You might also like

- The Rise of States and The Age of CommerceDocument2 pagesThe Rise of States and The Age of CommerceMaria DevinaNo ratings yet

- The First Steps Towards National RevivalDocument2 pagesThe First Steps Towards National RevivalMaria DevinaNo ratings yet

- Popular Culture in Indonesia - Fluid Identity in Post-Authoritarian PoliticDocument2 pagesPopular Culture in Indonesia - Fluid Identity in Post-Authoritarian PoliticMaria DevinaNo ratings yet

- Quiz 1 KeyDocument1 pageQuiz 1 KeyMaria DevinaNo ratings yet

- Summary Week 2 - Maria Devina Sanjaya (392626)Document2 pagesSummary Week 2 - Maria Devina Sanjaya (392626)Maria DevinaNo ratings yet

- Not A Religious StateDocument2 pagesNot A Religious StateMaria DevinaNo ratings yet

- Pancasila and The Christians in IndonesiaDocument2 pagesPancasila and The Christians in IndonesiaMaria DevinaNo ratings yet

- Quiz 2 KeyDocument1 pageQuiz 2 KeyMaria DevinaNo ratings yet

- SecularismDocument2 pagesSecularismMaria DevinaNo ratings yet

- Quiz 3 KeyDocument1 pageQuiz 3 KeyMaria DevinaNo ratings yet

- 13 12 08 The International Ir Framework 2 1Document37 pages13 12 08 The International Ir Framework 2 1Egar PamujiNo ratings yet

- Sesi 13 Whistle Blowing SystemDocument26 pagesSesi 13 Whistle Blowing SystemMaria Devina100% (1)

- Practice Test A - StructureDocument6 pagesPractice Test A - StructureMichael Cruz RodríguezNo ratings yet

- Chapter 2-5Document15 pagesChapter 2-5Maria DevinaNo ratings yet

- Kunci PR 1Document6 pagesKunci PR 1Maria DevinaNo ratings yet

- Answer Case 3Document1 pageAnswer Case 3Maria DevinaNo ratings yet

- Questions CH 10Document4 pagesQuestions CH 10Maria DevinaNo ratings yet

- Baker Adhesives PaperDocument11 pagesBaker Adhesives PaperMaria DevinaNo ratings yet

- Case Week 5Document3 pagesCase Week 5Maria DevinaNo ratings yet

- Bagian ADocument3 pagesBagian AMaria DevinaNo ratings yet

- Toefl Reading 1Document2 pagesToefl Reading 1Maria DevinaNo ratings yet

- Uts Psa 2016Document4 pagesUts Psa 2016Maria DevinaNo ratings yet

- Summary Buat UASDocument5 pagesSummary Buat UASMaria DevinaNo ratings yet

- Flowchart KURANG LAKU - Maria Devina Sanjaya (392626)Document1 pageFlowchart KURANG LAKU - Maria Devina Sanjaya (392626)Maria DevinaNo ratings yet

- Fiscal Reconciliation ExerciseDocument1 pageFiscal Reconciliation ExerciseMaria DevinaNo ratings yet

- EFM2e, CH 07, Slides-1Document51 pagesEFM2e, CH 07, Slides-1Maria DevinaNo ratings yet

- Fiscal Reconciliation ExerciseDocument1 pageFiscal Reconciliation ExerciseMaria DevinaNo ratings yet

- EFM2e, CH 06, SlidesDocument21 pagesEFM2e, CH 06, SlidesMaria DevinaNo ratings yet

- EFM2e, CH 05, SlidesDocument16 pagesEFM2e, CH 05, SlidesMaria DevinaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Tax Invoice: Zomato Limited Address: Pan NoDocument1 pageTax Invoice: Zomato Limited Address: Pan NoAshwaniNo ratings yet

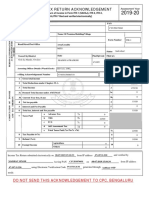

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruVikas MahorNo ratings yet

- Fesco Online Bill January 2Document1 pageFesco Online Bill January 2HaseebPirachaNo ratings yet

- Adobe Scan 21-Feb-2023Document2 pagesAdobe Scan 21-Feb-2023Pushpendra SinghNo ratings yet

- 2009 Tax Table 1040 1040NR For H1B, F1, J1, OPTDocument13 pages2009 Tax Table 1040 1040NR For H1B, F1, J1, OPTusvisataxesNo ratings yet

- Paper-Wise Exemptions On Reciprocal Basis To Icsi and Icwai StudentsDocument1 pagePaper-Wise Exemptions On Reciprocal Basis To Icsi and Icwai StudentsKarandeep Singh TuliNo ratings yet

- Tax Accountin 11Document3 pagesTax Accountin 11Muhammad Raihan AdzdzikrullohNo ratings yet

- Pocket Tax Book 2023Document120 pagesPocket Tax Book 2023Hary GunawanNo ratings yet

- Boat White Headphone BillDocument1 pageBoat White Headphone BillAvanish JaiswalNo ratings yet

- Accounting Officers Memo 2011 Revision Final January 2012 PDFDocument37 pagesAccounting Officers Memo 2011 Revision Final January 2012 PDFRosetta RennerNo ratings yet

- ReSA B42 TAX Final PB Exam Questions Answers Solutions PDFDocument17 pagesReSA B42 TAX Final PB Exam Questions Answers Solutions PDFNamnam KimNo ratings yet

- Intercontinental Broadcasting Corp. vs. Noemi B. Amarilla, Et Al., G.R. No. 162775, October 27, 2006Document2 pagesIntercontinental Broadcasting Corp. vs. Noemi B. Amarilla, Et Al., G.R. No. 162775, October 27, 2006xxxaaxxxNo ratings yet

- Annex A - Application Form BIR Form 2119Document2 pagesAnnex A - Application Form BIR Form 2119Antonio Reyes IVNo ratings yet

- Short Term CapitalDocument21 pagesShort Term CapitalGNR ASSOCIATESNo ratings yet

- Special Taxpayers Subject To Preferential Tax RatesDocument42 pagesSpecial Taxpayers Subject To Preferential Tax RatesErneylou RanayNo ratings yet

- Tax Quiz2 Answer KeyDocument5 pagesTax Quiz2 Answer Keycloy aubreyNo ratings yet

- Uncollected Social Security and Medicare Tax On WagesDocument2 pagesUncollected Social Security and Medicare Tax On Wagesnujahm1639No ratings yet

- Chapter 16Document22 pagesChapter 16KENTANG GORENGNo ratings yet

- SHAHID IQBAL'S LESCO BILLDocument1 pageSHAHID IQBAL'S LESCO BILLarsalan khanNo ratings yet

- Income Taxation Banggawan 2019 Ed Solution ManualDocument40 pagesIncome Taxation Banggawan 2019 Ed Solution Manualqwerty 130% (1)

- Fundamentals of VATDocument30 pagesFundamentals of VATNikhil YadavNo ratings yet

- NOLCODocument8 pagesNOLCOChristopher SantosNo ratings yet

- NSB Tax CalculatorDocument2 pagesNSB Tax CalculatorHassan RanaNo ratings yet

- BIR Ruling 05-90Document1 pageBIR Ruling 05-90Andrea RioNo ratings yet

- Pesco Online Bill 2Document1 pagePesco Online Bill 2salarabidjanNo ratings yet

- The University of Lahore: Regular Fee VoucherDocument1 pageThe University of Lahore: Regular Fee VoucherMuhammad ALINo ratings yet

- Fred Thompson Contribution FormDocument1 pageFred Thompson Contribution FormA. KleinheiderNo ratings yet

- Bigfoot 00476Document1 pageBigfoot 00476Akash AggarwalNo ratings yet

- Vighnaharta: Indirect TaxDocument99 pagesVighnaharta: Indirect Taxasmagolden313No ratings yet

- Taxation of interest income paid to foreign corporationsDocument1 pageTaxation of interest income paid to foreign corporationsCass CataloNo ratings yet