which Can Be Divided AsBalaji GajendranNo ratings yet

- Banking-Law Notes11Document66 pagesBanking-Law Notes11BharatNo ratings yet

- FinMan Chapter 16 and 17 ProblemsDocument3 pagesFinMan Chapter 16 and 17 ProblemsJufel Ramirez100% (1)

- Analyzing Transactions in Service BusinessesDocument8 pagesAnalyzing Transactions in Service BusinessesUnamadable UnleomarableNo ratings yet

- Intern Ship Report OneDocument10 pagesIntern Ship Report Onefitsum kirosNo ratings yet

- Learning Objective 9-1: Chapter 9 ReceivablesDocument45 pagesLearning Objective 9-1: Chapter 9 ReceivablesMarqaz MarqazNo ratings yet

- What Is The Claims Calculator?Document3 pagesWhat Is The Claims Calculator?Robert PopNo ratings yet

- Sources of Finance - CreditDocument12 pagesSources of Finance - CreditSanta PinkaNo ratings yet

- 7e - Chapter 16Document65 pages7e - Chapter 16Lindsay SummersNo ratings yet

- Acca Fundamentals of Accounting (FA1)Document24 pagesAcca Fundamentals of Accounting (FA1)Paredes FlozerenziNo ratings yet

- Carrington Ltd's Switch to AfterpayDocument11 pagesCarrington Ltd's Switch to AfterpayKJSAdNo ratings yet

- Osborne Books Answer Sheet PDFDocument37 pagesOsborne Books Answer Sheet PDFBarışEgeUysalNo ratings yet

- 9new - 471233 - Learning Material - SMEDocument28 pages9new - 471233 - Learning Material - SMERavi KumarNo ratings yet

- Jiddeh Nidea-Selda, MBA Faculty Member, CBMADocument28 pagesJiddeh Nidea-Selda, MBA Faculty Member, CBMASteff ReodiqueNo ratings yet

- Computing commissions, down payments, and balancesDocument12 pagesComputing commissions, down payments, and balancesDearla BitoonNo ratings yet

- Cash and Marketable Securities Seatworks PDFDocument3 pagesCash and Marketable Securities Seatworks PDFGirl Lang AkoNo ratings yet

- Understanding Short-Term Financing OptionsDocument56 pagesUnderstanding Short-Term Financing OptionsQuendrick SurbanNo ratings yet

- Egypt Debtor PolicyDocument13 pagesEgypt Debtor PolicyKhaled SherifNo ratings yet

- 01 - Accounting For Trades and Other ReceivablesDocument5 pages01 - Accounting For Trades and Other ReceivablesCatherine CaleroNo ratings yet

- UST WC Finance With AnswersDocument11 pagesUST WC Finance With AnswersPauline Kisha Castro100% (1)

- Credit ManagmentDocument17 pagesCredit ManagmentKetan SonawaneNo ratings yet

- Template 1st 2prep P2Document6 pagesTemplate 1st 2prep P2asem shabanNo ratings yet

- The IASB and Global Harmonization of Accounting StandardsDocument19 pagesThe IASB and Global Harmonization of Accounting Standardsasem shabanNo ratings yet

- New Microsoft Word DocumentDocument1 pageNew Microsoft Word Documentasem shabanNo ratings yet

- Accounting For Hospital TransactionsDocument6 pagesAccounting For Hospital Transactionsasem shabanNo ratings yet

- Accounting For University's Transactions: The Last Two Items Only Were On CreditDocument5 pagesAccounting For University's Transactions: The Last Two Items Only Were On Creditasem shabanNo ratings yet

- 10 - Written Communication, Professional Writing Through CV and Interview Skills PDFDocument16 pages10 - Written Communication, Professional Writing Through CV and Interview Skills PDFhader elsaydNo ratings yet

- Plan & ReportDocument225 pagesPlan & Reportasem shabanNo ratings yet

- 3Document5 pages3asem shabanNo ratings yet

- ch26Document88 pagesch26asem shabanNo ratings yet

- Ch13 SMDocument12 pagesCh13 SMasem shabanNo ratings yet

- Accounting For University's Transactions: The Last Two Items Only Were On CreditDocument5 pagesAccounting For University's Transactions: The Last Two Items Only Were On Creditasem shabanNo ratings yet

- StudentDocument21 pagesStudentasem shabanNo ratings yet

- Horngren Ima16 Tif 17 GEDocument53 pagesHorngren Ima16 Tif 17 GEasem shabanNo ratings yet

- Accounting For Hospital TransactionsDocument6 pagesAccounting For Hospital Transactionsasem shabanNo ratings yet

- L1-Bank's Balance Sheet: Q2: Classify Each of The Following Accounts From The Bank's Point of ViewDocument4 pagesL1-Bank's Balance Sheet: Q2: Classify Each of The Following Accounts From The Bank's Point of Viewasem shabanNo ratings yet

- Horngren Ima16 Tif 07 GEDocument59 pagesHorngren Ima16 Tif 07 GEasem shaban100% (3)

- First Session - Fesability - 4th Y - EnglishDocument3 pagesFirst Session - Fesability - 4th Y - Englishasem shabanNo ratings yet

- AsemDocument10 pagesAsemasem shabanNo ratings yet

- Horngren Ima16 Tif 16 GEDocument47 pagesHorngren Ima16 Tif 16 GEasem shabanNo ratings yet

- Banking CH 01Document15 pagesBanking CH 01asem shabanNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument15 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesLordson RamosNo ratings yet

- Horngren Ima16 Tif 17 GEDocument53 pagesHorngren Ima16 Tif 17 GEasem shabanNo ratings yet

- Chapter 1 The Assurance Services Market: Auditing and Assurance Services, 15e, Global Edition (Arens)Document17 pagesChapter 1 The Assurance Services Market: Auditing and Assurance Services, 15e, Global Edition (Arens)asem shabanNo ratings yet

- Horngren Ima16 Tif 06 GEDocument59 pagesHorngren Ima16 Tif 06 GEasem shaban67% (3)

- Horngren Ima16 Tif 08 GEDocument49 pagesHorngren Ima16 Tif 08 GEasem shaban100% (3)

- Horngren Ima16 Tif 10 GEDocument50 pagesHorngren Ima16 Tif 10 GEasem shaban100% (2)

- Horngren Ima16 Tif 14 GEDocument72 pagesHorngren Ima16 Tif 14 GEasem shaban67% (3)

- Horngren Ima16 Tif 07 GEDocument59 pagesHorngren Ima16 Tif 07 GEasem shaban100% (3)

- Horngren Ima16 Tif 15 GEDocument49 pagesHorngren Ima16 Tif 15 GEasem shaban100% (1)

- A Project Report On Title: Submitted ByDocument15 pagesA Project Report On Title: Submitted ByChirag LaxmanNo ratings yet

- List Down The Terminologies Which Were Mentioned in The Movie and Define Each Based On Your Own Research and UnderstandingDocument5 pagesList Down The Terminologies Which Were Mentioned in The Movie and Define Each Based On Your Own Research and UnderstandingvonnevaleNo ratings yet

- Journal To Trial BalanceDocument20 pagesJournal To Trial BalanceJenny Valerie SualNo ratings yet

- Remitly Matteo MazzaDocument4 pagesRemitly Matteo MazzahkbiguivgNo ratings yet

- NBL Credit Management Internship ReportDocument65 pagesNBL Credit Management Internship ReportShamsuddin Ahmed43% (7)

- Middle East FundsDocument4 pagesMiddle East FundsAli Gokhan KocanNo ratings yet

- BSRM Steels LimitedDocument6 pagesBSRM Steels LimitedFossil FuelNo ratings yet

- XYZ Co Ltd Risk Matrix ReviewDocument42 pagesXYZ Co Ltd Risk Matrix ReviewAnupam BaliNo ratings yet

- Stauch USAADocument47 pagesStauch USAALeigh EganNo ratings yet

- Oona Corporate Profile - v16Document16 pagesOona Corporate Profile - v16PFMPC SecretaryNo ratings yet

- California Qui Tam False Claims Recording FeesDocument18 pagesCalifornia Qui Tam False Claims Recording Feesthorne1022No ratings yet

- Display Classified Ad RatesDocument6 pagesDisplay Classified Ad RatesaklatreaderNo ratings yet

- Hero Fincorp Ltd. Account Statement Generated On (Date & Time) :29/11/2022 04:27:41Document6 pagesHero Fincorp Ltd. Account Statement Generated On (Date & Time) :29/11/2022 04:27:41Raju BhaiNo ratings yet

- BPI Investment Corp V CADocument2 pagesBPI Investment Corp V CAJona Myka DugayoNo ratings yet

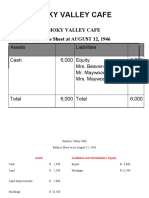

- Smoky Valley CafeDocument3 pagesSmoky Valley CafeRajkumar KrishnamoorthyNo ratings yet

- Cambridge IGCSE: Accounting 0452/22Document20 pagesCambridge IGCSE: Accounting 0452/22Valerine VictoriaNo ratings yet

- Audits of Voluntary Health and Welfare Organizations (1967) Indu PDFDocument74 pagesAudits of Voluntary Health and Welfare Organizations (1967) Indu PDFFate LauNo ratings yet

- Accounting equation computationsDocument8 pagesAccounting equation computationsMarjon DimafilisNo ratings yet

- Recruitment Selection31Document64 pagesRecruitment Selection31Nadeeha RiffaiNo ratings yet

- Guarantor Indemnity For Illness or DeathDocument2 pagesGuarantor Indemnity For Illness or Deathlajaun hindsNo ratings yet

- Embedded FinanceDocument31 pagesEmbedded FinanceHans100% (1)

- NATCOPHARM 29052023175546 AnnualSecreatarialComplianceReport29052023Document9 pagesNATCOPHARM 29052023175546 AnnualSecreatarialComplianceReport29052023kongarajaykumarNo ratings yet

- Receivables Financing ProblemsDocument2 pagesReceivables Financing ProblemsAdam CuencaNo ratings yet

- File: Chapter 05 - Consolidated Financial Statements - Intra-Entity Asset Transactions Multiple ChoiceDocument53 pagesFile: Chapter 05 - Consolidated Financial Statements - Intra-Entity Asset Transactions Multiple Choicejana ayoubNo ratings yet

- Ac GK CapsuleDocument280 pagesAc GK CapsuleRamesh SharmaNo ratings yet

- PrinciplesofFinance WEBDocument643 pagesPrinciplesofFinance WEBGLADYS JAMES100% (2)

- IFRS 15 Part 2 Perfomance Obligations Satisfied Over TimeDocument26 pagesIFRS 15 Part 2 Perfomance Obligations Satisfied Over TimeKiri chrisNo ratings yet

- H&M Balance Sheet and Income Statement AnalysisDocument7 pagesH&M Balance Sheet and Income Statement AnalysisHoàng TrâmNo ratings yet

- Mutual FundsDocument15 pagesMutual FundsMirchi RiyazNo ratings yet

- Intermediate Accounting Chapter 7 Exercises - ValixDocument26 pagesIntermediate Accounting Chapter 7 Exercises - ValixAbbie ProfugoNo ratings yet