You might also like

- MCS of InfosysDocument7 pagesMCS of InfosysMunish PathaniaNo ratings yet

- Evolution of MISDocument4 pagesEvolution of MISHarshitha PadmashaliNo ratings yet

- Group 2-Transparency & DisclosureDocument12 pagesGroup 2-Transparency & DisclosureSoo CealNo ratings yet

- "An Individual Assesse Is Allowed To Get Tax Rebate On Certain Investment"-Explain. 4Document3 pages"An Individual Assesse Is Allowed To Get Tax Rebate On Certain Investment"-Explain. 4Shawon SarkerNo ratings yet

- Accounting Practices in Bangladesh: A Study On Kazi FarmsDocument19 pagesAccounting Practices in Bangladesh: A Study On Kazi FarmsMehedi HasanNo ratings yet

- ONIDADocument4 pagesONIDARebecca Martin0% (1)

- SMU MBA101 - Management Process and Organizational Behaviour Free Solved AssignmentDocument9 pagesSMU MBA101 - Management Process and Organizational Behaviour Free Solved Assignmentrahulverma2512100% (1)

- An Overview of Business ProcessDocument22 pagesAn Overview of Business Processalemayehu100% (1)

- Case Study - 1 & 2Document3 pagesCase Study - 1 & 2Hasibul Ashraf67% (3)

- Final Report of Soneri BankDocument24 pagesFinal Report of Soneri Banksanashk0% (1)

- Accounting For LabourDocument10 pagesAccounting For LabourTaleem Tableeg100% (1)

- The Four Models of Corporate EntrepreneurshipDocument16 pagesThe Four Models of Corporate EntrepreneurshipAlfred Kiruba RajNo ratings yet

- Chap016 TNx2Document89 pagesChap016 TNx2Atif SaeedNo ratings yet

- IntroductionDocument11 pagesIntroductionSagar KapoorNo ratings yet

- Tutorial 3-Stu Suggested AnsDocument4 pagesTutorial 3-Stu Suggested AnsAlan KhorNo ratings yet

- Chapter020 Solutions Manuall 2 PDFDocument29 pagesChapter020 Solutions Manuall 2 PDFleoyay50% (2)

- Basic Management Accounting ConceptsDocument28 pagesBasic Management Accounting ConceptsAmanda100% (2)

- Capital Budgeting NPV Case Study: Retail Fashion StoreDocument2 pagesCapital Budgeting NPV Case Study: Retail Fashion StoreAnand Prakash Sharma100% (1)

- Performance Appraisal System of Bangladesh Abashan LtdDocument48 pagesPerformance Appraisal System of Bangladesh Abashan LtdFahimNo ratings yet

- CASE 30 Tesla MotorsDocument15 pagesCASE 30 Tesla MotorsPurna WayanNo ratings yet

- Group No 10 HRIS AssignmentDocument8 pagesGroup No 10 HRIS AssignmentWinifridaNo ratings yet

- Student Roll Number ListDocument21 pagesStudent Roll Number ListPayal PatelNo ratings yet

- Performance Management Analysis Standard Chartered BankDocument10 pagesPerformance Management Analysis Standard Chartered BankMadridista KroosNo ratings yet

- T & D Case Study of NestleDocument4 pagesT & D Case Study of NestleShivani BoseNo ratings yet

- Dr. SchekterDocument5 pagesDr. SchekterRaja Shaban Qamer Mukhlis100% (1)

- Functions of MISDocument2 pagesFunctions of MISSK LashariNo ratings yet

- Chapter - General Journal 4Document32 pagesChapter - General Journal 4Israr AhmedNo ratings yet

- Banasthali Vidyapeeth Hrds Assignment 2 Submitted By: Muskan Saxena 2045167 (WBMBA2000 7) Batch A1, Mba Semester 2Document4 pagesBanasthali Vidyapeeth Hrds Assignment 2 Submitted By: Muskan Saxena 2045167 (WBMBA2000 7) Batch A1, Mba Semester 2muskanNo ratings yet

- Activity-Based Costing and Activity-Based Management: Undercosting/Overcosting ExampleDocument11 pagesActivity-Based Costing and Activity-Based Management: Undercosting/Overcosting ExampleFAEETNo ratings yet

- Decisions Involving Alternative ChoicesDocument3 pagesDecisions Involving Alternative ChoicesHimani Meet JadavNo ratings yet

- Exercise On CapacityDocument2 pagesExercise On CapacityNino Natradze100% (1)

- Concept of Responsibility CentreDocument5 pagesConcept of Responsibility Centrevijayadarshini vNo ratings yet

- MIS AssignmentDocument1 pageMIS AssignmentTalila Sida100% (2)

- HR Case StudyDocument7 pagesHR Case StudyNesreen RaghebNo ratings yet

- Case Study 3 - Janssen-Cilag Wiki Solution: MBA FT-7601 Managing E-BusinessDocument5 pagesCase Study 3 - Janssen-Cilag Wiki Solution: MBA FT-7601 Managing E-BusinessAayush GoyalNo ratings yet

- Analysis of Crown Point Cabinetry-By Group JDocument2 pagesAnalysis of Crown Point Cabinetry-By Group Jvinayak1511No ratings yet

- Advantages Disadvantages Information System MISDocument2 pagesAdvantages Disadvantages Information System MISNurul Hawa100% (2)

- Rise of Extreme JobsDocument1 pageRise of Extreme JobsVishnu Raj57% (7)

- Chapter 9 Making Capital Investment DecisionsDocument32 pagesChapter 9 Making Capital Investment Decisionsiyun KNNo ratings yet

- Compensation PDFDocument260 pagesCompensation PDFruchit gupta100% (2)

- KPTM SMPDocument2 pagesKPTM SMPdrbobhcNo ratings yet

- Case Study - Week 6Document1 pageCase Study - Week 6Alexander Hernandez100% (1)

- MBSA1523 Managerial Economics Group 4 Presentation 1 PPT SlidesDocument21 pagesMBSA1523 Managerial Economics Group 4 Presentation 1 PPT SlidesPIONG MENG ZIAN MBS211233No ratings yet

- Lincoln Electric's Unique Management System Drives ProductivityDocument6 pagesLincoln Electric's Unique Management System Drives ProductivityKeresh HallNo ratings yet

- Lecture 13 14Document2 pagesLecture 13 14Ali Optimistic0% (1)

- SamaraDocument3 pagesSamaraRAsel FaRuqueNo ratings yet

- HRM Case Test 1 PDFDocument5 pagesHRM Case Test 1 PDFVinodshankar BhatNo ratings yet

- Chapter-I: Management System. We Understand That Payroll Management Systemin Not A Product To BeDocument22 pagesChapter-I: Management System. We Understand That Payroll Management Systemin Not A Product To BeShankarNo ratings yet

- Managing Personal CommunicationsDocument10 pagesManaging Personal CommunicationsPY SorianoNo ratings yet

- Capital StructureDocument4 pagesCapital StructureNaveen GurnaniNo ratings yet

- Proposal For Mba 4th Sem - Job Analysis and DesignDocument8 pagesProposal For Mba 4th Sem - Job Analysis and DesignbijayNo ratings yet

- Zimbra Zooms AheadDocument13 pagesZimbra Zooms Aheaduswakhan100% (3)

- Chapter 4 Job AnalysisDocument17 pagesChapter 4 Job AnalysisAbir AhmedNo ratings yet

- Principle of Auditing AssignmentDocument6 pagesPrinciple of Auditing AssignmentranjinikpNo ratings yet

- Understanding Process CostingDocument30 pagesUnderstanding Process CostingJehan MahmudNo ratings yet

- Chapter 3 SolutionsDocument72 pagesChapter 3 SolutionsAshishpal SinghNo ratings yet

- Write Up Zakaria SirDocument14 pagesWrite Up Zakaria Sirdinar aimcNo ratings yet

- MTP Case Analysis 1. Bharat Engineering Works Limited: 2. The Assistant Business ManagerDocument12 pagesMTP Case Analysis 1. Bharat Engineering Works Limited: 2. The Assistant Business ManagerMelsew BelachewNo ratings yet

- Notes On Small Scale IndustriesDocument19 pagesNotes On Small Scale IndustriesAli SaifyNo ratings yet

- ControllingDocument51 pagesControllingParul KhannaNo ratings yet

- Chapter 12 Establishing A Code of Ethics and Ethical GuidelinesDocument21 pagesChapter 12 Establishing A Code of Ethics and Ethical GuidelinesNiz IsmailNo ratings yet

- Fall 2013 BES CH 03Document25 pagesFall 2013 BES CH 03geenah111No ratings yet

- MyQUEST 20162017 RATING RESULT SOCIAL SCIENCES, BUSINESS & LAWDocument7 pagesMyQUEST 20162017 RATING RESULT SOCIAL SCIENCES, BUSINESS & LAWNiz IsmailNo ratings yet

- Immigrant and Refugee Families: Global Perspectives On Displacement and Resettlement ExperiencesDocument224 pagesImmigrant and Refugee Families: Global Perspectives On Displacement and Resettlement ExperiencesNiz IsmailNo ratings yet

- ACC2124 Mid-Term Test S2/17Document2 pagesACC2124 Mid-Term Test S2/17Niz IsmailNo ratings yet

- Bias, Prejudice, Stereotype, and DiscriminationDocument8 pagesBias, Prejudice, Stereotype, and DiscriminationNiz IsmailNo ratings yet

- Job Description Safety & HealthDocument1 pageJob Description Safety & HealthNiz IsmailNo ratings yet

- Chapter 1 The Foundation of Ethical ThoughtDocument32 pagesChapter 1 The Foundation of Ethical ThoughtNiz IsmailNo ratings yet

- Understanding Business Ethics: First EditionDocument15 pagesUnderstanding Business Ethics: First EditionNiz IsmailNo ratings yet

- Impromptu ListingDocument14 pagesImpromptu ListingNiz IsmailNo ratings yet

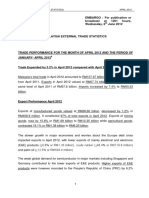

- Trade Performance For The Month of April 2012 and The Period of January - April 2012Document12 pagesTrade Performance For The Month of April 2012 and The Period of January - April 2012Niz IsmailNo ratings yet

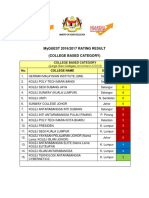

- MyQUEST 20162017 RATING RESULT - COLLEGE BASEDDocument11 pagesMyQUEST 20162017 RATING RESULT - COLLEGE BASEDNiz IsmailNo ratings yet

- Managing Diversity in The WorkplaceDocument2 pagesManaging Diversity in The WorkplaceNiz IsmailNo ratings yet

- Principles of Marketing and StrategyDocument24 pagesPrinciples of Marketing and StrategyNiz IsmailNo ratings yet

- Daniels Ib13 02Document30 pagesDaniels Ib13 02akmohideenNo ratings yet

- A Millenial's View of Diversity and Inclusion PDFDocument1 pageA Millenial's View of Diversity and Inclusion PDFNiz IsmailNo ratings yet

- Daniels Ib13 01Document19 pagesDaniels Ib13 01Nitin DhimanNo ratings yet

- Diversity in The WorkplaceDocument2 pagesDiversity in The WorkplaceNiz IsmailNo ratings yet

- Chapter 9 Foundations of ControlDocument34 pagesChapter 9 Foundations of ControlNiz IsmailNo ratings yet

- Chapter 7 Understanding Groups and Work TeamsDocument33 pagesChapter 7 Understanding Groups and Work TeamsNiz IsmailNo ratings yet

- Chapter 3 Integrative Managerial IssuesDocument38 pagesChapter 3 Integrative Managerial IssuesNiz IsmailNo ratings yet

- Chapter 6 Organizational Structure and DesignDocument45 pagesChapter 6 Organizational Structure and DesignNiz Ismail100% (1)

- Chapter 1 Managers and OrganizationDocument27 pagesChapter 1 Managers and OrganizationNiz IsmailNo ratings yet

- Chapter 5 Foundations of PlanningDocument31 pagesChapter 5 Foundations of PlanningNiz Ismail0% (1)

- Chapter 2 The Management EnvironmentDocument23 pagesChapter 2 The Management EnvironmentNiz IsmailNo ratings yet

- Com2114 MT QDocument1 pageCom2114 MT QNiz IsmailNo ratings yet

- Chapter 4 Foundations of Decision MakingDocument26 pagesChapter 4 Foundations of Decision MakingNiz IsmailNo ratings yet

- Lecture 1 - The Entrepreneurial Mind: Crafting A Personal Entrepreneurial StrategyDocument49 pagesLecture 1 - The Entrepreneurial Mind: Crafting A Personal Entrepreneurial StrategyNiz IsmailNo ratings yet

- Section A (TOTAL: 100 MARKS) Answer ALL Questions. Please Read and Answer Each Question CarefullyDocument3 pagesSection A (TOTAL: 100 MARKS) Answer ALL Questions. Please Read and Answer Each Question CarefullyNiz IsmailNo ratings yet

- Barriers To Learning Assignment SheetDocument3 pagesBarriers To Learning Assignment SheetAcid_Bath76No ratings yet

- English For Computer The Benefits of A Computer: Author: Yusuf Assya Bani Adam 41518010005Document10 pagesEnglish For Computer The Benefits of A Computer: Author: Yusuf Assya Bani Adam 41518010005Yusuf AsyaNo ratings yet

- Management Information Systems - Laudon - SummaryDocument92 pagesManagement Information Systems - Laudon - SummaryBirte Reiter91% (32)

- Federal Info Policy ExplainedDocument23 pagesFederal Info Policy ExplainedeonekeyNo ratings yet

- Design of Energy Consumption Monitoring and Energy Saving ManagementDocument3 pagesDesign of Energy Consumption Monitoring and Energy Saving ManagementFirma PurbantoroNo ratings yet

- Consumer BehaviourDocument27 pagesConsumer BehaviourSatyajeet SumanNo ratings yet

- Cdec1411-Early Childhood EducationDocument7 pagesCdec1411-Early Childhood Educationclara dupitasNo ratings yet

- Teacher Roles PDFDocument8 pagesTeacher Roles PDFGilberto MaldonadoNo ratings yet

- Huawei 3g ParametersDocument201 pagesHuawei 3g ParametersBilal Asif100% (2)

- Priority Sector Report: Digital IndustriesThe title provides a concise, SEO-optimized title for the given document:TITLE Report on Key Trends in Europe's Digital Industries SectorDocument20 pagesPriority Sector Report: Digital IndustriesThe title provides a concise, SEO-optimized title for the given document:TITLE Report on Key Trends in Europe's Digital Industries Sectorreza faghihiNo ratings yet

- APM Short NotesDocument41 pagesAPM Short Notesvaswanisid03No ratings yet

- Information Security Thesis ExamplesDocument5 pagesInformation Security Thesis Examplesafkololop100% (2)

- M3c Reporting Findings (Student Version) (Updated Aug 2020)Document25 pagesM3c Reporting Findings (Student Version) (Updated Aug 2020)You RanNo ratings yet

- B Com 105Document250 pagesB Com 105dihuNo ratings yet

- 325 Lecture Quiz 3Document7 pages325 Lecture Quiz 3JoyluxxiNo ratings yet

- South Africa 2014/15 Potato Industry ReportDocument122 pagesSouth Africa 2014/15 Potato Industry ReportGRAMYA Pvt Ltd.No ratings yet

- Extending AppsDocument14 pagesExtending AppskiranNo ratings yet

- Academic Staff and Researchers UseDocument21 pagesAcademic Staff and Researchers UseKrishia Sol LibradoNo ratings yet

- Seadrill Investor Presentation FINALDocument26 pagesSeadrill Investor Presentation FINALFreddy ReyesNo ratings yet

- 6130 Coursework Handbook (For Examination From 2020)Document37 pages6130 Coursework Handbook (For Examination From 2020)kitty christina winstonNo ratings yet

- Form 990 Information Gathering Account Opening Form 2023Document4 pagesForm 990 Information Gathering Account Opening Form 2023Geney BothaNo ratings yet

- Update and Document Operational Procedure-FinalDocument16 pagesUpdate and Document Operational Procedure-Finalmohammed ahmed80% (5)

- IC ToolkitDocument29 pagesIC ToolkitFelix DragoiNo ratings yet

- Finma 4 Prelim ResearchDocument10 pagesFinma 4 Prelim Researchfrescy mosterNo ratings yet

- Journal of CyberTherapy and Rehabilitation, Volume 2, Issue 4, 2009Document100 pagesJournal of CyberTherapy and Rehabilitation, Volume 2, Issue 4, 2009Giuseppe Riva100% (1)

- Hmi MP277 Operating Instructions en-US en-USDocument308 pagesHmi MP277 Operating Instructions en-US en-USjohn.thornley5775No ratings yet

- Barrett's and Bloom's TaxonomyDocument10 pagesBarrett's and Bloom's Taxonomygpl143No ratings yet

- Com202 - Writing For Media Book NotesDocument4 pagesCom202 - Writing For Media Book Notesj_claflin100% (3)

- GB922 Addendum 5LR Logical Resource R9 0 V9-3Document351 pagesGB922 Addendum 5LR Logical Resource R9 0 V9-3youssef MCHNo ratings yet

- Bosman Et Al-2016-British Journal of Educational TechnologyDocument10 pagesBosman Et Al-2016-British Journal of Educational TechnologyLucía CironaNo ratings yet