You might also like

- Shaking Tables Around The WorldDocument15 pagesShaking Tables Around The Worlddjani_ip100% (1)

- PLM in The Automotive IndustryDocument11 pagesPLM in The Automotive IndustryHussam AliNo ratings yet

- A Case Study of Toyota Marketing EssayDocument8 pagesA Case Study of Toyota Marketing EssayHND Assignment HelpNo ratings yet

- Operations Management in Automotive Industries: From Industrial Strategies to Production Resources Management, Through the Industrialization Process and Supply Chain to Pursue Value CreationFrom EverandOperations Management in Automotive Industries: From Industrial Strategies to Production Resources Management, Through the Industrialization Process and Supply Chain to Pursue Value CreationNo ratings yet

- Car InovationDocument3 pagesCar InovationClaudiu KLodNo ratings yet

- Oliver Wyman Car InnovationDocument32 pagesOliver Wyman Car InnovationKhizra JamalNo ratings yet

- Hyundai 091124091217 Phpapp02Document62 pagesHyundai 091124091217 Phpapp02mbogadhiNo ratings yet

- Dissertation Topics Automobile IndustryDocument8 pagesDissertation Topics Automobile IndustryWriteMyEconomicsPaperUK100% (1)

- A001 Lean A Key Success Factor in Automobile IndustryDocument7 pagesA001 Lean A Key Success Factor in Automobile Industryarvindchopra3kNo ratings yet

- Research Papers Automobile IndustryDocument5 pagesResearch Papers Automobile Industryqbqkporhf100% (1)

- A Nano Car in Every DrivewayDocument13 pagesA Nano Car in Every DrivewayRajendra PetheNo ratings yet

- Ford Automobile Industry Case StudyDocument10 pagesFord Automobile Industry Case StudyUpendra SharmaNo ratings yet

- AutoDocument8 pagesAutoShwetank TNo ratings yet

- 2014 BCG - Accelerating InnovationDocument20 pages2014 BCG - Accelerating InnovationikhabibullinNo ratings yet

- Cost Reduction Techniques FinalDocument75 pagesCost Reduction Techniques FinalJig HiraniNo ratings yet

- Thesis AutomotiveDocument7 pagesThesis Automotiveheatherdionnemanchester100% (2)

- Mastering Engineering Service Outsourcing in The Automotive IndustryDocument40 pagesMastering Engineering Service Outsourcing in The Automotive IndustryArchitNo ratings yet

- Automotive Thesis ExampleDocument6 pagesAutomotive Thesis Examplednqjxbz2100% (2)

- Changing Trends in The Auto Ancillary Industry: FlexibilityDocument4 pagesChanging Trends in The Auto Ancillary Industry: FlexibilitymanishaNo ratings yet

- Automotive Industry Dissertation TopicsDocument4 pagesAutomotive Industry Dissertation TopicsNeedHelpWithPaperErie100% (1)

- China's Growing Auto Supply ChainsDocument40 pagesChina's Growing Auto Supply ChainsGary MaoNo ratings yet

- Research Paper On Automobile PartsDocument4 pagesResearch Paper On Automobile Partsrvpchmrhf100% (1)

- Daimler Chrysler MergerDocument49 pagesDaimler Chrysler MergerSamir Saffari100% (1)

- Sustainable Development: Opportunity or Threat For The Auto Industry?Document7 pagesSustainable Development: Opportunity or Threat For The Auto Industry?lalou4No ratings yet

- Delloite AutomotiveDocument28 pagesDelloite AutomotiveKsl Vajrala100% (1)

- Team 5 Industry PaperDocument23 pagesTeam 5 Industry Paperapi-315687330No ratings yet

- German Automobile IndustryDocument9 pagesGerman Automobile IndustryAshik ChowdhuryNo ratings yet

- 10% AssignmentDocument4 pages10% Assignment99045448No ratings yet

- Planning a 2,000 Unit A00 Class Car FactoryDocument46 pagesPlanning a 2,000 Unit A00 Class Car FactoryJesu RajNo ratings yet

- Book - Automotive Technology RoadmapDocument458 pagesBook - Automotive Technology RoadmapSunil Deshpande100% (1)

- Engine Manufacturing CompanyDocument11 pagesEngine Manufacturing CompanyperminderlbwNo ratings yet

- Mid Term P&ODocument5 pagesMid Term P&OHADLIZAN BIN MOHZAN (B19361012)No ratings yet

- India's Growing Automobile Industry Attracts Global MajorsDocument3 pagesIndia's Growing Automobile Industry Attracts Global MajorsSayan KunduNo ratings yet

- Porter's Five Forces Model On Automobile IndustryDocument6 pagesPorter's Five Forces Model On Automobile IndustryBhavinShankhalparaNo ratings yet

- Automobile IndustryDocument30 pagesAutomobile IndustrychakshuNo ratings yet

- Fdi in Automobile Sector in IndiaDocument26 pagesFdi in Automobile Sector in Indiauditnarula09No ratings yet

- European Car Market: Business Plan: Mission StatementDocument3 pagesEuropean Car Market: Business Plan: Mission Statementd445390No ratings yet

- The Automobile Manufacturing IndustryDocument3 pagesThe Automobile Manufacturing Industrysaur.latadNo ratings yet

- CtimagDocument40 pagesCtimagDeepak Chachra100% (1)

- ITT AutomotiveDocument3 pagesITT AutomotiveVisweswara Reddy100% (1)

- Industry ProfileDocument3 pagesIndustry ProfileSathish UrfriendNo ratings yet

- Knowledge Management in The Automobile Industry - FinalDocument13 pagesKnowledge Management in The Automobile Industry - FinalAshrafAbdoSNo ratings yet

- Papazoglou Webserv 2e Cs Solution Notes Part1Document26 pagesPapazoglou Webserv 2e Cs Solution Notes Part1TALALQUIDERNo ratings yet

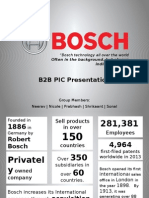

- B2B PIC Presentation: Often in The Background, But Always Indispensable."Document28 pagesB2B PIC Presentation: Often in The Background, But Always Indispensable."KiaraSinghNo ratings yet

- Car Company ReportDocument10 pagesCar Company ReportTrident ManagementNo ratings yet

- Sciencedirect: New Opportunities and Incentives For Remanufacturing by 2020 S Car Service TrendsDocument6 pagesSciencedirect: New Opportunities and Incentives For Remanufacturing by 2020 S Car Service TrendsAlexandra RenteaNo ratings yet

- A Nano Car in Every Driveway PDFDocument8 pagesA Nano Car in Every Driveway PDFAshwani MattooNo ratings yet

- Factors Affecting Four Wheeler Industries in IndiaDocument54 pagesFactors Affecting Four Wheeler Industries in IndiaRitesh Vaishnav100% (2)

- ITT AutomotiveDocument3 pagesITT AutomotiveAnuragNo ratings yet

- Market Adaptation of Volkswagen PoloDocument36 pagesMarket Adaptation of Volkswagen PoloRohit Sopori100% (1)

- A Seminar Report On "Automobile Sector of India"Document33 pagesA Seminar Report On "Automobile Sector of India"Mohammad Anwar Ali100% (1)

- Automotive Supplier Innovation Management SystemDocument13 pagesAutomotive Supplier Innovation Management Systemjmoreno434No ratings yet

- Q 02 Assignment NissanDocument17 pagesQ 02 Assignment NissankiranatifNo ratings yet

- E - Commerce in Automotive Component IndustryDocument12 pagesE - Commerce in Automotive Component IndustryfaruquepgdmNo ratings yet

- Executive SummaryDocument20 pagesExecutive SummarySachin UmbarajeNo ratings yet

- A Study On Measuring The Service Quality of Car Dealers in AllepeyDocument66 pagesA Study On Measuring The Service Quality of Car Dealers in AllepeyshashimuraliNo ratings yet

- Ieee FileDocument4 pagesIeee FileGhanshyam PrajapatNo ratings yet

- June 2010 (v1) QP - Paper 1 CIE Economics IGCSEDocument12 pagesJune 2010 (v1) QP - Paper 1 CIE Economics IGCSEjoseph oukoNo ratings yet

- Revised approval for 132/33kV substation in ElchuruDocument2 pagesRevised approval for 132/33kV substation in ElchuruHareesh KumarNo ratings yet

- Method Statement-Site CleaningDocument6 pagesMethod Statement-Site Cleaningprisma integrated100% (1)

- Project Report SSIDocument140 pagesProject Report SSIharsh358No ratings yet

- Analysis of Marketing Mix of Honda Cars in IndiaDocument25 pagesAnalysis of Marketing Mix of Honda Cars in Indiaamitkumar_npg7857100% (5)

- Dgcis Report Kolkata PDFDocument12 pagesDgcis Report Kolkata PDFABCDNo ratings yet

- Global Trends AssignmentDocument9 pagesGlobal Trends Assignmentjan yeabuki100% (2)

- MSDS Blattanex Gel PDFDocument5 pagesMSDS Blattanex Gel PDFIsna AndriantoNo ratings yet

- ICA Ghana Exemption FormDocument1 pageICA Ghana Exemption Form3944/95No ratings yet

- GMG AirlineDocument15 pagesGMG AirlineabusufiansNo ratings yet

- Biblioteca Ingenieria Petrolera 2015Document54 pagesBiblioteca Ingenieria Petrolera 2015margaritaNo ratings yet

- Quan Tri TCQTDocument44 pagesQuan Tri TCQTHồ NgânNo ratings yet

- Indgiro 20181231 PDFDocument1 pageIndgiro 20181231 PDFHuiwen Cheok100% (1)

- Rancang Bangun Alat Mixer Vertikal Adonan Kue Donat Dengan Gearbox Tipe Bevel Gear Kapasitas 7 KilogramDocument6 pagesRancang Bangun Alat Mixer Vertikal Adonan Kue Donat Dengan Gearbox Tipe Bevel Gear Kapasitas 7 KilogramRachmad RisaldiNo ratings yet

- Microeconomics Chapter 1 IntroDocument28 pagesMicroeconomics Chapter 1 IntroMc NierraNo ratings yet

- Manufacturing Resources PlanningDocument5 pagesManufacturing Resources PlanningSachin SalvanikarNo ratings yet

- Briefing Note: "2011 - 2014 Budget and Taxpayer Savings"Document6 pagesBriefing Note: "2011 - 2014 Budget and Taxpayer Savings"Jonathan Goldsbie100% (1)

- TPS and ERPDocument21 pagesTPS and ERPTriscia QuiñonesNo ratings yet

- Tata Motors Suv Segment ProjectDocument57 pagesTata Motors Suv Segment ProjectmonikaNo ratings yet

- F Business Taxation 671079211Document4 pagesF Business Taxation 671079211anand0% (1)

- Kunal Uniforms CNB TxnsDocument2 pagesKunal Uniforms CNB TxnsJanu JanuNo ratings yet

- Fair & Lovely Born: 1978 History: The Fairness Cream Brand Was Developed by Hindustan Lever LTDDocument3 pagesFair & Lovely Born: 1978 History: The Fairness Cream Brand Was Developed by Hindustan Lever LTDNarendra KumarNo ratings yet

- Proposal Letter of B 2 B Redeifined Angel (2) (1) 3 (New)Document3 pagesProposal Letter of B 2 B Redeifined Angel (2) (1) 3 (New)Hardy TomNo ratings yet

- Management of Environmental Quality: An International JournalDocument21 pagesManagement of Environmental Quality: An International Journalmadonna rustomNo ratings yet

- Becker Friedman Institute Annual Report 2013-14Document24 pagesBecker Friedman Institute Annual Report 2013-14bficommNo ratings yet

- MTNL Mumbai PlansDocument3 pagesMTNL Mumbai PlansTravel HelpdeskNo ratings yet

- Princeton Economics Archive Three-Faces-Inflation PDFDocument3 pagesPrinceton Economics Archive Three-Faces-Inflation PDFadamvolkovNo ratings yet

- Credit Decision ManagementDocument14 pagesCredit Decision ManagementSat50% (2)

- BELENDocument22 pagesBELENLuzbe BelenNo ratings yet