You might also like

- This Study Resource Was: Tutorial 6Document4 pagesThis Study Resource Was: Tutorial 6Nicole CapundanNo ratings yet

- Chartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalDocument81 pagesChartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalPrashant Sagar GautamNo ratings yet

- RTP Dec 2020 QnsDocument13 pagesRTP Dec 2020 QnsbinuNo ratings yet

- Financial Accounting II MinDocument4 pagesFinancial Accounting II MinAsna Rachal ShibuNo ratings yet

- Tutorial 11 Preparation of Financial Statements (Q)Document6 pagesTutorial 11 Preparation of Financial Statements (Q)lious liiNo ratings yet

- Project Question: Financial Management 1ADocument4 pagesProject Question: Financial Management 1AHashimRazaNo ratings yet

- FINANCIAL ACCOUNTING I 2019 MinDocument6 pagesFINANCIAL ACCOUNTING I 2019 MinKedarNo ratings yet

- Institute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartDocument3 pagesInstitute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartSafi SheikhNo ratings yet

- FAC511S - Financial Accounting 101 - 2nd Opportunity - January 2017Document6 pagesFAC511S - Financial Accounting 101 - 2nd Opportunity - January 2017Uno VeiiNo ratings yet

- Minicases 5Document3 pagesMinicases 5dini sofiaNo ratings yet

- Acct 1 and 2 ProblemsDocument3 pagesAcct 1 and 2 ProblemsRenz AlconeraNo ratings yet

- AC1025 2016 Exam Paper With Comments AC1025 2016 Exam Paper With CommentsDocument74 pagesAC1025 2016 Exam Paper With Comments AC1025 2016 Exam Paper With Comments전민건No ratings yet

- FYJC Book Keeping and Accuntancy Topic Final AccountDocument4 pagesFYJC Book Keeping and Accuntancy Topic Final AccountRavichandraNo ratings yet

- II PUC Accountancy Paper 2Document6 pagesII PUC Accountancy Paper 2Tarannum KNo ratings yet

- Ncpar Cup 2012Document18 pagesNcpar Cup 2012Allen Carambas Astro100% (2)

- MBAP - AF101-Accounting and Finance - 10 Nov 23Document6 pagesMBAP - AF101-Accounting and Finance - 10 Nov 23aqueelahadam786No ratings yet

- Mock Exercise 16 July 2021 Dear Students, Submit It Using Dummy Link Provided On WBLEDocument3 pagesMock Exercise 16 July 2021 Dear Students, Submit It Using Dummy Link Provided On WBLEWen Xin GanNo ratings yet

- Budgeting and Cash Flow ForecastingDocument3 pagesBudgeting and Cash Flow ForecastingJing ZeNo ratings yet

- Bcom 2 Sem Financial Accounting 2 20101139 Nov 2020Document5 pagesBcom 2 Sem Financial Accounting 2 20101139 Nov 2020Akhil AbrahamNo ratings yet

- Sec 03 - A2Document8 pagesSec 03 - A2MahmozNo ratings yet

- Bookkeeping: June 2019Document5 pagesBookkeeping: June 2019Kay100% (1)

- Review Questions Volume 1 - Chapter 28Document2 pagesReview Questions Volume 1 - Chapter 28YelenochkaNo ratings yet

- Accounting Paper-Zoom 2Document7 pagesAccounting Paper-Zoom 2Sufyan SheikhNo ratings yet

- Higher National Diploma in Accountancy Hnda 2 Year, Second Semester Examination - 2018 2202-Computer Applications For AccountingDocument14 pagesHigher National Diploma in Accountancy Hnda 2 Year, Second Semester Examination - 2018 2202-Computer Applications For AccountingName of RoshanNo ratings yet

- BCOMSC - Accounting 1 - 15-Jan-24 - S1Document8 pagesBCOMSC - Accounting 1 - 15-Jan-24 - S1blessingmudarikwa2No ratings yet

- AccountingDocument19 pagesAccountinggigigiNo ratings yet

- FA Dec 2018Document8 pagesFA Dec 2018Shawn LiewNo ratings yet

- Accounting Grade 12 Test 1Document4 pagesAccounting Grade 12 Test 1Ryno de BeerNo ratings yet

- Akuntansi KeuanganDocument11 pagesAkuntansi KeuanganDyan NoviaNo ratings yet

- FAC1502 Assignment 4 Semester 2 2023Document192 pagesFAC1502 Assignment 4 Semester 2 2023Haat My LaterNo ratings yet

- Accounting NumaricalDocument7 pagesAccounting NumaricalMuhamamd Asfand YarNo ratings yet

- UKAF1083 FA2 - Sept 2017 Adapted A.Q1 B.Q1a B.Q2aDocument7 pagesUKAF1083 FA2 - Sept 2017 Adapted A.Q1 B.Q1a B.Q2a--bolabolaNo ratings yet

- Question - Test Acc106 Mac 2021 - 2july2021Document4 pagesQuestion - Test Acc106 Mac 2021 - 2july2021Fara husnaNo ratings yet

- Analysis of Financial Statement-I - FIN330 (A)Document2 pagesAnalysis of Financial Statement-I - FIN330 (A)Aisha AishaNo ratings yet

- FND Partnership QuestionDocument3 pagesFND Partnership QuestionShweta BhadauriaNo ratings yet

- AFA End Examination 2021-2022Document6 pagesAFA End Examination 2021-2022sebastian mlingwaNo ratings yet

- 73601bos59426 Inter p5qDocument7 pages73601bos59426 Inter p5qKali KhannaNo ratings yet

- Loyola College (Autonomous), Chennai - 600 034: Degree Examination - CommerceDocument4 pagesLoyola College (Autonomous), Chennai - 600 034: Degree Examination - CommerceHarish KapoorNo ratings yet

- Abfa1513 220518Document6 pagesAbfa1513 220518CRYSTAL NGNo ratings yet

- Faculty of Management Sciences: Department: Accounting Economics and FinanceDocument5 pagesFaculty of Management Sciences: Department: Accounting Economics and FinanceUno VeiiNo ratings yet

- Student financial accounts portfolioDocument5 pagesStudent financial accounts portfolioKevin PhạmNo ratings yet

- AccountingDocument5 pagesAccountingOwen Hambulo Sr.No ratings yet

- Tutorial 3Document14 pagesTutorial 3NURSUHAILI IZZATI ABU BAKARNo ratings yet

- Exam MaeDocument3 pagesExam MaeIbtissam El mansouriNo ratings yet

- 11 Com Pre-ExamDocument4 pages11 Com Pre-ExamObaid Khan50% (2)

- HAC Intro To FInancial Management QuestionPaperDocument6 pagesHAC Intro To FInancial Management QuestionPaperfortune maviyaNo ratings yet

- April 2020 Exam for Introduction to Accounting at UTARDocument5 pagesApril 2020 Exam for Introduction to Accounting at UTARCRYSTAL NGNo ratings yet

- ExercisesDocument20 pagesExercisesRolivhuwaNo ratings yet

- CA Inter Adv. Accounting Top 50 Question May 2021Document117 pagesCA Inter Adv. Accounting Top 50 Question May 2021Sumitra yadavNo ratings yet

- Financial Accounting P3Document4 pagesFinancial Accounting P3amiNo ratings yet

- Test Series: October, 2020 Mock Test Paper Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingDocument7 pagesTest Series: October, 2020 Mock Test Paper Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingAruna RajappaNo ratings yet

- Primehyper Tax Calculation for 2023Document4 pagesPrimehyper Tax Calculation for 2023Asive BalisoNo ratings yet

- Accounts Receivable ReviewDocument15 pagesAccounts Receivable ReviewnanaNo ratings yet

- Bafna Suggested Answers CDocument18 pagesBafna Suggested Answers Csizantu100% (1)

- FAC1601 Financial Accounting Reporting Tutorial LetterDocument15 pagesFAC1601 Financial Accounting Reporting Tutorial LetterSophie ZinyandoNo ratings yet

- Practice Paper-June 2020: Answer Any Five Sub-Questions, Each Sub-Question Carries Two Marks. 5x2 10Document5 pagesPractice Paper-June 2020: Answer Any Five Sub-Questions, Each Sub-Question Carries Two Marks. 5x2 10RavichandraNo ratings yet

- Corporate Accounting Ii-1Document4 pagesCorporate Accounting Ii-1ARAVIND V KNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Microeconomics Marking Key SET 1Document7 pagesMicroeconomics Marking Key SET 1Yus LindaNo ratings yet

- Microeconmics QP Set 1Document10 pagesMicroeconmics QP Set 1Yus LindaNo ratings yet

- DIM2183 Exam Jan 2024 Set 1Document4 pagesDIM2183 Exam Jan 2024 Set 1Yus LindaNo ratings yet

- Chapter 7 and 8 Market StructureDocument16 pagesChapter 7 and 8 Market StructureYus LindaNo ratings yet

- Chapter 6 Cost of ProductionDocument9 pagesChapter 6 Cost of ProductionYus LindaNo ratings yet

- DIM1363 MK Set 1Document4 pagesDIM1363 MK Set 1Yus LindaNo ratings yet

- Chapter 2 Demand SupplyDocument9 pagesChapter 2 Demand SupplyYus LindaNo ratings yet

- Chapter 4 Theory of Consumer BehaviourDocument9 pagesChapter 4 Theory of Consumer BehaviourYus Linda100% (1)

- Microeconomics: Chapter 3 Market Equilibrium: DD SSDocument9 pagesMicroeconomics: Chapter 3 Market Equilibrium: DD SSYus LindaNo ratings yet

- Chapter 5 Theory of ProductionDocument5 pagesChapter 5 Theory of ProductionYus Linda100% (1)

- Sirah Tahun 1Document7 pagesSirah Tahun 1Ibrahim Fikri Bin Abdullah84% (49)

- Chapter 1 IntroductionDocument7 pagesChapter 1 IntroductionYus LindaNo ratings yet

- Tutorial 8Document3 pagesTutorial 8Yus LindaNo ratings yet

- Tutorial 6Document2 pagesTutorial 6Yus LindaNo ratings yet

- Promotion Tutorial Sales TechniquesDocument2 pagesPromotion Tutorial Sales TechniquesYus LindaNo ratings yet

- Corporate FinanceDocument5 pagesCorporate FinanceYus LindaNo ratings yet

- Tutorial 5: Chapter 5Document3 pagesTutorial 5: Chapter 5Yus LindaNo ratings yet

- Name: Tutorial Chapter 3Document3 pagesName: Tutorial Chapter 3Yus LindaNo ratings yet

- Chapter 4 Theory of Consumer BehaviourDocument9 pagesChapter 4 Theory of Consumer BehaviourYus LindaNo ratings yet

- Quiz: Chapter 4Document2 pagesQuiz: Chapter 4Yus LindaNo ratings yet

- Tutorial 7Document3 pagesTutorial 7Yus LindaNo ratings yet

- Marketing Concept QuizDocument3 pagesMarketing Concept QuizYus LindaNo ratings yet

- Quiz: Chapter 2Document2 pagesQuiz: Chapter 2Yus LindaNo ratings yet

- General Konwledge QuizDocument53 pagesGeneral Konwledge QuizYus LindaNo ratings yet

- Important !: We Can Only AddDocument7 pagesImportant !: We Can Only AddYus LindaNo ratings yet

- Kassean & Juwaheer 26Document15 pagesKassean & Juwaheer 26Noush BakerallyNo ratings yet

- Category Company Locality Address Pin Email Whatsappphone #1 Phone #2 Phone #3Document35 pagesCategory Company Locality Address Pin Email Whatsappphone #1 Phone #2 Phone #3Sunny KulshresthaNo ratings yet

- H9Jlfv2H: M-Pesa StatementDocument1 pageH9Jlfv2H: M-Pesa StatementTHE EMPIRE LIONS ROBOTICS INVESTMENTS LTDNo ratings yet

- Summary of Account Activity Payment Information: Protecting What Matters MostDocument4 pagesSummary of Account Activity Payment Information: Protecting What Matters MostJames BergmanNo ratings yet

- Transport ListDocument9 pagesTransport ListJavahir sarojNo ratings yet

- Novatek Layer Mash - Rfq-Kcsa-9492 PDFDocument1 pageNovatek Layer Mash - Rfq-Kcsa-9492 PDFKennedy MsimukoNo ratings yet

- How Do We Deliver Truck Trailer To You by Sea (Shipping Procedure)Document16 pagesHow Do We Deliver Truck Trailer To You by Sea (Shipping Procedure)DTG GroupNo ratings yet

- Guidance Installation SDA AntennaDocument22 pagesGuidance Installation SDA AntennaYorico Bhaskara ManoppoNo ratings yet

- Income Tax Payment Mandate Form RTGS NEFTDocument2 pagesIncome Tax Payment Mandate Form RTGS NEFTNitin RautNo ratings yet

- C - Report 18 PDFDocument32 pagesC - Report 18 PDF30 Novita Kusuma WardhaniNo ratings yet

- The Nigerian Financial System at A Glance - Monetary Policy DepartmentDocument356 pagesThe Nigerian Financial System at A Glance - Monetary Policy DepartmentAgbons EbohonNo ratings yet

- Faktor yang Mempengaruhi Keputusan Pembelian Melalui Sosial MediaDocument8 pagesFaktor yang Mempengaruhi Keputusan Pembelian Melalui Sosial MediaArum Mukti UtamiNo ratings yet

- Supply Chain For Dummies JDADocument76 pagesSupply Chain For Dummies JDAAgustin Scoponi100% (5)

- Capstone Project: Submitted in The Partial Fulfillment For The Award of The Degree ofDocument115 pagesCapstone Project: Submitted in The Partial Fulfillment For The Award of The Degree ofRushikesh ChandeleNo ratings yet

- Introduction To Data CommunicationDocument72 pagesIntroduction To Data CommunicationRaj ChauhanNo ratings yet

- VTUlive Banking Question BankDocument2 pagesVTUlive Banking Question BankNaren Samy100% (1)

- 1.bcredit Creation by CLDocument4 pages1.bcredit Creation by CLBoobalan RNo ratings yet

- 1A What Is Managed Care Pharmacy - 2016Document31 pages1A What Is Managed Care Pharmacy - 2016Nhuong LeNo ratings yet

- Purchases Day BookDocument8 pagesPurchases Day Bookdrishti.singh0609No ratings yet

- (Decision Lab) - Epayments U&A Report1Document47 pages(Decision Lab) - Epayments U&A Report1Leo LuuNo ratings yet

- Cloudup - Cloud Practitioner ScheduleDocument2 pagesCloudup - Cloud Practitioner ScheduleMonika MoniNo ratings yet

- Updated - SBB Script (BL DLP) - ZenithDocument18 pagesUpdated - SBB Script (BL DLP) - Zenithuday kumarNo ratings yet

- CyberEdge Insurance Proposal Form SummaryDocument6 pagesCyberEdge Insurance Proposal Form SummaryMW MelvinNo ratings yet

- Banking and Finance Project-1Document37 pagesBanking and Finance Project-1ADITYA DHONENo ratings yet

- World tourism vocabulary and statisticsDocument4 pagesWorld tourism vocabulary and statisticsSeradona Altiria AlexonNo ratings yet

- Webplat Technologies PVT LTDDocument17 pagesWebplat Technologies PVT LTDmayur KhadseNo ratings yet

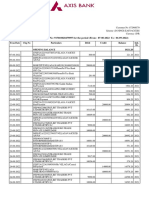

- Account STMTDocument5 pagesAccount STMTvamsiNo ratings yet

- 5pmf1710235pmf12e08023779d774074 Fpesig1710235puy7sw8t7nrbtwaDocument10 pages5pmf1710235pmf12e08023779d774074 Fpesig1710235puy7sw8t7nrbtwaAyush PanditaNo ratings yet

- Madocs HXDocument3 pagesMadocs HXJoren Angela GalangNo ratings yet

- E-commerce Growth in Peru During COVID-19Document82 pagesE-commerce Growth in Peru During COVID-19David HRNo ratings yet