You might also like

- List of Cases of Supreme Court, 2010Document31 pagesList of Cases of Supreme Court, 2010Nagaraja ReddyNo ratings yet

- Company Production Installed Capacity Net Profit (2008-2009) (Rs Lakhs)Document7 pagesCompany Production Installed Capacity Net Profit (2008-2009) (Rs Lakhs)Ponnoju ShashankaNo ratings yet

- (Copy of The Same Is Also Available On Our Website) : IndicationDocument4 pages(Copy of The Same Is Also Available On Our Website) : IndicationajgondalNo ratings yet

- JSW Steel - WikipediaDocument28 pagesJSW Steel - WikipediaPawan SrivastavaNo ratings yet

- Case 5 Tata Steel's Acquisition of CorusDocument28 pagesCase 5 Tata Steel's Acquisition of Corusashmit100% (1)

- Top Tata Buyouts ReportDocument1 pageTop Tata Buyouts ReportSanket PaiNo ratings yet

- Adarsh Management Institute of India: An Iso 9001: 2008 Certified International B-SchoolDocument17 pagesAdarsh Management Institute of India: An Iso 9001: 2008 Certified International B-SchoolAmit TandelNo ratings yet

- Indian Insider Buyings June 17, 2008-DhananDocument2 pagesIndian Insider Buyings June 17, 2008-Dhananapi-3702531No ratings yet

- Tata Steel EuropeDocument5 pagesTata Steel Europeraj_mduNo ratings yet

- Collaboration and FinanceDocument11 pagesCollaboration and FinanceAditya JainNo ratings yet

- PrefaceDocument4 pagesPrefacevikas04071987No ratings yet

- Bibliography: Business WorldDocument19 pagesBibliography: Business WorldKajal KumariNo ratings yet

- 2012 Sept IMG NoteDocument12 pages2012 Sept IMG NoteNDTVNo ratings yet

- Market Outlook Market Outlook: Dealer's DiaryDocument13 pagesMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingNo ratings yet

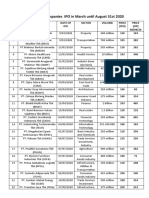

- Indonesian Companies IPO in March Until August 31st 2020Document2 pagesIndonesian Companies IPO in March Until August 31st 2020Landrikus RevynNo ratings yet

- A Presentation of Economics Analysis ON Tata Steel LTDDocument35 pagesA Presentation of Economics Analysis ON Tata Steel LTDDhaval PatelNo ratings yet

- Tata Steel - Corus Case StudyDocument24 pagesTata Steel - Corus Case StudyMegha Munshi ShahNo ratings yet

- Sterlite Industries From Wikipedia, The Free EncyclopediaDocument7 pagesSterlite Industries From Wikipedia, The Free EncyclopediamanirathinaNo ratings yet

- Tata Steel Limited Is An Indian Multinational SteelDocument5 pagesTata Steel Limited Is An Indian Multinational SteelDeepak NayakNo ratings yet

- 9 October 2015Document1 page9 October 2015Ady HasbullahNo ratings yet

- Vol 25, Issue No 9, DataBankDocument32 pagesVol 25, Issue No 9, DataBanklkmsrkNo ratings yet

- Mergers&Acquisition Report On Tata Steel and CorusDocument10 pagesMergers&Acquisition Report On Tata Steel and Corusdipanjan dharNo ratings yet

- POSCO India - Company ProfileDocument4 pagesPOSCO India - Company Profilevinit1117No ratings yet

- Corporate PresentationDocument39 pagesCorporate PresentationSheshank VermaNo ratings yet

- Indian Coal Allocation Scam: Jump To Navigationjump To SearchDocument12 pagesIndian Coal Allocation Scam: Jump To Navigationjump To SearchAbhishek KumarNo ratings yet

- Tata Steel LimitedDocument11 pagesTata Steel LimitedSTAR PRINTINGNo ratings yet

- Indian Steel Industry: An OverviewDocument7 pagesIndian Steel Industry: An OverviewAshwin KelwadkarNo ratings yet

- VN Hi HVVFDocument4 pagesVN Hi HVVFSurys AccountNo ratings yet

- Infrastructural Challenges in Steel Industry - Best Paper Published in 4th International Steel Logistics Conference in AntwerpDocument38 pagesInfrastructural Challenges in Steel Industry - Best Paper Published in 4th International Steel Logistics Conference in Antwerpsubrat_sahoo19690% (1)

- Sterlite Copper - WikipediaDocument14 pagesSterlite Copper - Wikipediasupriya sonkusareNo ratings yet

- Tata Steel LTD Corus Steel See ReportDocument25 pagesTata Steel LTD Corus Steel See ReportRavi ganganiNo ratings yet

- Strategy Management Project Report On Tata SteelDocument34 pagesStrategy Management Project Report On Tata SteelAndreea CriclevitNo ratings yet

- Tata SteelDocument41 pagesTata SteelSanjana GuptaNo ratings yet

- Porter's Analysis On IndustryDocument11 pagesPorter's Analysis On IndustrySnow SnowNo ratings yet

- M&A Tata Corus Merger AnalysisDocument21 pagesM&A Tata Corus Merger AnalysisPreetam Joga100% (1)

- Time Schedule As-10 WebsiteDocument12 pagesTime Schedule As-10 WebsiteParth DewanganNo ratings yet

- Ann Rep 1011Document118 pagesAnn Rep 1011Rachit TiwariNo ratings yet

- IDT Tested Case LawsDocument2 pagesIDT Tested Case Lawssathish_61288@yahooNo ratings yet

- Issuer Company Issue Open Issue Close Offer Price (RS.) Issue Type Issue Size (Crore RS.)Document2 pagesIssuer Company Issue Open Issue Close Offer Price (RS.) Issue Type Issue Size (Crore RS.)Bishal HandiqueNo ratings yet

- Kalyani Steel LimitedDocument26 pagesKalyani Steel LimitedDeepak L JainNo ratings yet

- JSW Steel LTDDocument5 pagesJSW Steel LTDCA Sonia JageshaNo ratings yet

- Tata Steel Corus Acquisition Financial DetailsDocument6 pagesTata Steel Corus Acquisition Financial DetailsSandarbh Agarwal0% (1)

- Tata Steel LimitedDocument19 pagesTata Steel LimitedARINDAM DATTANo ratings yet

- Tata Corus AcquisitionDocument10 pagesTata Corus Acquisitionsheetal_jerathNo ratings yet

- Overview of Indian Cement Industry 2010Document17 pagesOverview of Indian Cement Industry 2010shubhav1988100% (2)

- Agreement Between NSSMC and Arcelormittal Regarding Joint Acquisition of Essar Steel India Limited and Establishment of A Joint Venture in IndiaDocument2 pagesAgreement Between NSSMC and Arcelormittal Regarding Joint Acquisition of Essar Steel India Limited and Establishment of A Joint Venture in IndiaGanesan RamanNo ratings yet

- Fortnightly Portfolio - Axis Ultra Short Term Fund - 30 SeptemberDocument6 pagesFortnightly Portfolio - Axis Ultra Short Term Fund - 30 SeptemberKoustav MondalNo ratings yet

- Tata SteelDocument28 pagesTata SteelSonica LodhaNo ratings yet

- 49189151Document10 pages49189151Chirag FulwaniNo ratings yet

- TISCODocument4 pagesTISCODev BansalNo ratings yet

- QuizDocument10 pagesQuizravipearlNo ratings yet

- Vol 25, Issue No 23, DataBankDocument32 pagesVol 25, Issue No 23, DataBankAshish RanjanNo ratings yet

- Tata Corus Acquisition and M&ADocument16 pagesTata Corus Acquisition and M&ASaurabh PaliwalNo ratings yet

- Brief Overview of Steel Authority of India Ltd. (SAIL) : (A) Merger & Acquisition (M&A)Document7 pagesBrief Overview of Steel Authority of India Ltd. (SAIL) : (A) Merger & Acquisition (M&A)Himansu Sekhar KisanNo ratings yet

- Sail Project ReportDocument4 pagesSail Project ReportSumeshNo ratings yet

- CL Test Unit 3Document4 pagesCL Test Unit 3VbNo ratings yet

- Summary of Classification of LiabilitiesDocument14 pagesSummary of Classification of LiabilitiesJulma JaiiyNo ratings yet

- Investment Banking - : Introduction, History, and Their Business Portfolio (Chapter 5 & 6)Document16 pagesInvestment Banking - : Introduction, History, and Their Business Portfolio (Chapter 5 & 6)SuvajitLaikNo ratings yet

- Different Types of Capital IssuesDocument5 pagesDifferent Types of Capital IssuesUdhayakumar ManickamNo ratings yet

- TYIT InternshipDocument1 pageTYIT Internshipsubhamgupta7495No ratings yet

- How To Draft Articles of IncorporationDocument7 pagesHow To Draft Articles of Incorporationgilbertmalcolm100% (1)

- CH 14Document61 pagesCH 14arif nugraha100% (1)

- BASFINE - Banks HomeworkDocument5 pagesBASFINE - Banks HomeworkDanaNo ratings yet

- Mutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPDocument32 pagesMutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPbholagangster1No ratings yet

- BLL12 - Introduction To NI ActDocument3 pagesBLL12 - Introduction To NI Actsvm kishoreNo ratings yet

- Chapter 8 HomeworkDocument4 pagesChapter 8 HomeworkJones RamosNo ratings yet

- Ratio Analysis - Montex PensDocument28 pagesRatio Analysis - Montex Penss_sannit2k9No ratings yet

- The Capital Asset Pricing Model (CAPM)Document17 pagesThe Capital Asset Pricing Model (CAPM)RezvanmoghisehNo ratings yet

- REVENUE MEMORANDUM ORDER NO. 3-2009 Issued On January 23, 2009 Amends andDocument7 pagesREVENUE MEMORANDUM ORDER NO. 3-2009 Issued On January 23, 2009 Amends andGedan TanNo ratings yet

- Direct Tax AssignmentDocument3 pagesDirect Tax AssignmentCHAITANYA ANNE100% (1)

- RSM 332 Lec1Document16 pagesRSM 332 Lec1Bella ChungNo ratings yet

- Ch01-The Investment SettingDocument27 pagesCh01-The Investment Settingmc limNo ratings yet

- Asset Privatization Trust Vs SandiganbayanDocument13 pagesAsset Privatization Trust Vs Sandiganbayandarts090No ratings yet

- OverviewDocument9 pagesOverviewwwongvgNo ratings yet

- Mergers and AcquisitionDocument93 pagesMergers and Acquisitionapi-3712392100% (7)

- Company Project 1Document23 pagesCompany Project 1Amber SiddiquiNo ratings yet

- Understanding A Private Placement (Texas)Document28 pagesUnderstanding A Private Placement (Texas)bdelphinNo ratings yet

- Initial Syngenta Response - 4!30!2015Document2 pagesInitial Syngenta Response - 4!30!2015Marla BarbotNo ratings yet

- Value Based MGTDocument75 pagesValue Based MGTNoorunnishaNo ratings yet

- Uas AKMDocument14 pagesUas AKMThorieq Mulya MiladyNo ratings yet

- Arbitage TheoryDocument9 pagesArbitage Theorymahesh19689No ratings yet

- MastekDocument27 pagesMastekcsheth3650No ratings yet

- List of Blockchain Use CasesDocument8 pagesList of Blockchain Use CasesSelvakumar EsraNo ratings yet

- Investment and Security Analysis by Charles P Jones 12th Ed Chapter 1 - Tabish Khan From KohatDocument25 pagesInvestment and Security Analysis by Charles P Jones 12th Ed Chapter 1 - Tabish Khan From KohatTabish KhanNo ratings yet

- DD 190220143644Document1 pageDD 190220143644gyrics7No ratings yet

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyFrom EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyRating: 3 out of 5 stars3/5 (1)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsFrom EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNo ratings yet

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsFrom EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsRating: 4.5 out of 5 stars4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondFrom EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNo ratings yet

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)From EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Rating: 4 out of 5 stars4/5 (5)

- Buffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsFrom EverandBuffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsRating: 5 out of 5 stars5/5 (1)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)