You might also like

- Qatar - Civil Material RatesDocument20 pagesQatar - Civil Material Ratespraveenraj murugadass100% (1)

- Solution Manual for an Introduction to Equilibrium ThermodynamicsFrom EverandSolution Manual for an Introduction to Equilibrium ThermodynamicsNo ratings yet

- PDF To DocsDocument72 pagesPDF To Docs777priyankaNo ratings yet

- MasDocument13 pagesMasHiroshi Wakato50% (2)

- Unit 2-3 ADM TYBBADocument24 pagesUnit 2-3 ADM TYBBAVohra AimanNo ratings yet

- AkmenDocument2 pagesAkmenHuệ ĐặngNo ratings yet

- Silo - Tips Standard Costing With SolutionsDocument65 pagesSilo - Tips Standard Costing With SolutionsAlbert MuzitiNo ratings yet

- Cost Accountin1ccm 116Document3 pagesCost Accountin1ccm 116gakumoNo ratings yet

- Practice Question Three-Material, Labour Sales Mix VarianceDocument4 pagesPractice Question Three-Material, Labour Sales Mix VarianceGrechen UdigengNo ratings yet

- Standard Costing 2Document69 pagesStandard Costing 2Jash SanghviNo ratings yet

- Worksheet Campar IndustriesDocument11 pagesWorksheet Campar IndustriesRUPIKA R GNo ratings yet

- Standard Costing With Solutions: SolutionDocument3 pagesStandard Costing With Solutions: Solution777priyankaNo ratings yet

- 8 Standard CostingDocument10 pages8 Standard CostingLakshay SharmaNo ratings yet

- (Chap 25) MaDocument11 pages(Chap 25) MaDuong TrinhNo ratings yet

- Input STD Material 1000Kg Output STD Finish Good 990 KG Wastage 10kgDocument2 pagesInput STD Material 1000Kg Output STD Finish Good 990 KG Wastage 10kglucifer goneNo ratings yet

- Variance Analysis CW QuestionsDocument14 pagesVariance Analysis CW QuestionsMedhaNo ratings yet

- Chp1 QuestionsOnStandardCostingDocument9 pagesChp1 QuestionsOnStandardCostingNur HidayahNo ratings yet

- Fact Pattern: Example 10.5 (Direct Material Cost Variances)Document9 pagesFact Pattern: Example 10.5 (Direct Material Cost Variances)Saiyed KosinNo ratings yet

- Chapter 12 Standard Costing Nov 2020 2Document112 pagesChapter 12 Standard Costing Nov 2020 2Kunal KuvadiaNo ratings yet

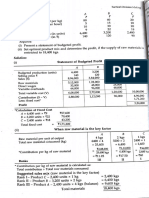

- Budgeted Statement ExamDocument11 pagesBudgeted Statement ExamNelz KhoNo ratings yet

- Exercises 2-Standard CostingDocument4 pagesExercises 2-Standard CostingBernardo BuenaventeNo ratings yet

- 29 Ngwasiri Dickson Ngwanue Exercise 29Document3 pages29 Ngwasiri Dickson Ngwanue Exercise 29rita tamohNo ratings yet

- ACC2008 Lecture 4 - Advanced VariancesDocument42 pagesACC2008 Lecture 4 - Advanced VariancesSu-Kym TanNo ratings yet

- Standard Costing Practice Questions FinalDocument5 pagesStandard Costing Practice Questions FinalShehrozSTNo ratings yet

- KTQT-2 C10Document5 pagesKTQT-2 C10Huệ ĐặngNo ratings yet

- ABS Problems (1-2)Document3 pagesABS Problems (1-2)dewlate abinaNo ratings yet

- Management Accounting and Decision Making: Submitted ByDocument12 pagesManagement Accounting and Decision Making: Submitted ByKavisha singhNo ratings yet

- P1 Solution CMA JUNE 2020Document5 pagesP1 Solution CMA JUNE 2020Awal ShekNo ratings yet

- Standard Costing - Solutions To Home Work Problems: Question No: 19 Reconciliation With Finished Goods InventoryDocument7 pagesStandard Costing - Solutions To Home Work Problems: Question No: 19 Reconciliation With Finished Goods InventoryDevi ParameshNo ratings yet

- Whitestone Company: $ 658,800 654,225 $1,313,025 $43,005 F Price $ 691,740 664,290 $1,356,030 $16,470 U MixDocument4 pagesWhitestone Company: $ 658,800 654,225 $1,313,025 $43,005 F Price $ 691,740 664,290 $1,356,030 $16,470 U MixJashmin CosainNo ratings yet

- Cost and Management AccountingDocument7 pagesCost and Management AccountingJoseph PhaustineNo ratings yet

- UNIT5 Cost Accounting AssignmentDocument29 pagesUNIT5 Cost Accounting AssignmentRuby RosiosNo ratings yet

- Standard CostingDocument19 pagesStandard CostingCillian ReevesNo ratings yet

- FManAcc Teaching Week 11 Seminar Answers Part 1 2023 - 2024 - TaggedDocument5 pagesFManAcc Teaching Week 11 Seminar Answers Part 1 2023 - 2024 - Taggedredwaanmo19No ratings yet

- Accounting3 HW 7Document5 pagesAccounting3 HW 7jpNo ratings yet

- Standard Costing (I) - SolutionsDocument3 pagesStandard Costing (I) - Solutions行歌No ratings yet

- Standard Costing RS QuestionsDocument29 pagesStandard Costing RS QuestionsArnik AgarwalNo ratings yet

- Test 8Document1 pageTest 8Gamerz Den Pes 17No ratings yet

- Man Acc GRP 5 3 1 To 3 17 Answer SheetDocument15 pagesMan Acc GRP 5 3 1 To 3 17 Answer SheetMatthew Brian TajanlangitNo ratings yet

- BTVNDocument8 pagesBTVNTrâm PhươngNo ratings yet

- Chapter 08 - QuestionsDocument2 pagesChapter 08 - QuestionsgurnoorkaurgilllNo ratings yet

- MCV MPVDocument8 pagesMCV MPVHarsh MittalNo ratings yet

- Slide MA2Document11 pagesSlide MA2Afaf Naily100% (1)

- MfacDocument8 pagesMfacarronyeagarNo ratings yet

- Joint Products and By-ProductsDocument16 pagesJoint Products and By-ProductsAnmol AgalNo ratings yet

- Joint Product and by Product Costing For Online TeachingDocument9 pagesJoint Product and by Product Costing For Online Teachingfaith olaNo ratings yet

- Independent University, BangladeshDocument10 pagesIndependent University, BangladeshpritomNo ratings yet

- Tesr 10 Standard Costing and Variance AnalysisDocument1 pageTesr 10 Standard Costing and Variance AnalysisAnmoul ZahraNo ratings yet

- Full Mock 2 (Shriya)Document8 pagesFull Mock 2 (Shriya)Shriya SaralayaNo ratings yet

- Week 5 Variance AnalysisDocument43 pagesWeek 5 Variance AnalysisMichel BanvoNo ratings yet

- Problem10 18 and 10 20Document9 pagesProblem10 18 and 10 20DhanushaNo ratings yet

- Standard CostingDocument65 pagesStandard CostingSyed Hussam Haider Tirmazi100% (2)

- Chapter 11 Exercise and CaseDocument10 pagesChapter 11 Exercise and CaseVenus PalmencoNo ratings yet

- Master BudgetDocument8 pagesMaster BudgetScribdTranslationsNo ratings yet

- Standard CostingDocument16 pagesStandard CostingJash SanghviNo ratings yet

- Ch. 4 Yield Variances-NoteDocument11 pagesCh. 4 Yield Variances-Notesolomon adamuNo ratings yet

- Suraj T S (Me Cs 4)Document4 pagesSuraj T S (Me Cs 4)Suraj TSNo ratings yet

- CM Unit 3Document6 pagesCM Unit 3shanthala mNo ratings yet

- The Basics - 7 Bankroll Management - 1 Poker Bankroll ManagementDocument5 pagesThe Basics - 7 Bankroll Management - 1 Poker Bankroll ManagementOpawesomeNo ratings yet

- Statement of Axis Account No:080010100183918 For The Period (From: 19-10-2020 To: 18-10-2021)Document4 pagesStatement of Axis Account No:080010100183918 For The Period (From: 19-10-2020 To: 18-10-2021)Ketan PatelNo ratings yet

- Economic System of PakistanDocument6 pagesEconomic System of PakistanSyed Hassan Raza75% (4)

- Cash-And-Cash-Equivalent - Answers On HandoutDocument6 pagesCash-And-Cash-Equivalent - Answers On HandoutElaine AntonioNo ratings yet

- Indian Immunologicals Ltd.Document10 pagesIndian Immunologicals Ltd.Nani VolsNo ratings yet

- Jeevika Concept NoteDocument5 pagesJeevika Concept NoteSamir Kumar SahuNo ratings yet

- Chamber Maid's Trolley (Kashish 2)Document6 pagesChamber Maid's Trolley (Kashish 2)Piyush PriyadarshiNo ratings yet

- DPWH-INFR-45 ConMethDocument3 pagesDPWH-INFR-45 ConMethRayarch WuNo ratings yet

- Chapter 9 Cost EstimationDocument6 pagesChapter 9 Cost EstimationAli AhsanNo ratings yet

- 6-Module 6.2Document5 pages6-Module 6.2Juneil CortejosNo ratings yet

- 66 - 1 - 1 - Business StudiesDocument23 pages66 - 1 - 1 - Business StudiesbhaiyarakeshNo ratings yet

- LGSF ANNEX B Sample OnlyDocument2 pagesLGSF ANNEX B Sample OnlyRen Mathew QuitorianoNo ratings yet

- Tata-Aig General Insurance Company LTD: Policy No. 0238443404 / 0238443469 Claim No.Document3 pagesTata-Aig General Insurance Company LTD: Policy No. 0238443404 / 0238443469 Claim No.Mahendra SinghNo ratings yet

- ﻲﻟﺎﺣﻟا لوﻻا كﻧﺑﻟ بﺗارﻟا بﺎﺳﺣ Existing Alawwal Bank salary account ﮫﯾﻠﻋ ﻲﺑﺗار ﻊﻓدﻟ دﯾدﺟﻟا بﺎﺳ بﺎﺳﺣ New SABB account to pay my salary toDocument2 pagesﻲﻟﺎﺣﻟا لوﻻا كﻧﺑﻟ بﺗارﻟا بﺎﺳﺣ Existing Alawwal Bank salary account ﮫﯾﻠﻋ ﻲﺑﺗار ﻊﻓدﻟ دﯾدﺟﻟا بﺎﺳ بﺎﺳﺣ New SABB account to pay my salary tovijai_bhNo ratings yet

- Opex VSM Training Module 100711001122 Phpapp02Document53 pagesOpex VSM Training Module 100711001122 Phpapp02Jesus Jose Hernandez GuerreroNo ratings yet

- Bodie 11e PPT Ch08Document26 pagesBodie 11e PPT Ch08Fatimah AlashourNo ratings yet

- Ampoulel Section Equipment, HVAC List (Updated)Document4 pagesAmpoulel Section Equipment, HVAC List (Updated)fahadNo ratings yet

- Chapter 8: Accounting For Receivables: Exercise 1Document45 pagesChapter 8: Accounting For Receivables: Exercise 1jokerightwegmail.com joke1233No ratings yet

- Package Scheme of Incentive - 2019Document59 pagesPackage Scheme of Incentive - 2019GOYAL & AGRAWAL GOYAL & AGRAWALNo ratings yet

- Karl MarxDocument4 pagesKarl MarxFigen ErgürbüzNo ratings yet

- Deed of SaleDocument5 pagesDeed of SaleFelipe FamilyNo ratings yet

- UAQ Assignment 2 by RajeevDocument14 pagesUAQ Assignment 2 by RajeevRajeev KumarNo ratings yet

- Washers M24Document1 pageWashers M24jaseelNo ratings yet

- ARIMAX AnalysisDocument4 pagesARIMAX AnalysisJSNo ratings yet

- Potensi Pasar Sekunder Spektrum Frekuensi Radio Di IndonesiaDocument16 pagesPotensi Pasar Sekunder Spektrum Frekuensi Radio Di IndonesiaLodewijk SitompulNo ratings yet

- Chapter 2 Answers For EconomicsDocument5 pagesChapter 2 Answers For EconomicsterrancekuNo ratings yet

- Common NFT Form Rev 1Document2 pagesCommon NFT Form Rev 1Sree Siddarameshwara Agro IndustriesNo ratings yet

- ContractDocument3,272 pagesContractJanet VillarrealNo ratings yet

- Triveni Exp Third Ac (3A)Document2 pagesTriveni Exp Third Ac (3A)Anurag KumarNo ratings yet