You might also like

- S 4 Hana Overview - PDF CatalogueDocument17 pagesS 4 Hana Overview - PDF CatalogueSayantani Bhattacharya0% (1)

- Strategy & Strategic PlanningDocument9 pagesStrategy & Strategic PlanningThe Natak CompanyNo ratings yet

- Strategies of Persuasion With Gary Orren PDFDocument3 pagesStrategies of Persuasion With Gary Orren PDFchevistarNo ratings yet

- Activity Based Costing Practice Problems ExplainedDocument7 pagesActivity Based Costing Practice Problems ExplainedRorNo ratings yet

- Project Finance: Aditya Agarwal Sandeep KaulDocument96 pagesProject Finance: Aditya Agarwal Sandeep Kaulsguha123No ratings yet

- Hotel Management 100+ Excel ProgramsDocument3 pagesHotel Management 100+ Excel ProgramsaalesandraNo ratings yet

- Loyalty Marketing & Loyal CustomersDocument17 pagesLoyalty Marketing & Loyal Customerssushildas2990% (1)

- Strategic Cost Management QuizDocument10 pagesStrategic Cost Management QuizMelanie SamsonaNo ratings yet

- Credit Scoring: Beyond The NumbersDocument34 pagesCredit Scoring: Beyond The NumbersramssravaniNo ratings yet

- KREDIVO MARKET RESEARCHDocument86 pagesKREDIVO MARKET RESEARCHMikhael Gracius67% (3)

- Credit Derivatives PrimerDocument32 pagesCredit Derivatives PrimerRyan YouNo ratings yet

- Consumer Lending in IndiaDocument25 pagesConsumer Lending in IndiaGautamNo ratings yet

- Dessler Hrm16 PPT 09Document41 pagesDessler Hrm16 PPT 09Khang Ngô Hoàng NgọcNo ratings yet

- The Design of Micro Credit Contracts and Micro Enterprise Finance in UgandaFrom EverandThe Design of Micro Credit Contracts and Micro Enterprise Finance in UgandaNo ratings yet

- CrowdForce - Pitch Deck 22.04.21Document22 pagesCrowdForce - Pitch Deck 22.04.21thiwa karanNo ratings yet

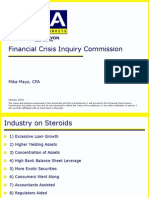

- Financial Crisis Inquiry Commission: Mike Mayo, CFADocument14 pagesFinancial Crisis Inquiry Commission: Mike Mayo, CFAosmar92387No ratings yet

- Sesi 2-1 Indivara - Risk in Financing Multifinance Company v1.4Document15 pagesSesi 2-1 Indivara - Risk in Financing Multifinance Company v1.4Nur Ulfawati HadiNo ratings yet

- Macroeconomic (Saving and Investment)Document110 pagesMacroeconomic (Saving and Investment)Sheillie KirklandNo ratings yet

- Consumer Lending in IndiaDocument22 pagesConsumer Lending in IndiadeepakNo ratings yet

- (FiinRatings) Corporate BondsDocument31 pages(FiinRatings) Corporate BondsTrần Thị Hà MyNo ratings yet

- Beams Aa13e PPT 18Document44 pagesBeams Aa13e PPT 18Brianna GilharryNo ratings yet

- Advanced Accounting: Corporate Liquidations and ReorganizationsDocument43 pagesAdvanced Accounting: Corporate Liquidations and ReorganizationsitaNo ratings yet

- Retail Lending: in A Post Covid WorldDocument24 pagesRetail Lending: in A Post Covid WorldAbhishek JaiswalNo ratings yet

- The Subprime & India: PresentersDocument30 pagesThe Subprime & India: Presentersgauravsurana213065100% (2)

- Banking Basics: Classification, Advances, NPAs, Deposits & Basel 3 NormsDocument26 pagesBanking Basics: Classification, Advances, NPAs, Deposits & Basel 3 NormsDev DugarNo ratings yet

- Will Credit Help The U.S. Consumer in H2-2014?: Economics GroupDocument6 pagesWill Credit Help The U.S. Consumer in H2-2014?: Economics Groupchatuuuu123No ratings yet

- Tracking How Small Finance Banks Advance Financial InclusionDocument30 pagesTracking How Small Finance Banks Advance Financial InclusionNeelanjan MaitiNo ratings yet

- Ing Musharakah by Muhammad Shaheed KhanDocument20 pagesIng Musharakah by Muhammad Shaheed KhanShammo SagaNo ratings yet

- Credit Information Bureau (India) LimitedDocument39 pagesCredit Information Bureau (India) LimitedmumbaiskingNo ratings yet

- Facets: Fintech Lending Trends From FACE Members, Mar 2022 Issue 1Document14 pagesFacets: Fintech Lending Trends From FACE Members, Mar 2022 Issue 1GUPTA SAGAR SURESH 1980174No ratings yet

- Bank Management: PGDM Iimc 2020 Praloy MajumderDocument35 pagesBank Management: PGDM Iimc 2020 Praloy MajumderLiontiniNo ratings yet

- Rural CreditDocument4 pagesRural CreditanjusaraliaNo ratings yet

- Project Finance: Campbell R. Harvey Aditya Agarwal Sandeep KaulDocument99 pagesProject Finance: Campbell R. Harvey Aditya Agarwal Sandeep KaulSudhir WaghuleNo ratings yet

- Low Income Housing Tax Credits: March 4, 2013Document31 pagesLow Income Housing Tax Credits: March 4, 2013Michael ShavolianNo ratings yet

- IFSL Confidential IM - Dec'22 17012023 PDFDocument22 pagesIFSL Confidential IM - Dec'22 17012023 PDFAhmed SamyNo ratings yet

- SME Finance in CambodiaDocument15 pagesSME Finance in CambodiaADBI EventsNo ratings yet

- N02912LICHSGFINXXXXX Dec17Document19 pagesN02912LICHSGFINXXXXX Dec17Ganesh KullarkarNo ratings yet

- IC Meeting 4a. - Private Credit RFP Wilshire PresentationDocument30 pagesIC Meeting 4a. - Private Credit RFP Wilshire Presentationgeorgi.korovskiNo ratings yet

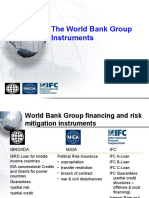

- The World Bank Group InstrumentsDocument14 pagesThe World Bank Group InstrumentsDinesh SolankiNo ratings yet

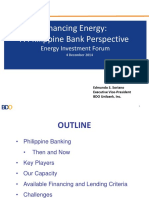

- Financing Energy: A Philippine Bank PerspectiveDocument40 pagesFinancing Energy: A Philippine Bank PerspectiveJoshua ArmeaNo ratings yet

- Why We Need Transparent Pricing in Microfinance: Chuck Waterfield Microfinance Transparency 11 November 2008Document63 pagesWhy We Need Transparent Pricing in Microfinance: Chuck Waterfield Microfinance Transparency 11 November 2008ziad saberiNo ratings yet

- Retail Banking in A Digital World: September 2015Document50 pagesRetail Banking in A Digital World: September 2015Abhi SharmaNo ratings yet

- Kumar Sachin Deo Kumar Sachin Deo Heena Praveen Heena PraveenDocument15 pagesKumar Sachin Deo Kumar Sachin Deo Heena Praveen Heena Praveenkumar sachin deoNo ratings yet

- Project ppt.-1Document21 pagesProject ppt.-1Shraddha TripathiNo ratings yet

- Sources of Working CapitalDocument17 pagesSources of Working CapitalAyush ShrimalNo ratings yet

- City Bank Limited, The: Update To Credit AnalysisDocument10 pagesCity Bank Limited, The: Update To Credit AnalysisJannatun NayeemaNo ratings yet

- CR NBFC Survey Mar2024 FinalDocument19 pagesCR NBFC Survey Mar2024 FinalmadhavkumarNo ratings yet

- Fne306 Assignment 6 AnsDocument9 pagesFne306 Assignment 6 AnsMichael PironeNo ratings yet

- Crif Creditscape Vol VII Personal Loans in IndiaDocument16 pagesCrif Creditscape Vol VII Personal Loans in IndiaHardik ShahNo ratings yet

- DCB Bank Growth and Financial PerformanceDocument8 pagesDCB Bank Growth and Financial PerformanceYogesh ChhaprooNo ratings yet

- Next Generation BankingDocument20 pagesNext Generation BankingyosephNo ratings yet

- MD Abdullah Al Mamun - ID-17102049 - Major Accounting.Document44 pagesMD Abdullah Al Mamun - ID-17102049 - Major Accounting.Abdullah Al MamunNo ratings yet

- HANOI UNIVERSITY REPORTDocument8 pagesHANOI UNIVERSITY REPORTQuynh Ngoc DangNo ratings yet

- Silicon Valley Bank Failure PDFDocument5 pagesSilicon Valley Bank Failure PDFKary MontalvoNo ratings yet

- Debt in Cameroon IMF and WBDocument14 pagesDebt in Cameroon IMF and WBprince marcNo ratings yet

- EdelweissDocument29 pagesEdelweissnprabakaran88No ratings yet

- Financial Management Case 9 Primus Automation DivisionDocument15 pagesFinancial Management Case 9 Primus Automation DivisiondidiNo ratings yet

- Credit Team Slides 1Document29 pagesCredit Team Slides 1Saugat DangalNo ratings yet

- Basel Norms and Credit Risk AssessmentDocument28 pagesBasel Norms and Credit Risk AssessmentAnubhav SrivastavaNo ratings yet

- Bajaj FinanceDocument19 pagesBajaj FinanceAmar50% (2)

- Fintech Emerging Don of Financial ServicesDocument23 pagesFintech Emerging Don of Financial Servicesavinash singhNo ratings yet

- Banking On Each Other PDFDocument43 pagesBanking On Each Other PDFYannis PierrakisNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2021 Volume III: Digitalizing Microfinance in Bangladesh: Findings from the Baseline SurveyFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2021 Volume III: Digitalizing Microfinance in Bangladesh: Findings from the Baseline SurveyNo ratings yet

- COBIT Control Objectives for Managing ITDocument35 pagesCOBIT Control Objectives for Managing IThendrigantingNo ratings yet

- THAIS MARIA SOUZA FREITAS InglesDocument2 pagesTHAIS MARIA SOUZA FREITAS InglesThais MariaNo ratings yet

- Flow Charting - TechniqueDocument3 pagesFlow Charting - TechniquemuneerppNo ratings yet

- PSA 330, 500 and 520: Chapter 3: Phase 2 - Risk Response: Overall and Further Audit ProdecuresDocument14 pagesPSA 330, 500 and 520: Chapter 3: Phase 2 - Risk Response: Overall and Further Audit ProdecuresLydelle Mae CabaltejaNo ratings yet

- HR-EssentialsDocument29 pagesHR-EssentialsReineNo ratings yet

- Kerr Uwi CV 2018 Update NDocument6 pagesKerr Uwi CV 2018 Update Napi-258725200No ratings yet

- HR Planning EssentialsDocument3 pagesHR Planning EssentialsAirish CruzNo ratings yet

- Transportation Engineering PDFDocument23 pagesTransportation Engineering PDFEashan Adil0% (2)

- Transactions Beginning in SapDocument7 pagesTransactions Beginning in SapalisnowkissNo ratings yet

- Prof. S K Palhan Operations Management: Post Graduate Diploma in Management Batch: 2013-2015Document3 pagesProf. S K Palhan Operations Management: Post Graduate Diploma in Management Batch: 2013-2015Shiva Kumar DunaboinaNo ratings yet

- While It Is True That Increases in Efficiency Generate Productivity IncreasesDocument3 pagesWhile It Is True That Increases in Efficiency Generate Productivity Increasesgod of thunder ThorNo ratings yet

- LA020504 Ass1 BSBMGT517 Ed2Document6 pagesLA020504 Ass1 BSBMGT517 Ed2ghasepNo ratings yet

- Customer Relationship Management AssignmentDocument8 pagesCustomer Relationship Management AssignmentPreeti ChoudharyNo ratings yet

- Case Study Regaining Service CustomersDocument16 pagesCase Study Regaining Service Customerspooja shutradharNo ratings yet

- Components of Data AnalyticsDocument4 pagesComponents of Data AnalyticsJoel DsouzaNo ratings yet

- Athletics ReviewDocument52 pagesAthletics ReviewMandy Hank RegoNo ratings yet

- Case study questions distribution and student assignmentsDocument2 pagesCase study questions distribution and student assignmentsTomi -No ratings yet

- Activity - Based - Costing Case SolutionDocument5 pagesActivity - Based - Costing Case SolutionRienk HeegsmaNo ratings yet

- MM 104 ReviewerDocument8 pagesMM 104 ReviewerKayeNo ratings yet

- Integrated Audit Manual 2015 LatestDocument73 pagesIntegrated Audit Manual 2015 LatestKunalKumarNo ratings yet

- Project Planning - As Applied in Engineering and Construction For Capital ProjectsDocument18 pagesProject Planning - As Applied in Engineering and Construction For Capital ProjectsReza SalimiNo ratings yet

- CH 18Document6 pagesCH 18أبو الحسن المطريNo ratings yet