You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- W 2Document3 pagesW 2lysprr33% (3)

- Quiz Week 11 MODULE 10 Practice Quiz PDFDocument11 pagesQuiz Week 11 MODULE 10 Practice Quiz PDFKim100% (1)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 1-Consumption Tax ExercisesDocument2 pages1-Consumption Tax ExercisesVu Thi ThuongNo ratings yet

- IND 14 CHP 04 2A Textbook Problems 2012 SolutionsDocument20 pagesIND 14 CHP 04 2A Textbook Problems 2012 SolutionsrakutenmeeshoNo ratings yet

- Documents - 5ab25ae789bcd942d600247c - TCL00427 BCWPK5181K16 07 2019 17 22 39 PDFDocument5 pagesDocuments - 5ab25ae789bcd942d600247c - TCL00427 BCWPK5181K16 07 2019 17 22 39 PDFsadanand kanadeNo ratings yet

- Rise of AccountancyDocument1 pageRise of AccountancyiamneonkingNo ratings yet

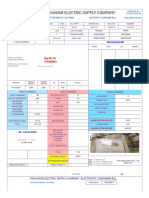

- Pesco Online BillDocument2 pagesPesco Online Billahad shahNo ratings yet

- Employes's Name Position Monthly Rate Gross Pay Sss-Ee Phic-Ee Hdmf-Ee Tax Loans Total Deduction Net PayDocument1 pageEmployes's Name Position Monthly Rate Gross Pay Sss-Ee Phic-Ee Hdmf-Ee Tax Loans Total Deduction Net PayBon.AlastoyNo ratings yet

- Sample Self Certification FormDocument1 pageSample Self Certification FormSai PastranaNo ratings yet

- Form10BE - ALPNA VARMA - 2021 - AABTK6329H06221000050Document1 pageForm10BE - ALPNA VARMA - 2021 - AABTK6329H06221000050hemalatha aNo ratings yet

- Saraf Real Infra Pvt. Ltd generates e-invoice and e-way bill for steel structure saleDocument2 pagesSaraf Real Infra Pvt. Ltd generates e-invoice and e-way bill for steel structure salemsNo ratings yet

- Solved An Investor in A 28 Tax Bracket Owns Land That PDFDocument1 pageSolved An Investor in A 28 Tax Bracket Owns Land That PDFAnbu jaromiaNo ratings yet

- Tax Deposit-Challan 281-Excel FormatDocument5 pagesTax Deposit-Challan 281-Excel FormatpreetNo ratings yet

- Philippine Airlines ticket receipt detailsDocument1 pagePhilippine Airlines ticket receipt detailsVideo TimeNo ratings yet

- Congratulations On Putting Your Family's Health First: Proforma InvoiceDocument1 pageCongratulations On Putting Your Family's Health First: Proforma InvoiceRamdas NagareNo ratings yet

- House Majority Forward's 2020 Tax FormsDocument49 pagesHouse Majority Forward's 2020 Tax FormsJoeSchoffstallNo ratings yet

- Tax Invoice DetailsDocument1 pageTax Invoice DetailsMonirul IslamNo ratings yet

- UMi Inc. Payroll ReportDocument10 pagesUMi Inc. Payroll ReportSeagate SilverNo ratings yet

- Romases Inc. Orporate Lawyer: ObjectivesDocument11 pagesRomases Inc. Orporate Lawyer: ObjectivesZyreen Silva GiduquioNo ratings yet

- Cipla Limited Cipla House Lower Parel: Payslip For The Month of NOVEMBER 2021Document2 pagesCipla Limited Cipla House Lower Parel: Payslip For The Month of NOVEMBER 2021Dhruv RanaNo ratings yet

- BPI Vs PosadasDocument2 pagesBPI Vs PosadasCarlota Nicolas VillaromanNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument2 pagesBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountPadma GouteNo ratings yet

- Salary AnnexureDocument1 pageSalary Annexuredpnair50% (4)

- Tax Rates Salaried Individuals 2022 2023Document2 pagesTax Rates Salaried Individuals 2022 2023by kirmaniNo ratings yet

- Bir Ruling 2021 - DST On Loan Exemption by PezaDocument5 pagesBir Ruling 2021 - DST On Loan Exemption by Pezajohn allen MarillaNo ratings yet

- Individual and corporate income tax ratesDocument4 pagesIndividual and corporate income tax ratesThe man with a Square stacheNo ratings yet

- Turning Point USA - FY 2016 990Document36 pagesTurning Point USA - FY 2016 990Lachlan MarkayNo ratings yet

- Indian Income Tax Return AcknowledgementDocument1 pageIndian Income Tax Return AcknowledgementRahul KashyapNo ratings yet

- Fundamentals of Taxation 2017 Edition 10Th Edition Cruz Solutions Manual Full Chapter PDFDocument47 pagesFundamentals of Taxation 2017 Edition 10Th Edition Cruz Solutions Manual Full Chapter PDFmarushiapatrina100% (12)

- $RN8C7G2Document3 pages$RN8C7G2akxerox47No ratings yet