You might also like

- PSAK 53-RevDocument18 pagesPSAK 53-Revapi-3708783No ratings yet

- Psak 42Document15 pagesPsak 42api-3708783100% (1)

- PSAK 54-RevDocument11 pagesPSAK 54-Revapi-3708783100% (3)

- PSAK 52-RevDocument9 pagesPSAK 52-Revapi-3708783No ratings yet

- PSAK 39-RevDocument13 pagesPSAK 39-Revapi-3708783No ratings yet

- PSAK 55-revFPDocument23 pagesPSAK 55-revFPapi-3708783100% (1)

- PSAK 50-RevDocument9 pagesPSAK 50-Revapi-3708783100% (1)

- PSAK 51-RevDocument5 pagesPSAK 51-Revapi-3708783No ratings yet

- Psak 49Document11 pagesPsak 49api-3708783100% (2)

- Psak 44 Real Estate Ver171299Document20 pagesPsak 44 Real Estate Ver171299api-3708783No ratings yet

- PSAK 47-RevDocument11 pagesPSAK 47-Revapi-3708783100% (1)

- Psak 38Document7 pagesPsak 38api-3708783No ratings yet

- PSAK 48 Reduction in Val VER171299Document19 pagesPSAK 48 Reduction in Val VER171299api-3708783No ratings yet

- Psak 46Document15 pagesPsak 46api-3708783100% (1)

- Psak 43Document9 pagesPsak 43api-3708783No ratings yet

- PSAK 41-RevDocument6 pagesPSAK 41-Revapi-3708783No ratings yet

- Psak 34Document20 pagesPsak 34api-3708783No ratings yet

- Psak 37Document12 pagesPsak 37api-3708783100% (1)

- Psak 35Document8 pagesPsak 35api-3708783100% (1)

- Psak 33Document19 pagesPsak 33api-3708783No ratings yet

- PSAK 40-RevDocument15 pagesPSAK 40-Revapi-3708783No ratings yet

- Psak 36Document28 pagesPsak 36api-3708783No ratings yet

- Psak 32Document14 pagesPsak 32api-3708783100% (1)

- Psak 30Document8 pagesPsak 30api-3708783No ratings yet

- Psak 45 Npo Ver171299Document23 pagesPsak 45 Npo Ver171299api-3708783100% (1)

- Psak 28Document16 pagesPsak 28api-3708783100% (1)

- PSAK 27 (98 RevDocument19 pagesPSAK 27 (98 Revapi-3708783No ratings yet

- Financial Accounting Standard 25 Association of Indonesian AccountantsDocument15 pagesFinancial Accounting Standard 25 Association of Indonesian Accountantsapi-3708783100% (1)

- PSAK 26 (1997 Revision)Document8 pagesPSAK 26 (1997 Revision)api-3708783No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Design Build AgreementDocument7 pagesDesign Build AgreementJaseTanNo ratings yet

- 51369-Intuit-QB-Core Glossary-V02-RJCDocument14 pages51369-Intuit-QB-Core Glossary-V02-RJCgayle aldoNo ratings yet

- Risk Management Process AnalysisDocument15 pagesRisk Management Process AnalysisAyat KhanNo ratings yet

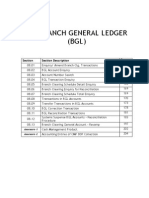

- 01 08-BGLDocument40 pages01 08-BGLmevrick_guy100% (2)

- Application Form Cgrs@ibps - inDocument24 pagesApplication Form Cgrs@ibps - inGouthamNaikNo ratings yet

- Danske Bank Message Implement at Ion Guide Multiple Credit Advice (Edifact D.96A - Cremul)Document32 pagesDanske Bank Message Implement at Ion Guide Multiple Credit Advice (Edifact D.96A - Cremul)aNo ratings yet

- 5369 14-08-2019 129455Document3 pages5369 14-08-2019 129455Achal Kumar0% (1)

- Kanchan YadavDocument14 pagesKanchan YadavNandini JaganNo ratings yet

- Bank Statement Template 19Document4 pagesBank Statement Template 19Thai Chu DinhNo ratings yet

- Account Name BSB Account Number Account Type Date OpenedDocument6 pagesAccount Name BSB Account Number Account Type Date OpenedSandeep TuladharNo ratings yet

- Builder NOC FormatDocument2 pagesBuilder NOC FormatvikrameyeNo ratings yet

- Coupon Code: TIMES600: Rs. 600 OffDocument15 pagesCoupon Code: TIMES600: Rs. 600 OffRaghavNo ratings yet

- Bab 6 Akuntansi Untuk Perusahaan DagangDocument76 pagesBab 6 Akuntansi Untuk Perusahaan DagangBaskaraaryaNo ratings yet

- Zions Bank: Business Internet Banking User'S GuideDocument24 pagesZions Bank: Business Internet Banking User'S GuideSachin KulgodNo ratings yet

- The Influence of Online Shopping Determinants On Customer Satisfaction in The Serbian MarketDocument28 pagesThe Influence of Online Shopping Determinants On Customer Satisfaction in The Serbian MarketDAVID WONG LEE KANG LEE KANGNo ratings yet

- Chapter 11 Test Bank Test BankDocument25 pagesChapter 11 Test Bank Test BankAyesha BajwaNo ratings yet

- Introduction To Big BazaarDocument8 pagesIntroduction To Big BazaarSaksham AgarwalNo ratings yet

- Theme 7 Front OfficeDocument35 pagesTheme 7 Front OfficeСофи БреславецNo ratings yet

- EXPORT FINANCE GUIDEDocument33 pagesEXPORT FINANCE GUIDEPrashant ShettigarNo ratings yet

- Northern Region Transmission System-Ii: Recruitment For The Post of Diploma Trainee (Electrical) in Nrts-IiDocument3 pagesNorthern Region Transmission System-Ii: Recruitment For The Post of Diploma Trainee (Electrical) in Nrts-IiakashthecosmosNo ratings yet

- iSHRAQ Islamic Finance PlatformDocument18 pagesiSHRAQ Islamic Finance PlatformahmedzafarNo ratings yet

- SGC TokenDocument76 pagesSGC TokenRicky PerdanaNo ratings yet

- Bhansali Invento SystemDocument18 pagesBhansali Invento SystemJeje OiNo ratings yet

- Alibaba Payment, Shipping & Refund GuideDocument24 pagesAlibaba Payment, Shipping & Refund Guidekafala lalimaNo ratings yet

- Voucher TypeDocument32 pagesVoucher TypePool KingNo ratings yet

- Principles of Banking 9th EditionDocument374 pagesPrinciples of Banking 9th EditionDoãn VyNo ratings yet

- NACHA Format SpecificationDocument14 pagesNACHA Format SpecificationAshok BogavalliNo ratings yet

- Internship ReportDocument14 pagesInternship ReportVanitha100% (1)

- Plastic Money: An Introduction to Credit and Debit CardsDocument20 pagesPlastic Money: An Introduction to Credit and Debit CardsJeetu VermaNo ratings yet

- Form A-1 (For Import Payments Only) : Open General LicenceDocument6 pagesForm A-1 (For Import Payments Only) : Open General LicenceAmit MittalNo ratings yet