You might also like

- Toast Profit Loss Statement Template 2022Document24 pagesToast Profit Loss Statement Template 2022Krishna SharmaNo ratings yet

- Calculations in The Catering Industry: 8065-02 Unit 219: Catering Operations, Costs and Menu PlanningDocument12 pagesCalculations in The Catering Industry: 8065-02 Unit 219: Catering Operations, Costs and Menu PlanningSZA100% (1)

- Presupuesto FamiliarbDocument10 pagesPresupuesto FamiliarbmmauryfgNo ratings yet

- Establishing Sales TargetDocument10 pagesEstablishing Sales TargetErich VirayNo ratings yet

- ADG Staffing Matrix As at 13-6-11 FINALDocument44 pagesADG Staffing Matrix As at 13-6-11 FINALAnanda ZoelfaNo ratings yet

- Cookery & Bakery: Ruwan Ranasinghe, BSC, MbaDocument61 pagesCookery & Bakery: Ruwan Ranasinghe, BSC, MbaCHATURIKA priyadarshaniNo ratings yet

- Excel 3 TestDocument3 pagesExcel 3 Testapi-233183465No ratings yet

- Employee Schedule1Document4 pagesEmployee Schedule1Faishal KalbuadiNo ratings yet

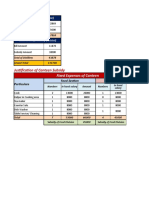

- Justification of Canteen SubsidyDocument2 pagesJustification of Canteen SubsidyGaurav Vij Asstt. Manager - H.RNo ratings yet

- Food Courts Food Malls Banquet Halls Set Up ConsultancyDocument28 pagesFood Courts Food Malls Banquet Halls Set Up ConsultancymohamadNo ratings yet

- Basic and Common Competencies ExamDocument2 pagesBasic and Common Competencies ExamNoreen Cañaveral NochefrancaNo ratings yet

- Restaurant Rating QuestionsDocument4 pagesRestaurant Rating QuestionsshehzadaminNo ratings yet

- Rev MNGTDocument63 pagesRev MNGTKiran MayiNo ratings yet

- Prof. V. B. Shah Institute of ManagementDocument69 pagesProf. V. B. Shah Institute of ManagementFaidz FuadNo ratings yet

- Food Storing and Issuing Control: Principles of Food, Beverage, and Labour Cost Controls, Canadian EditionDocument26 pagesFood Storing and Issuing Control: Principles of Food, Beverage, and Labour Cost Controls, Canadian Editionnur sharmira mohamdNo ratings yet

- Understanding Financial Statements and Financial RatiosDocument5 pagesUnderstanding Financial Statements and Financial RatiosJana Rose PaladaNo ratings yet

- Cookery 161121024647 PDFDocument150 pagesCookery 161121024647 PDFArlette Cargullo MolinaNo ratings yet

- Waste Managment NKA UPES Mar 2-2k11Document64 pagesWaste Managment NKA UPES Mar 2-2k11Nk AgarwalNo ratings yet

- Mapping of Cookery SkillsDocument2 pagesMapping of Cookery Skillszoltan2014No ratings yet

- PortfolioDocument49 pagesPortfolioapi-373140726No ratings yet

- FC & VCDocument25 pagesFC & VCAdanbungaran PangribNo ratings yet

- Soezzy'S Catering Planner V 3.06Document8 pagesSoezzy'S Catering Planner V 3.06José Manuel VazNo ratings yet

- Kitchen Equipment SelectionDocument21 pagesKitchen Equipment Selectioncucucucucu72No ratings yet

- Daily LogDocument1 pageDaily LogTarun MaudgalyaNo ratings yet

- F and B NC II Core - Unit 1Document28 pagesF and B NC II Core - Unit 1Jaybert GamayonNo ratings yet

- 6 7 Basic Kitchen Opening and Closing Checks TemplateDocument2 pages6 7 Basic Kitchen Opening and Closing Checks TemplatedonexcelNo ratings yet

- Meat and PoultryDocument34 pagesMeat and PoultryEben BudiantoNo ratings yet

- Sake Inventory and Cost - 16 Feb '15Document2 pagesSake Inventory and Cost - 16 Feb '15Tom TommyNo ratings yet

- Model Balance Sheet Word TemplateDocument2 pagesModel Balance Sheet Word TemplateHina JeeNo ratings yet

- Comply With Workplace Hygiene Procedures: Unit Code: D1.HRS - CL1.05 D1.HOT - CL1.04 D2.TTO - CL4.10Document187 pagesComply With Workplace Hygiene Procedures: Unit Code: D1.HRS - CL1.05 D1.HOT - CL1.04 D2.TTO - CL4.10irneil H. PepitoNo ratings yet

- SP Session1Document72 pagesSP Session1Abood Abood100% (1)

- Sequences of SpielsDocument5 pagesSequences of SpielsRoy AmoresNo ratings yet

- Service Standard Training PlanDocument9 pagesService Standard Training PlanQuy TranxuanNo ratings yet

- Hotel MuseFood Safety Monitoring Record Version 1Document13 pagesHotel MuseFood Safety Monitoring Record Version 1Aditya SharmaNo ratings yet

- Clean and Tidy Beverage and Food Service Areas HPR 3-12 SPDocument7 pagesClean and Tidy Beverage and Food Service Areas HPR 3-12 SPTiara Niken A100% (1)

- 337 Hotel Management & CateringDocument175 pages337 Hotel Management & CateringThusith WijayawardenaNo ratings yet

- Ch.5 - Inventory and COGS - MHDocument61 pagesCh.5 - Inventory and COGS - MHSamZhaoNo ratings yet

- Restaurant Cleaning Checklist: Week in Use: InitialsDocument3 pagesRestaurant Cleaning Checklist: Week in Use: InitialsSampalau AnglerNo ratings yet

- CostControls BarArtsDocument12 pagesCostControls BarArtsHuu Thanh TranNo ratings yet

- 15 Utensils and 5 Equipments: Anggota Kelompok: Yohana Riri Dian Hery BOYDocument21 pages15 Utensils and 5 Equipments: Anggota Kelompok: Yohana Riri Dian Hery BOYNadzwaaNo ratings yet

- Financial Analysis Cheat Sheet: by ViaDocument2 pagesFinancial Analysis Cheat Sheet: by Viaheehan6No ratings yet

- Hotel Management & Catering Technology SyllabusDocument81 pagesHotel Management & Catering Technology SyllabusYelesh LanjewarNo ratings yet

- Barmanagementpartone 220328155613Document257 pagesBarmanagementpartone 220328155613yudhiNo ratings yet

- Menu Pricing Menu PricingDocument44 pagesMenu Pricing Menu PricingEduardo GrandeNo ratings yet

- Restaurant ManualDocument38 pagesRestaurant Manualmaria ysareli jaimes rodriguezNo ratings yet

- Hospitality Hub Recipe Costing SheetDocument12 pagesHospitality Hub Recipe Costing SheetAntonio Salazar GutierrezNo ratings yet

- BHM 402T PDFDocument120 pagesBHM 402T PDFKamlesh HarbolaNo ratings yet

- Recipe Costing Form - Vegan Banana Bread - in Class Starting Point - Partially CompletedDocument1 pageRecipe Costing Form - Vegan Banana Bread - in Class Starting Point - Partially Completedapi-529979796No ratings yet

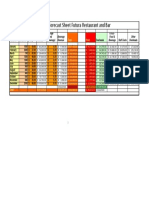

- Budget Forecast Sheet Futura Restaurant and BarDocument1 pageBudget Forecast Sheet Futura Restaurant and BarRaviNo ratings yet

- Ratio Analysis of The Balance Sheet: Accounting For Hospitality Managers Fifth Edition (362TXT or 362CIN)Document13 pagesRatio Analysis of The Balance Sheet: Accounting For Hospitality Managers Fifth Edition (362TXT or 362CIN)grishma jadavNo ratings yet

- M&M ThaneDocument808 pagesM&M ThanegadmaleNo ratings yet

- Food and Beverage ManagementDocument138 pagesFood and Beverage ManagementCaleb MukaviNo ratings yet

- Chapter 05 The Flow of Food An IntroductionDocument12 pagesChapter 05 The Flow of Food An Introductiondajonaef89No ratings yet

- BHM 232 Food and Beverage Operations 4Document6 pagesBHM 232 Food and Beverage Operations 4Pankaj PathaniaNo ratings yet

- Chapter 10 - Managing Food HygieneDocument38 pagesChapter 10 - Managing Food Hygienenaa znlNo ratings yet

- Forty Thieves of Food Cost An Updated Version v2Document4 pagesForty Thieves of Food Cost An Updated Version v2pogasNo ratings yet

- Free Training For Full Tools of F&B ManagementDocument48 pagesFree Training For Full Tools of F&B ManagementSPHM HospitalityNo ratings yet

- F&B Project - Tina TahilyaniDocument26 pagesF&B Project - Tina TahilyaniTina Tahilyani�No ratings yet

- HT2 CoCU 2 Cooking TechniqueDocument10 pagesHT2 CoCU 2 Cooking TechniqueNama Saya Suhail HadriNo ratings yet

- Balance Sheet Component Matching Solution: Account DescriptionDocument3 pagesBalance Sheet Component Matching Solution: Account Descriptionnishant jindalNo ratings yet

- Ent600 - Blueprint - Guidelines & TemplateDocument16 pagesEnt600 - Blueprint - Guidelines & TemplateSOFIA EIZZATUL EILLYANA ZAMBAHARINo ratings yet

- SM Garrison MGR Acc 13e Ch16Document49 pagesSM Garrison MGR Acc 13e Ch16YuliArdiansyahNo ratings yet

- Business Plan: Mobile RestaurantDocument29 pagesBusiness Plan: Mobile RestaurantVytautas VasiliauskasNo ratings yet

- 1049 IndAS Notes by CA Chiranjeev Jain PDFDocument28 pages1049 IndAS Notes by CA Chiranjeev Jain PDFMaya ChaudharyNo ratings yet

- Financial Accounting: Accounting For Merchandise OperationsDocument84 pagesFinancial Accounting: Accounting For Merchandise OperationsAnnie DuolingoNo ratings yet

- Monopoly Profit MaximizationDocument29 pagesMonopoly Profit MaximizationArmanNo ratings yet

- Pre-Test Entreprenuership Grade-12 Choose The Best AnswerDocument5 pagesPre-Test Entreprenuership Grade-12 Choose The Best AnswerMark Gil GuillermoNo ratings yet

- Eportfolio AssignmentDocument12 pagesEportfolio Assignmentapi-300872702No ratings yet

- WatatapsDocument29 pagesWatatapsjessa mae zerdaNo ratings yet

- Implementing Strategies: Marketing, Finance/Accounting, R&D, & MIS IssuesDocument18 pagesImplementing Strategies: Marketing, Finance/Accounting, R&D, & MIS IssuesIcuwootNo ratings yet

- Mid Term Exam FIN 3-Aug 2013Document20 pagesMid Term Exam FIN 3-Aug 2013monzkymine57% (7)

- Chapter 14Document38 pagesChapter 14Carmelie CumigadNo ratings yet

- Specific Financial Reporting Questions & Answers: Suggested Solution 1Document37 pagesSpecific Financial Reporting Questions & Answers: Suggested Solution 1Tawanda Tatenda Herbert100% (2)

- 21 Financial Assets at Fair Value: Solution 21-1 Answer CDocument30 pages21 Financial Assets at Fair Value: Solution 21-1 Answer CLayNo ratings yet

- 6.income Statement and Related InformationDocument45 pages6.income Statement and Related InformationShajidur RashidNo ratings yet

- Item 1days Expenses (RM) Other Expenses (RM) : Administrative BudgetDocument4 pagesItem 1days Expenses (RM) Other Expenses (RM) : Administrative Budgetmohd_mddNo ratings yet

- Latihan Jurnal PenyesuaianDocument5 pagesLatihan Jurnal Penyesuaiangabriel berwulo100% (1)

- Entrepreneurship ManagementDocument18 pagesEntrepreneurship Managementcandy lollipoNo ratings yet

- Most Common Finance Interview QuestionsDocument20 pagesMost Common Finance Interview QuestionsAyushiNo ratings yet

- CHAPTER 2 Review of Financial Statement Preparation, Analysis, and InterpretationDocument6 pagesCHAPTER 2 Review of Financial Statement Preparation, Analysis, and InterpretationCatherine Rivera100% (3)

- Fabm 121.week 6-10 ModuleDocument22 pagesFabm 121.week 6-10 Modulekhaizer matias100% (1)

- Chapter 08, Modern Advanced Accounting-Review Q & ExrDocument36 pagesChapter 08, Modern Advanced Accounting-Review Q & Exrrlg4814100% (5)

- Project On HondaDocument68 pagesProject On HondaPraveen Kumar Hc50% (2)

- Feasibility StudyDocument46 pagesFeasibility StudyAcsecnarf AbarueNo ratings yet

- Cash Flow Excercise Questions-Set-2Document2 pagesCash Flow Excercise Questions-Set-2AgANo ratings yet

- Financial Planning and ControlDocument10 pagesFinancial Planning and ControlMoona AwanNo ratings yet

- Employees Benefit PalnDocument60 pagesEmployees Benefit PalnHimanshu GaurNo ratings yet

- Khurasan University Faculty of Economics (BBA) : Cost AccountingDocument47 pagesKhurasan University Faculty of Economics (BBA) : Cost AccountingTalaqa Sam Sha100% (2)

- Boston Beer Company Case ExhibitsDocument2 pagesBoston Beer Company Case ExhibitsDavidNo ratings yet

- Worksheet Data For Savaglia Company Are Presented Below. The Owner Did Not Make Any Additional Investments in The Business in April.Document6 pagesWorksheet Data For Savaglia Company Are Presented Below. The Owner Did Not Make Any Additional Investments in The Business in April.Risky FernandoNo ratings yet