You might also like

- Classification of Companies 2Document3 pagesClassification of Companies 2Chaudhry Adeel WaheedNo ratings yet

- Dawn Monday Economic StoryDocument9 pagesDawn Monday Economic StoryChaudhry Adeel WaheedNo ratings yet

- Presentation On Movie (The Day After Tomorrow)Document34 pagesPresentation On Movie (The Day After Tomorrow)Chaudhry Adeel WaheedNo ratings yet

- Profitability Merger Portfolio 27Document22 pagesProfitability Merger Portfolio 27Chaudhry Adeel WaheedNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

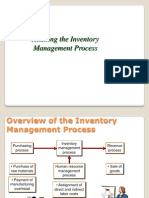

- Auditing The Inventory Management ProcessDocument15 pagesAuditing The Inventory Management ProcessGohar Mahmood100% (1)

- Financial Management PDFDocument397 pagesFinancial Management PDFArly Kurt TorresNo ratings yet

- Business ValuationDocument6 pagesBusiness ValuationlenoraNo ratings yet

- Kirschen SolutionsDocument10 pagesKirschen SolutionsRodrigo Alvim100% (1)

- Tutorial Budget2Document6 pagesTutorial Budget2Prashant KumarNo ratings yet

- FM 2016 Week 3 - Chapter 3Document86 pagesFM 2016 Week 3 - Chapter 3Wira MokiNo ratings yet

- A Study On Awareness of GST Among College Students in MumbaiDocument56 pagesA Study On Awareness of GST Among College Students in Mumbaisameep gourNo ratings yet

- Dentsply Sirona Q2 Earnings Presentation - FINALDocument18 pagesDentsply Sirona Q2 Earnings Presentation - FINALmedtechyNo ratings yet

- Model Test Paper-1Document24 pagesModel Test Paper-1Rupali RoyNo ratings yet

- B2B Chapter 3Document58 pagesB2B Chapter 3lkhakimNo ratings yet

- LSCM Unit-IiDocument21 pagesLSCM Unit-IiGangadhara RaoNo ratings yet

- ITC standalone balance sheet and profit and loss highlights 2021-22Document7 pagesITC standalone balance sheet and profit and loss highlights 2021-22jhanvi tandonNo ratings yet

- Financial Statement - Service CompanyDocument4 pagesFinancial Statement - Service CompanySherly Amalia DewiNo ratings yet

- Audit Liabilities Completeness ProceduresDocument3 pagesAudit Liabilities Completeness ProceduresJobby Jaranilla100% (1)

- Elasticity of Demand and SupplyDocument29 pagesElasticity of Demand and SupplyEmily Canlas DalmacioNo ratings yet

- Nature and Formation of Partnership - 2021Document6 pagesNature and Formation of Partnership - 2021LLYOD FRANCIS LAYLAYNo ratings yet

- Business PlanDocument18 pagesBusiness PlanAngelo Francis100% (2)

- Kanthal 2Document3 pagesKanthal 2Ramesh MandavaNo ratings yet

- ADocument7 pagesAAyad Abdelkarim NasirNo ratings yet

- Melody Joy Austria SWOT analysis and product lifecycleDocument3 pagesMelody Joy Austria SWOT analysis and product lifecycleMj AustriaNo ratings yet

- 7 Men Park Cars in Row Puzzle with 8 SolutionsDocument6 pages7 Men Park Cars in Row Puzzle with 8 Solutionssunny756No ratings yet

- Philippines Supreme Court rules no constructive receipt of dividends by estateDocument4 pagesPhilippines Supreme Court rules no constructive receipt of dividends by estateMj BrionesNo ratings yet

- Tally ACEDocument118 pagesTally ACESandhya Sandy0% (1)

- Agile Resilient Stronger: ASOS PLC Annual Report and Accounts 2020Document63 pagesAgile Resilient Stronger: ASOS PLC Annual Report and Accounts 2020Swapna Wedding Castle EramaloorNo ratings yet

- Chapter 4-Differential AnalysisDocument16 pagesChapter 4-Differential AnalysisVanessa HaliliNo ratings yet

- DTC Agreement Between United Arab Emirates and VenezuelaDocument26 pagesDTC Agreement Between United Arab Emirates and VenezuelaOECD: Organisation for Economic Co-operation and Development100% (1)

- Installment SalesDocument12 pagesInstallment SalesAllyzzaBuhain100% (1)

- Accounting Textbook Solutions - 60Document19 pagesAccounting Textbook Solutions - 60acc-expertNo ratings yet

- Role of Financial Manager (WEEK 2)Document15 pagesRole of Financial Manager (WEEK 2)Aliza Urtal100% (1)

- TrustDocument8 pagesTrustSaravananNo ratings yet