You might also like

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Status Report Example 021606110036 Status Report-ExampleDocument5 pagesStatus Report Example 021606110036 Status Report-ExampleAhmed Mohamed Khattab100% (2)

- PPE Cost MeasurementDocument5 pagesPPE Cost MeasurementRazel Tercino100% (1)

- PSBA - Property, Plant and EquipmentDocument13 pagesPSBA - Property, Plant and EquipmentAbdulmajed Unda MimbantasNo ratings yet

- 2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Document1 page2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Lyka Lim Pascua100% (1)

- Property Plant and EquipmentDocument13 pagesProperty Plant and EquipmentWilsonNo ratings yet

- IASb 16 Property, Plant EquipmentDocument32 pagesIASb 16 Property, Plant EquipmentIan chisema100% (1)

- Studet Practical Accounting Ch17 PPE AcquisitionDocument16 pagesStudet Practical Accounting Ch17 PPE Acquisitionsabina del monteNo ratings yet

- Property. Plant A: ' EquipmentDocument45 pagesProperty. Plant A: ' EquipmentLhene Angcon73% (11)

- Ias 16Document33 pagesIas 16Kiri chris100% (1)

- Chapter 17 - Ppe - AssignmentDocument16 pagesChapter 17 - Ppe - Assignmentsabina del monteNo ratings yet

- LLP NotesDocument8 pagesLLP NotesRajaNo ratings yet

- 17 Property Plant and Equipment PART 1 PDFDocument25 pages17 Property Plant and Equipment PART 1 PDFJay Aubrey PinedaNo ratings yet

- Property, Plant and Equipment IAS 16: Lacpa IFRS PresentationDocument31 pagesProperty, Plant and Equipment IAS 16: Lacpa IFRS PresentationKenncyNo ratings yet

- Chapter 8 Intangible AssetsDocument12 pagesChapter 8 Intangible AssetsKrissa Mae Longos100% (3)

- Module 7 - PAS 16 PPEDocument6 pagesModule 7 - PAS 16 PPEbladdor DG.No ratings yet

- Conceptual Framework: & Accounting StandardsDocument45 pagesConceptual Framework: & Accounting StandardsAmie Jane MirandaNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Farap 4504Document8 pagesFarap 4504Marya NvlzNo ratings yet

- Chapter-10 Acctg3226Document36 pagesChapter-10 Acctg3226Nadine SantosNo ratings yet

- AS 10 (Revised) : Property, Plant and EquipmentDocument34 pagesAS 10 (Revised) : Property, Plant and EquipmentAkshay PatilNo ratings yet

- Ind AS 16 - RBM (WBS)Document7 pagesInd AS 16 - RBM (WBS)KRISHNENDU JASHNo ratings yet

- PAS 16 PPE GuideDocument29 pagesPAS 16 PPE GuideArvin Garbo50% (2)

- PAS 16 - PPE - DiscussionDocument7 pagesPAS 16 - PPE - DiscussionRicaNo ratings yet

- Accounting for property, plant and equipmentDocument31 pagesAccounting for property, plant and equipmentRyou ShinodaNo ratings yet

- IPSAS 17. Property-Plant - EquipmentDocument28 pagesIPSAS 17. Property-Plant - EquipmentKibromWeldegiyorgisNo ratings yet

- AS 10 - Property Plant and Equipment: Recognition CriteriaDocument5 pagesAS 10 - Property Plant and Equipment: Recognition CriteriaAshutosh shriwasNo ratings yet

- 2022 06 DepreciationDocument46 pages2022 06 DepreciationSafi UllahNo ratings yet

- Property, Plant and Equipment: By: Maria Monica L. Dacullo BSA 1-Set CDocument17 pagesProperty, Plant and Equipment: By: Maria Monica L. Dacullo BSA 1-Set CMaria Monica DaculloNo ratings yet

- Property Plant Tutorials Number OneDocument46 pagesProperty Plant Tutorials Number OneNatalie SerranoNo ratings yet

- Lecture Notes On PPE - Acq & RecDocument6 pagesLecture Notes On PPE - Acq & Recjudel ArielNo ratings yet

- Property, Plant and Equipment (Pas 16)Document1 pageProperty, Plant and Equipment (Pas 16)Jhets CalumbayNo ratings yet

- ReviewerDocument5 pagesReviewercholestudyNo ratings yet

- PP&E accounting guidelinesDocument7 pagesPP&E accounting guidelinesJongseong ParkNo ratings yet

- Initial Measurement at Cost.: Property, Plant and EquipmentDocument5 pagesInitial Measurement at Cost.: Property, Plant and EquipmentCarms St ClaireNo ratings yet

- Ias 16 PpeDocument47 pagesIas 16 PpefitusNo ratings yet

- Lecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringDocument49 pagesLecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringZenyui100% (1)

- Ias 16Document31 pagesIas 16Reever RiverNo ratings yet

- ICAIEKM Material 180116Document57 pagesICAIEKM Material 180116INTER SMARTIANSNo ratings yet

- (H) - 3rd Year - BCH 6.4 (DSE-4) - Sem-6 - Financial Reporting and Analysis - Week 4 - Himani DahiyaDocument19 pages(H) - 3rd Year - BCH 6.4 (DSE-4) - Sem-6 - Financial Reporting and Analysis - Week 4 - Himani DahiyaARGHYA MANDALNo ratings yet

- MFRS 116 PPE - Part 1 NotesDocument24 pagesMFRS 116 PPE - Part 1 NotesWAN AMIRUL MUHAIMIN WAN ZUKAMALNo ratings yet

- IAS 16 GuideDocument100 pagesIAS 16 GuideClarkMaasNo ratings yet

- Ias 16Document20 pagesIas 16Jasmine LamugNo ratings yet

- AS10: Property, Plant and Equipment (Revised) : S6 Open Cou Rse DR - Sarin Thomas Modu Le 2 U Ni T 2 Pa RT 3Document12 pagesAS10: Property, Plant and Equipment (Revised) : S6 Open Cou Rse DR - Sarin Thomas Modu Le 2 U Ni T 2 Pa RT 3JohanNo ratings yet

- Fixed Assets IAS 16Document25 pagesFixed Assets IAS 16zulfi100% (2)

- FARAP 4404 Property Plant EquipmentDocument11 pagesFARAP 4404 Property Plant EquipmentJohn Ray RonaNo ratings yet

- Module 7 PPEDocument6 pagesModule 7 PPECha Eun WooNo ratings yet

- 3 Non-Current Assets TopicDocument43 pages3 Non-Current Assets TopicpesseNo ratings yet

- Ias 16Document5 pagesIas 16Edga WariobaNo ratings yet

- PAS 16 Property, Plant & Equipment ReviewDocument21 pagesPAS 16 Property, Plant & Equipment ReviewMakoy BixenmanNo ratings yet

- Accounting For Property, Plant & Equipment (Ppe) PAS 16Document44 pagesAccounting For Property, Plant & Equipment (Ppe) PAS 16Jay-L TanNo ratings yet

- A5 Audit of Ppe Part 1Document10 pagesA5 Audit of Ppe Part 1KezNo ratings yet

- 6904 PPT Materials For UploadDocument5 pages6904 PPT Materials For UploadAljur SalamedaNo ratings yet

- Far 006LN PDFDocument8 pagesFar 006LN PDFwingsenigma 00No ratings yet

- Mod.7 Property Plant and EquipmentDocument38 pagesMod.7 Property Plant and EquipmentCha Eun WooNo ratings yet

- Part D-8 Tangible non current assests (ch06)Document68 pagesPart D-8 Tangible non current assests (ch06)hyangNo ratings yet

- Chapter 8-2Document69 pagesChapter 8-2Joel Sam Bilji100% (1)

- Session # 17 Class MaterialDocument11 pagesSession # 17 Class MaterialTushar� SinghNo ratings yet

- IAS 16 PPE GuideDocument3 pagesIAS 16 PPE GuideRose MarieNo ratings yet

- Financial Accounting Chapter 9Document66 pagesFinancial Accounting Chapter 9Jihen SmariNo ratings yet

- Ias 16Document17 pagesIas 16david_thapaNo ratings yet

- This Short Story The Brahmin and His Enemies Is Quite Interesting To All The PeopleDocument2 pagesThis Short Story The Brahmin and His Enemies Is Quite Interesting To All The PeopleHimanshu Gaur100% (1)

- A Man Found A Cocoon of A ButterflyDocument2 pagesA Man Found A Cocoon of A ButterflyHimanshu GaurNo ratings yet

- I Woke One Morning and Realized Something AmazingDocument2 pagesI Woke One Morning and Realized Something AmazingHimanshu GaurNo ratings yet

- No Matter WhatDocument3 pagesNo Matter WhatHimanshu GaurNo ratings yet

- This Short Story The Arrogant Swans Is Quite Interesting To All The PeopleDocument2 pagesThis Short Story The Arrogant Swans Is Quite Interesting To All The PeopleHimanshu GaurNo ratings yet

- This Short Story The Clever Crow Is Quite Interesting To All The PeopleDocument3 pagesThis Short Story The Clever Crow Is Quite Interesting To All The PeopleHimanshu GaurNo ratings yet

- An Old Man Had Three SonsDocument2 pagesAn Old Man Had Three SonsHimanshu Gaur0% (1)

- This Short Story The Bonded Donkey Is Quite Interesting To All The PeopleDocument2 pagesThis Short Story The Bonded Donkey Is Quite Interesting To All The PeopleHimanshu GaurNo ratings yet

- SaseDocument3 pagesSaseHimanshu GaurNo ratings yet

- Tenali Raman and His Wife Were Going To A FriendDocument3 pagesTenali Raman and His Wife Were Going To A FriendHimanshu GaurNo ratings yet

- Jessica Seeks Help From Her Aunt For Parents' QuarrelsDocument3 pagesJessica Seeks Help From Her Aunt For Parents' QuarrelsHimanshu GaurNo ratings yet

- Two Twin Boys Were Raised by An Alcoholic FatherDocument2 pagesTwo Twin Boys Were Raised by An Alcoholic FatherHimanshu GaurNo ratings yet

- I Am Only 24 Years OldDocument3 pagesI Am Only 24 Years OldHimanshu GaurNo ratings yet

- One Calm NightDocument2 pagesOne Calm NightHimanshu GaurNo ratings yet

- Two Friends Were Walking Through The DesertDocument2 pagesTwo Friends Were Walking Through The DesertHimanshu GaurNo ratings yet

- The Cab Driver Picked Up His Passenger in The Dead of The NightDocument3 pagesThe Cab Driver Picked Up His Passenger in The Dead of The NightHimanshu GaurNo ratings yet

- SaseDocument3 pagesSaseHimanshu GaurNo ratings yet

- This Short Story Reward For Bravery Is Quite Interesting To All The PeopleDocument3 pagesThis Short Story Reward For Bravery Is Quite Interesting To All The PeopleHimanshu Gaur100% (1)

- Long AgoDocument1 pageLong AgoHimanshu GaurNo ratings yet

- Hotel Clerk's Act of Kindness Leads to Manager RoleDocument3 pagesHotel Clerk's Act of Kindness Leads to Manager RoleHimanshu GaurNo ratings yet

- Three monkeys go shopping in the cityDocument5 pagesThree monkeys go shopping in the cityHimanshu GaurNo ratings yet

- He Pushed His Wife To Save Himself From A Sinking Cruise ShipDocument2 pagesHe Pushed His Wife To Save Himself From A Sinking Cruise ShipHimanshu GaurNo ratings yet

- This Short Story Hercules Is Quite Interesting To All The PeopleDocument2 pagesThis Short Story Hercules Is Quite Interesting To All The PeopleHimanshu GaurNo ratings yet

- A Child's Excitement on a Stormy Sea VoyageDocument6 pagesA Child's Excitement on a Stormy Sea VoyageHimanshu GaurNo ratings yet

- Once Up A Time There Were Three LionsDocument5 pagesOnce Up A Time There Were Three LionsHimanshu GaurNo ratings yet

- This Short Story Louis Pasteur Is Quite Interesting To All The PeopleDocument3 pagesThis Short Story Louis Pasteur Is Quite Interesting To All The PeopleHimanshu GaurNo ratings yet

- Malar Lived at Keeranur Village in Pudukottai District With Her FamilyDocument2 pagesMalar Lived at Keeranur Village in Pudukottai District With Her FamilyHimanshu GaurNo ratings yet

- Father and SonDocument1 pageFather and SonHimanshu GaurNo ratings yet

- Improve Observation, Perception and Expression With MeditationDocument2 pagesImprove Observation, Perception and Expression With MeditationHimanshu GaurNo ratings yet

- There Was A Fight On The Sea Between England and FranceDocument2 pagesThere Was A Fight On The Sea Between England and FranceHimanshu GaurNo ratings yet

- KOKEBE TSIBAH 2021 Grade 12 Civics Work SheetDocument20 pagesKOKEBE TSIBAH 2021 Grade 12 Civics Work Sheetmmree yyttNo ratings yet

- Proposal HydrologyDocument4 pagesProposal HydrologyClint Sunako FlorentinoNo ratings yet

- Economic History of The PhilippinesDocument4 pagesEconomic History of The PhilippinesClint Agustin M. RoblesNo ratings yet

- User Exits in Sales Document ProcessingDocument9 pagesUser Exits in Sales Document Processingkirankumar723No ratings yet

- Strategic Management in Tourism 3rd Edition Chapter 3Document9 pagesStrategic Management in Tourism 3rd Edition Chapter 3Ringle JobNo ratings yet

- SolergyDocument3 pagesSolergyArsalan AhmedNo ratings yet

- Economics TopicsDocument2 pagesEconomics Topicsatif_ausaf100% (1)

- 7 Marketing Strategies of India Automobile CompaniesDocument7 pages7 Marketing Strategies of India Automobile CompaniesamritNo ratings yet

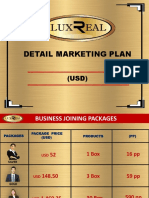

- Luxreal Detail Marketing Plan (2019) UsdDocument32 pagesLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Analysis Master RoadDocument94 pagesAnalysis Master RoadSachin KumarNo ratings yet

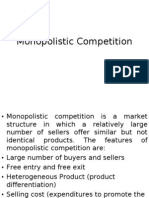

- Monopolistic CompetitionDocument14 pagesMonopolistic CompetitionRajesh GangulyNo ratings yet

- 20 Recent IELTS Graph Samples With AnswersDocument14 pages20 Recent IELTS Graph Samples With AnswersRizwan BashirNo ratings yet

- Inter-regional disparities in industrial growthDocument100 pagesInter-regional disparities in industrial growthrks_rmrctNo ratings yet

- Monopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineDocument36 pagesMonopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineNameNo ratings yet

- Customer Perception of Service Quality at Indian Overseas BankDocument96 pagesCustomer Perception of Service Quality at Indian Overseas BankRenjith K PushpanNo ratings yet

- Aviation ProjectDocument38 pagesAviation ProjectSomraj PathakNo ratings yet

- Airborne Express CaseDocument3 pagesAirborne Express Casehowlnmadmurphy2No ratings yet

- Jagath Nissanka,: Experience Key Roles and ResponsibilitiesDocument2 pagesJagath Nissanka,: Experience Key Roles and ResponsibilitiesJagath NissankaNo ratings yet

- IRCTCs e-Ticketing Service DetailsDocument2 pagesIRCTCs e-Ticketing Service DetailsOPrakash RNo ratings yet

- 10th March: by Dr. Gaurav GargDocument2 pages10th March: by Dr. Gaurav GarganupamNo ratings yet

- c6. Test 1. Listening. AnswerDocument5 pagesc6. Test 1. Listening. AnswerLê VinhNo ratings yet

- Signature Global Park 5 Apartment Details and Payment PlansDocument2 pagesSignature Global Park 5 Apartment Details and Payment Planssanyam ralliNo ratings yet

- ME Ch6 Wosabi09Document15 pagesME Ch6 Wosabi09Aamir Waseem0% (1)

- Phoenix Pallasio Lucknow Presentation 04-09-2019Document41 pagesPhoenix Pallasio Lucknow Presentation 04-09-2019T PatelNo ratings yet

- Price DispersionDocument4 pagesPrice DispersionAbel VasquezNo ratings yet

- Chapter One - Part 1Document21 pagesChapter One - Part 1ephremNo ratings yet

- Week 8Document2 pagesWeek 8Nikunj D Patel100% (1)