You might also like

- MME40001 Engineering Management 2 Sem1-2015 Unit of Study OutlineDocument9 pagesMME40001 Engineering Management 2 Sem1-2015 Unit of Study OutlineIbrahim HussainNo ratings yet

- Info3333: Computing 3 ManagementDocument4 pagesInfo3333: Computing 3 ManagementDarius ZhuNo ratings yet

- Unit - Guide - ACCG913 - 2016 - S2 EveningDocument19 pagesUnit - Guide - ACCG913 - 2016 - S2 Eveningadeel akramNo ratings yet

- FAR SYLLABUS FinalDocument13 pagesFAR SYLLABUS FinalUchiha WarrenNo ratings yet

- ACC202 - Managerial Accounting - Trimester 1 2024Document13 pagesACC202 - Managerial Accounting - Trimester 1 2024Huong Nguyen Thi XuanNo ratings yet

- FAR SYLLABUS FinalDocument13 pagesFAR SYLLABUS FinalUchiha WarrenNo ratings yet

- FAR SYLLABUS FinalDocument13 pagesFAR SYLLABUS FinalUchiha WarrenNo ratings yet

- ACCT6008 - Semester 2, 2021Document9 pagesACCT6008 - Semester 2, 2021Zhang RickNo ratings yet

- Fundamentals of Accountancy 1 SyllabusDocument8 pagesFundamentals of Accountancy 1 SyllabusronNo ratings yet

- School of Business Administration FIN330101: Principles of Finance Fall 2021 Course SyllabusDocument7 pagesSchool of Business Administration FIN330101: Principles of Finance Fall 2021 Course SyllabusHamza AmmadNo ratings yet

- PDBA Operations Course OutlineDocument12 pagesPDBA Operations Course OutlineQasim AbrahamsNo ratings yet

- UT Dallas Syllabus For Aim4336.501.07s Taught by Oktay Urcan (Oxu022000)Document7 pagesUT Dallas Syllabus For Aim4336.501.07s Taught by Oktay Urcan (Oxu022000)UT Dallas Provost's Technology GroupNo ratings yet

- Solution AnalysisDocument95 pagesSolution AnalysisRaluca UngureanuNo ratings yet

- Corporate Finance Essentials T1 2022Document10 pagesCorporate Finance Essentials T1 2022An Pham ThuyNo ratings yet

- USM Course Outline for Analysis of Financial StatementsDocument8 pagesUSM Course Outline for Analysis of Financial StatementsAndrian PratamaNo ratings yet

- ACCG340Document11 pagesACCG340Dung Tran0% (1)

- Assessment Pack BSBADM502 ODDocument10 pagesAssessment Pack BSBADM502 ODAyu PuspitaNo ratings yet

- ACCT4300 Students Unit Outline S223 KMKDocument9 pagesACCT4300 Students Unit Outline S223 KMKLincoln KendeNo ratings yet

- Philippine Business SyllabusDocument12 pagesPhilippine Business SyllabusLEXINE LOUISE NUBLANo ratings yet

- Acc707 Auditing and Assurance Services t116 GH 15 Feb 2015-FinalDocument11 pagesAcc707 Auditing and Assurance Services t116 GH 15 Feb 2015-FinalHaris AliNo ratings yet

- MSc in Climate Change Management & FinanceDocument9 pagesMSc in Climate Change Management & FinanceFrancisco Javier EspañaNo ratings yet

- General Guidelines:: ©IAS Placement Office DocumentDocument6 pagesGeneral Guidelines:: ©IAS Placement Office DocumentIqrä QurëshìNo ratings yet

- Syllabus Aku 3302 - Auditing 2Document6 pagesSyllabus Aku 3302 - Auditing 2alfianaNo ratings yet

- OFAD1001 - Syllabus ILACDocument4 pagesOFAD1001 - Syllabus ILACKrisha PatelNo ratings yet

- FINA 3710 SyllabusDocument4 pagesFINA 3710 SyllabusroBinNo ratings yet

- Course Information Summer Semester 2019/2020Document4 pagesCourse Information Summer Semester 2019/2020mmNo ratings yet

- 4 - Financial Management, Course Specification, Fall 2021Document6 pages4 - Financial Management, Course Specification, Fall 2021ASIMLIBNo ratings yet

- AF301 S2 - 2020 Course Outline V1Document6 pagesAF301 S2 - 2020 Course Outline V1Mithlesh Prasad100% (1)

- Project Code: SIP Project Title: Measuring The Performance of Commercial Papers RatingsDocument6 pagesProject Code: SIP Project Title: Measuring The Performance of Commercial Papers RatingsRAVI JAISWANI Student, Jaipuria IndoreNo ratings yet

- ACC 4203 Auditing (3 Credit Hours) : Section Instructor's Name Classroom, Time 1 Yoon Shik Han Yoon Shik HanDocument7 pagesACC 4203 Auditing (3 Credit Hours) : Section Instructor's Name Classroom, Time 1 Yoon Shik Han Yoon Shik HansirrikNo ratings yet

- Conceptual FrameworkDocument13 pagesConceptual FrameworkUchiha WarrenNo ratings yet

- Securities Analysis and Portfolio Management SyllabusDocument5 pagesSecurities Analysis and Portfolio Management Syllabusshilpa mishraNo ratings yet

- Jaipuria Institute of Management PGDM Trimester Ii Academic Year 2019-20Document9 pagesJaipuria Institute of Management PGDM Trimester Ii Academic Year 2019-20Sanjana SinghNo ratings yet

- CAR - DR G.SELVAGANAPAYTHY TAMIL II - BCOM GDocument15 pagesCAR - DR G.SELVAGANAPAYTHY TAMIL II - BCOM GSumathi NNo ratings yet

- FINA5120 - L6 - Fall2018 - Corporate Finance - Ekkachai SAENYASIRIDocument4 pagesFINA5120 - L6 - Fall2018 - Corporate Finance - Ekkachai SAENYASIRIalexander.cf.ipNo ratings yet

- Acct 621-45 Spring 2022 - Sarvir HothiDocument7 pagesAcct 621-45 Spring 2022 - Sarvir HothiVinay DanthuriNo ratings yet

- Personal Financial Planning and Manage EntDocument19 pagesPersonal Financial Planning and Manage EntJoseNo ratings yet

- Om 636 - Syllabus RevisedDocument5 pagesOm 636 - Syllabus RevisedNda-jiya SuberuNo ratings yet

- Final Report - Lynn MannDocument17 pagesFinal Report - Lynn Mannapi-371890611No ratings yet

- Car - Ed I B.com BDocument15 pagesCar - Ed I B.com BSumathi NNo ratings yet

- FINA 3710-91 CO F21 Abdool - Version2Document4 pagesFINA 3710-91 CO F21 Abdool - Version2Imran AbdoolNo ratings yet

- Guideline For Assessment SubmissionDocument21 pagesGuideline For Assessment SubmissionshaliniNo ratings yet

- ACC201 PA - UEH-ISB - S1 2019 - Unit Guide - Sent To LecturerDocument9 pagesACC201 PA - UEH-ISB - S1 2019 - Unit Guide - Sent To LecturerHa TranNo ratings yet

- Course Attainment Report MGNT ACC (II-A)Document15 pagesCourse Attainment Report MGNT ACC (II-A)Sumathi NNo ratings yet

- Financial Reporting and Analysis Course OverviewDocument7 pagesFinancial Reporting and Analysis Course OverviewBhai ho to dodoNo ratings yet

- Unit Outline: MKT20031 Marketing and InnovationDocument8 pagesUnit Outline: MKT20031 Marketing and InnovationShehry Vibes100% (1)

- Assessment Brief & RubricDocument9 pagesAssessment Brief & RubricPhuong ThaoNo ratings yet

- Developing Business Cases ProjectDocument45 pagesDeveloping Business Cases ProjectChriseth CruzNo ratings yet

- ACCT 215 - Introductory Financial Accounting I: Course DescriptionDocument5 pagesACCT 215 - Introductory Financial Accounting I: Course DescriptionJayden FrosterNo ratings yet

- Retirement FINA 702Document8 pagesRetirement FINA 702Telios AmbientesNo ratings yet

- Syllabus For Principles of Accounting IDocument8 pagesSyllabus For Principles of Accounting IJalexander26100% (1)

- Coursework FIN4274 AUGUST 2019 - DegreeDocument9 pagesCoursework FIN4274 AUGUST 2019 - DegreeYee Sin MeiNo ratings yet

- SIP GuidelinesDocument34 pagesSIP GuidelinesMayuri TetwarNo ratings yet

- UT Dallas Syllabus For Aim4336.521 06u Taught by Oktay Urcan (Oxu022000)Document7 pagesUT Dallas Syllabus For Aim4336.521 06u Taught by Oktay Urcan (Oxu022000)UT Dallas Provost's Technology GroupNo ratings yet

- Course Outline V1 - AuditingDocument3 pagesCourse Outline V1 - AuditingmoodiNo ratings yet

- DHSM 202 Ass 1 Training Proposal LO1 KVDM PreMod Compliant 180717Document7 pagesDHSM 202 Ass 1 Training Proposal LO1 KVDM PreMod Compliant 180717Slate WilsonNo ratings yet

- Jaipuria Institute of Management PGDM Trimester Ii Academic Year 2019-20Document10 pagesJaipuria Institute of Management PGDM Trimester Ii Academic Year 2019-20adarshNo ratings yet

- Student Handbook ACC3015 2018 - 19 DLDocument123 pagesStudent Handbook ACC3015 2018 - 19 DLThara DasanayakaNo ratings yet

- Nabu 404 2020 01 14Document5 pagesNabu 404 2020 01 14Sandhu SaabNo ratings yet

- Exam Cram Essentials Last-Minute Guide to Ace the PMP Exam: First EditionFrom EverandExam Cram Essentials Last-Minute Guide to Ace the PMP Exam: First EditionNo ratings yet

- Manage ReportDocument7 pagesManage ReportRafayel MarufNo ratings yet

- 1BUSN603 CGRM Assessment 2 Case Study Semester 1 2017Document6 pages1BUSN603 CGRM Assessment 2 Case Study Semester 1 2017Ṁysterious ṀarufNo ratings yet

- Career Development ManagementDocument30 pagesCareer Development ManagementRafayel MarufNo ratings yet

- Corporate Accounting Structure Due DateDocument1 pageCorporate Accounting Structure Due DateRafayel MarufNo ratings yet

- 40 Jenis Permainan Dalam Ruangan Untuk Diskusi.Document21 pages40 Jenis Permainan Dalam Ruangan Untuk Diskusi.Luqman HamidNo ratings yet

- Assignment 2Document3 pagesAssignment 2Rafayel MarufNo ratings yet

- A1. Just The FactsDocument14 pagesA1. Just The FactsRafayel MarufNo ratings yet

- 40 Icebreakers For Small GroupsDocument14 pages40 Icebreakers For Small GroupsRafayel MarufNo ratings yet

- Hochstrasser (Inspector of Taxes) V MayesDocument3 pagesHochstrasser (Inspector of Taxes) V MayesRafayel MarufNo ratings yet

- Donoghue Vs Stevenson 1932 AC 562Document1 pageDonoghue Vs Stevenson 1932 AC 562Rafayel MarufNo ratings yet

- Ch1 Accounting Information Systems An OverviewDocument19 pagesCh1 Accounting Information Systems An OverviewRafayel MarufNo ratings yet

- Ch1 Accounting Information Systems An OverviewDocument19 pagesCh1 Accounting Information Systems An OverviewRafayel MarufNo ratings yet

- PTE Essays-Emdad's PTE & IELTS PDFDocument22 pagesPTE Essays-Emdad's PTE & IELTS PDFRafayel MarufNo ratings yet

- Session 6 SlidesDocument15 pagesSession 6 SlidesRafayel MarufNo ratings yet

- School of Business - NSW Examination: Exam ConditionsDocument3 pagesSchool of Business - NSW Examination: Exam ConditionsRafayel MarufNo ratings yet

- Monetary Policy of BangladeshDocument9 pagesMonetary Policy of BangladeshRafayel MarufNo ratings yet

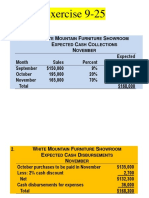

- Solution E9.25Document3 pagesSolution E9.25Rafayel MarufNo ratings yet

- Good Governance Guide: Risk Management OverviewDocument2 pagesGood Governance Guide: Risk Management OverviewRafayel MarufNo ratings yet

- Chapter 5Document46 pagesChapter 5Rafayel MarufNo ratings yet

- Bfile: Ch01, Chapter 1: The Role of Marketing Research in Management Decision MakingDocument8 pagesBfile: Ch01, Chapter 1: The Role of Marketing Research in Management Decision MakingOumaïma M'nounyNo ratings yet

- Envy, CWB, and Leadership Moderation in Public vs Private OrgsDocument8 pagesEnvy, CWB, and Leadership Moderation in Public vs Private OrgsAdroit WriterNo ratings yet

- Minerals: Design and Evaluation of An Expert System in A Crushing PlantDocument15 pagesMinerals: Design and Evaluation of An Expert System in A Crushing PlantLoven JannNo ratings yet

- Answ - Test 3Document7 pagesAnsw - Test 3Kristy LeeNo ratings yet

- Motivation LPDocument8 pagesMotivation LPShreekumarNo ratings yet

- K Means ExampleDocument10 pagesK Means ExampleDaljit SinghNo ratings yet

- For Andrew Kelsey PDFDocument5 pagesFor Andrew Kelsey PDFWayne A RoyceNo ratings yet

- Final Exam Sample TestDocument12 pagesFinal Exam Sample TestMinh ThưNo ratings yet

- AMP Check ListDocument8 pagesAMP Check ListCAM TAVNo ratings yet

- Continuing EducationDocument24 pagesContinuing EducationVijith.V.kumar100% (6)

- ML 43 Recruitment Selection and Induction Practice Ilm Assessment GuidanceDocument12 pagesML 43 Recruitment Selection and Induction Practice Ilm Assessment GuidanceAhmed UzairNo ratings yet

- CPF - Manual v1.0Document50 pagesCPF - Manual v1.0taikun_dtNo ratings yet

- Quality of Life in Older AgesDocument15 pagesQuality of Life in Older AgesAvina Anin NasiaNo ratings yet

- Microsoft Word - Deepanshu Internship ReportDocument61 pagesMicrosoft Word - Deepanshu Internship Reportdakshmehra217549100% (1)

- June 2017 CI Franklin Avenue Bridge ArticleDocument10 pagesJune 2017 CI Franklin Avenue Bridge ArticleFernando Castillo HerreraNo ratings yet

- Self Service TechnologyDocument27 pagesSelf Service TechnologyAngel Mae MeñozaNo ratings yet

- Audit Universe: Chartered Institute of Internal AuditorsDocument6 pagesAudit Universe: Chartered Institute of Internal AuditorsChen HanGuangNo ratings yet

- Quiz 1 RepairedDocument6 pagesQuiz 1 RepairedTran Pham Quoc ThuyNo ratings yet

- 2023-10-17 Letter To J Dinning From CPPIBDocument3 pages2023-10-17 Letter To J Dinning From CPPIBAdam ToyNo ratings yet

- P&S Unit-4 and 5Document3 pagesP&S Unit-4 and 5zzzzzNo ratings yet

- BSU-SC Tracer Study On The Employability of GraduatesDocument22 pagesBSU-SC Tracer Study On The Employability of GraduatesPerry Arcilla Serapio100% (1)

- Study ReadingDocument6 pagesStudy ReadingDian MirandaNo ratings yet

- 2014 AJO - Reliability of Upper Airway Linear, Area, and Volumetric Measurements in Cone-Beam Computed TomographyDocument10 pages2014 AJO - Reliability of Upper Airway Linear, Area, and Volumetric Measurements in Cone-Beam Computed Tomographydrgeorgejose7818No ratings yet

- (Routledge Focus - Disruptions - Studies in Digital Journalism) Steen Steensen, Oscar Westlund - What Is Digital Journalism Studies - Routledge - Taylor & Francis Group (2020)Document137 pages(Routledge Focus - Disruptions - Studies in Digital Journalism) Steen Steensen, Oscar Westlund - What Is Digital Journalism Studies - Routledge - Taylor & Francis Group (2020)Marcos Palacios100% (1)

- Alem BirhaneDocument78 pagesAlem Birhanebarkon desieNo ratings yet

- Hypothesis IDocument70 pagesHypothesis ILIM SIEW THIANGNo ratings yet

- SPE-177659-MS Field Development and Optimization Plan For Compartmentalized Oil Rim ReservoirDocument23 pagesSPE-177659-MS Field Development and Optimization Plan For Compartmentalized Oil Rim ReservoirDenis GontarevNo ratings yet

- Keller (2017) A Longitudinal Study of The Individual Characteristics of Effective R&D Project Team LeadersDocument14 pagesKeller (2017) A Longitudinal Study of The Individual Characteristics of Effective R&D Project Team LeadersGislayneNo ratings yet

- Importance and uses of surveying for civil engineersDocument34 pagesImportance and uses of surveying for civil engineersSagar SharmaNo ratings yet

- Webley POB SBADocument15 pagesWebley POB SBAkimona webley75% (8)