You might also like

- CCM 120 April June CATDocument1 pageCCM 120 April June CATMuya KihumbaNo ratings yet

- The Kenya Institute of Management Certificate Course in Management Section 1 October - December 2016 Cat CCM 111: Principles of Accounts Question OneDocument2 pagesThe Kenya Institute of Management Certificate Course in Management Section 1 October - December 2016 Cat CCM 111: Principles of Accounts Question OneMuya KihumbaNo ratings yet

- CCM 111 Make Up Cat Oct Dec 16Document2 pagesCCM 111 Make Up Cat Oct Dec 16Muya KihumbaNo ratings yet

- Interest Rate Caps Around The WorldDocument39 pagesInterest Rate Caps Around The WorldMuya KihumbaNo ratings yet

- Frozenonthe RatesDocument8 pagesFrozenonthe RatesMuya KihumbaNo ratings yet

- Topic One Mathematical MethodsDocument7 pagesTopic One Mathematical MethodsMuya KihumbaNo ratings yet

- Topic One Mathematical MethodsDocument7 pagesTopic One Mathematical MethodsMuya KihumbaNo ratings yet

- Systems of Linear Equations and Augmented Matrices: SectionDocument19 pagesSystems of Linear Equations and Augmented Matrices: SectionMuya KihumbaNo ratings yet

- Intro To MatricesDocument19 pagesIntro To MatricesnandoNo ratings yet

- Intro MatrixDocument9 pagesIntro MatrixMuya KihumbaNo ratings yet

- The Impact of Capping Interest Rates On The Kenyan EconomyDocument3 pagesThe Impact of Capping Interest Rates On The Kenyan EconomyMuya KihumbaNo ratings yet

- Interest Rate Caps Around The WorldDocument39 pagesInterest Rate Caps Around The WorldMuya KihumbaNo ratings yet

- Baf 1101 Fa Cat TwoDocument4 pagesBaf 1101 Fa Cat TwoMuya KihumbaNo ratings yet

- The Case For An Interest Rate CapDocument27 pagesThe Case For An Interest Rate CapMuya KihumbaNo ratings yet

- Frozenonthe RatesDocument8 pagesFrozenonthe RatesMuya KihumbaNo ratings yet

- Maf 5102Document2 pagesMaf 5102Muya KihumbaNo ratings yet

- The Case For An Interest Rate CapDocument27 pagesThe Case For An Interest Rate CapMuya KihumbaNo ratings yet

- The Impact of Capping Interest Rates On The Kenyan EconomyDocument3 pagesThe Impact of Capping Interest Rates On The Kenyan EconomyMuya KihumbaNo ratings yet

- Book 1Document4 pagesBook 1Muya KihumbaNo ratings yet

- Maf5102 Fa Cat 2 2018Document4 pagesMaf5102 Fa Cat 2 2018Muya KihumbaNo ratings yet

- Maf 5102: Financial Management CAT 1 20 Marks Instructions Attempt All Questions Question OneDocument6 pagesMaf 5102: Financial Management CAT 1 20 Marks Instructions Attempt All Questions Question OneMuya KihumbaNo ratings yet

- Gross Profit/ (Loss) : (Assume Montly Salary Is 2,000)Document6 pagesGross Profit/ (Loss) : (Assume Montly Salary Is 2,000)Muya KihumbaNo ratings yet

- Baf 1101 Fa Cat OneDocument4 pagesBaf 1101 Fa Cat OneMuya KihumbaNo ratings yet

- Maf 5102Document2 pagesMaf 5102Muya KihumbaNo ratings yet

- Maf5101 Fa Cat 1 2018 1Document1 pageMaf5101 Fa Cat 1 2018 1Muya KihumbaNo ratings yet

- Maf 5102Document2 pagesMaf 5102Muya KihumbaNo ratings yet

- Bed 1101 Cat 1 MicroeconomicsDocument10 pagesBed 1101 Cat 1 MicroeconomicsMuya KihumbaNo ratings yet

- Maf 5102Document2 pagesMaf 5102Muya KihumbaNo ratings yet

- Law of AgencyDocument20 pagesLaw of AgencyMuya KihumbaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Understanding Consumer Preference For Coconut Sugar Using Conjoint Analysis Approach 121212Document5 pagesUnderstanding Consumer Preference For Coconut Sugar Using Conjoint Analysis Approach 121212Ralph Justin IINo ratings yet

- Utility and Demand: Answers To The Review QuizzesDocument16 pagesUtility and Demand: Answers To The Review QuizzesWeko CheangNo ratings yet

- Marketing Sales Operations in Chicago IL Resume Curt PetersonDocument3 pagesMarketing Sales Operations in Chicago IL Resume Curt PetersoncurtpetersonNo ratings yet

- Ch06 Solutions Manual 2015-07-16Document34 pagesCh06 Solutions Manual 2015-07-16Prema Khatwani KesariyaNo ratings yet

- Engineering Economy, 3rd Ed With SolutionDocument398 pagesEngineering Economy, 3rd Ed With SolutionJay Dalwadi100% (1)

- Crossword Marketing PricingBasics - KeyDocument1 pageCrossword Marketing PricingBasics - KeyShaikh GhaziNo ratings yet

- Modified Kuppuswamy Socioeconomic Scale 2022 UpdatDocument4 pagesModified Kuppuswamy Socioeconomic Scale 2022 UpdatShamNo ratings yet

- Concept of Business Profit Holding Gains/lossesDocument9 pagesConcept of Business Profit Holding Gains/lossesPutriNo ratings yet

- Chapter 9 - BudgetingDocument27 pagesChapter 9 - BudgetingPria JakartaNo ratings yet

- Cgse StatsDocument20 pagesCgse StatsChandu SagiliNo ratings yet

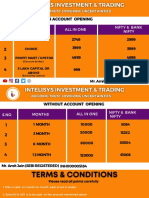

- Intelisys Pricing PlanDocument5 pagesIntelisys Pricing PlanregsNo ratings yet

- Case Study Abstract MC DonaldDocument2 pagesCase Study Abstract MC DonaldpradipkumarpatilNo ratings yet

- Case Problem 3Document21 pagesCase Problem 3Josh StevensNo ratings yet

- Fraction, Decimal and PercentDocument49 pagesFraction, Decimal and PercentTashaun NizodNo ratings yet

- DOVE FinalDocument27 pagesDOVE FinalAllen Keah100% (1)

- Anern Integrated Solar Garden Light-201604Document1 pageAnern Integrated Solar Garden Light-201604Godofredo VillenaNo ratings yet

- Security Analysis Paper For Wrigley and The Hershey CompanyDocument11 pagesSecurity Analysis Paper For Wrigley and The Hershey Companysegunpopoola1849100% (3)

- Economy PerformanceDocument16 pagesEconomy PerformanceMuhammad UmarNo ratings yet

- Absorption CostDocument2 pagesAbsorption Costsidra khanNo ratings yet

- Dynapac Soil CompactorsDocument20 pagesDynapac Soil CompactorsAchmad PrayogaNo ratings yet

- International Islamic University Islamabad Faculty of Management SciencesDocument10 pagesInternational Islamic University Islamabad Faculty of Management SciencesArslanNo ratings yet

- Bearish PatternsDocument41 pagesBearish PatternsKama Sae100% (1)

- Reinventing Metro Packet (9-19)Document42 pagesReinventing Metro Packet (9-19)CincinnatiEnquirerNo ratings yet

- 2013 Risk Premium Report Excerpt DP PDFDocument124 pages2013 Risk Premium Report Excerpt DP PDFJuan GSNo ratings yet

- Business Combination-Acquisition of Net AssetsDocument2 pagesBusiness Combination-Acquisition of Net AssetsMelodyLongakitBacatanNo ratings yet

- DiscountDocument4 pagesDiscountKartik BhargavaNo ratings yet

- Flash Boys Insider Perspective on HFTDocument131 pagesFlash Boys Insider Perspective on HFTPruthvish Shukla100% (1)

- Chelsea Parker 2442series HY25-2142-M1Document20 pagesChelsea Parker 2442series HY25-2142-M1Carlos Alberto Ramirez ParraNo ratings yet

- JP Morgan Best Equity Ideas 2014Document61 pagesJP Morgan Best Equity Ideas 2014Sara Lim100% (1)

- 6351 01 Que 20070118Document20 pages6351 01 Que 20070118Xin Ying LNo ratings yet