You might also like

- National Grid Energy Vision NYDocument32 pagesNational Grid Energy Vision NYTim KnaussNo ratings yet

- 81 Travel Time EstimatesDocument6 pages81 Travel Time EstimatesTim KnaussNo ratings yet

- Letter To President Biden On Ukraine RefugeesDocument1 pageLetter To President Biden On Ukraine RefugeesTim KnaussNo ratings yet

- Vaccination Rates by ZIP CodeDocument1 pageVaccination Rates by ZIP CodeTim KnaussNo ratings yet

- 12 Worst DealsDocument17 pages12 Worst DealsTim KnaussNo ratings yet

- Onondaga County DecisionDocument15 pagesOnondaga County DecisionTim KnaussNo ratings yet

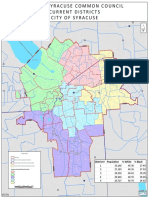

- Syracuse Council Districts MapDocument1 pageSyracuse Council Districts MapTim KnaussNo ratings yet

- The FEIS Executive Summary of The I-81 Viaduct ProjectDocument42 pagesThe FEIS Executive Summary of The I-81 Viaduct ProjectNewsChannel 9No ratings yet

- The FEIS Executive Summary of The I-81 Viaduct ProjectDocument42 pagesThe FEIS Executive Summary of The I-81 Viaduct ProjectNewsChannel 9No ratings yet

- Destiny OffensesDocument1 pageDestiny OffensesTim KnaussNo ratings yet

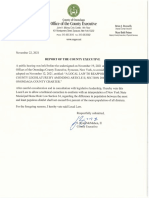

- Report of The County Executive 11-22-21Document1 pageReport of The County Executive 11-22-21Tim KnaussNo ratings yet

- B&L Sanitation Study 2.23.22Document12 pagesB&L Sanitation Study 2.23.22Tim KnaussNo ratings yet

- Onondaga County Police Reform PlanDocument59 pagesOnondaga County Police Reform PlanTim KnaussNo ratings yet

- FAQ On COBRA SubsidyDocument10 pagesFAQ On COBRA SubsidyTim KnaussNo ratings yet

- Attorney General James Releases Report On Nursing Homes' Response To COVID-19Document76 pagesAttorney General James Releases Report On Nursing Homes' Response To COVID-19News 8 WROCNo ratings yet

- Assembly Senate Response.2.10.21. Final PDFDocument16 pagesAssembly Senate Response.2.10.21. Final PDFZacharyEJWilliamsNo ratings yet

- Mayor Walsh Letter On Orange ZoneDocument2 pagesMayor Walsh Letter On Orange ZoneTim KnaussNo ratings yet

- TranscriptDocument3 pagesTranscriptNick Reisman100% (1)

- NYCLU Letter To OCSO Re COVID Restrictions at Justice Center - 12-24-2020Document3 pagesNYCLU Letter To OCSO Re COVID Restrictions at Justice Center - 12-24-2020Tim KnaussNo ratings yet

- LEO #19 (Signed) (37003)Document1 pageLEO #19 (Signed) (37003)Tim KnaussNo ratings yet

- Redistricting ResolutionDocument2 pagesRedistricting ResolutionTim KnaussNo ratings yet

- Veto MSG BOE Pay CutDocument2 pagesVeto MSG BOE Pay CutTim KnaussNo ratings yet

- Resolution To Roll Back Bail ReformDocument4 pagesResolution To Roll Back Bail ReformTim KnaussNo ratings yet

- Onondaga Zones OnlyDocument1 pageOnondaga Zones OnlyTim Knauss0% (1)

- DeWitt Warehouse EAFDocument48 pagesDeWitt Warehouse EAFTim KnaussNo ratings yet

- Ways & Means Budget ChangesDocument12 pagesWays & Means Budget ChangesTim KnaussNo ratings yet

- 2020 Poll Watcher Certificate GeneralDocument1 page2020 Poll Watcher Certificate GeneralTim KnaussNo ratings yet

- AEI Round 2 Allocation Recommendations ESDDocument3 pagesAEI Round 2 Allocation Recommendations ESDTim Knauss100% (2)

- 138 Brownfield PropertiesDocument4 pages138 Brownfield PropertiesTim KnaussNo ratings yet

- Brownfield PropertiesDocument5 pagesBrownfield PropertiesTim KnaussNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- REGULATORY FRAMEWORK FOR E-SABONGDocument8 pagesREGULATORY FRAMEWORK FOR E-SABONGKramier Haze HipolitoNo ratings yet

- Software Maintenance AgreementDocument4 pagesSoftware Maintenance AgreementAmardeep Singh HudaNo ratings yet

- NJGM Memo 2014-006Document8 pagesNJGM Memo 2014-006Office of the Student Regent, University of the PhilippinesNo ratings yet

- Ryanair Strategy Report: Daniel Geller Brendan Folan Brian Shain April 19, 2013Document28 pagesRyanair Strategy Report: Daniel Geller Brendan Folan Brian Shain April 19, 2013suongxuongnui100% (2)

- 67 Philippine Airlines, Inc. vs. EduDocument12 pages67 Philippine Airlines, Inc. vs. EduMary Joy JoniecaNo ratings yet

- Presentation On Abilities For Red Leaf Mortgages Neil WalshDocument3 pagesPresentation On Abilities For Red Leaf Mortgages Neil WalshlcdcomplaintNo ratings yet

- 1-2 Ex. H QWR Garry Smith, 17-80728, May 26, 2017Document21 pages1-2 Ex. H QWR Garry Smith, 17-80728, May 26, 2017larry-612445No ratings yet

- Past BillsDocument39 pagesPast BillsSal Salas100% (3)

- Fast Tag Application Form - 9 - 10 - 17 PDFDocument4 pagesFast Tag Application Form - 9 - 10 - 17 PDFMahesh badodkar100% (1)

- HighCourt Clerk HRYDocument7 pagesHighCourt Clerk HRYnareshjangra397No ratings yet

- RECONCILING THE BANK ACCOUNTDocument8 pagesRECONCILING THE BANK ACCOUNTSyed Adnan HossainNo ratings yet

- Gepco Online BillDocument2 pagesGepco Online Billroyalbutt413No ratings yet

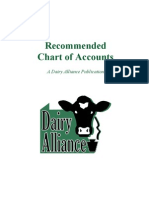

- Chart of Accounts - ImpDocument11 pagesChart of Accounts - Impravirambo_pNo ratings yet

- How Do I Speak To Someone at Copa AirlineDocument3 pagesHow Do I Speak To Someone at Copa AirlineskynairairlinesNo ratings yet

- Delhi-Haridwar-Rishikesh-Mussoorie-Auli TourDocument13 pagesDelhi-Haridwar-Rishikesh-Mussoorie-Auli TourRoshanNo ratings yet

- Fee StatementDocument4 pagesFee Statementchayemba.cheNo ratings yet

- Fleetwood Maritime Campus Senior Course ApplicationDocument7 pagesFleetwood Maritime Campus Senior Course ApplicationJeet SinghNo ratings yet

- Terms and Conditions Banquet EventDocument1 pageTerms and Conditions Banquet EventDeanna GarciaNo ratings yet

- Capital One, National Association vs. Jacob FrydmanDocument20 pagesCapital One, National Association vs. Jacob FrydmanJay100% (1)

- Loan Management of CBL - UshaDocument42 pagesLoan Management of CBL - UshaMd SalimNo ratings yet

- Card Transaction History and FeesDocument3 pagesCard Transaction History and FeesJEAN LAFORTUNENo ratings yet

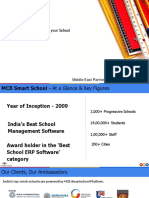

- The Operating System of your School ManagementDocument26 pagesThe Operating System of your School ManagementRejoy RadhakrishnanNo ratings yet

- Progress Michigan FOIA ProposalDocument18 pagesProgress Michigan FOIA ProposalMLive.comNo ratings yet

- Background:: Mind Mapperz and SAITMDocument4 pagesBackground:: Mind Mapperz and SAITMMohit SinghNo ratings yet

- Registration Guide: JANUARY 2017 SemesterDocument10 pagesRegistration Guide: JANUARY 2017 SemesterLynn LaiNo ratings yet

- HC MUD 180 Welcome Letter and Service FeesDocument3 pagesHC MUD 180 Welcome Letter and Service FeesMynette MalletNo ratings yet

- UA Checkliste VPD Verfahren enDocument3 pagesUA Checkliste VPD Verfahren enBharadwaja ReddyNo ratings yet

- Your Jazeera Airways Itinerary DetailsDocument2 pagesYour Jazeera Airways Itinerary DetailsKoteswar Mandava0% (1)

- 2T20202021 Tuition Fee Rates in FEUDocument16 pages2T20202021 Tuition Fee Rates in FEUAntoinette SangcapNo ratings yet