You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- TP Accounting For Decision Making ZimmermanDocument1 pageTP Accounting For Decision Making Zimmermanapi-3820619No ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Rewriting The Rules For India's BanksDocument4 pagesRewriting The Rules For India's Banksapi-3820619No ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- L32 Audit As Control ToolDocument12 pagesL32 Audit As Control Toolapi-3820619No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Emerging Market Mania: Is It Different This Time?Document3 pagesEmerging Market Mania: Is It Different This Time?api-3820619No ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- L30 The Balanced Scoreboard BLUEDocument14 pagesL30 The Balanced Scoreboard BLUEapi-3820619100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- L21 Long Range PlanningDocument7 pagesL21 Long Range Planningapi-3820619No ratings yet

- L27 MCS in Service IndDocument13 pagesL27 MCS in Service Indapi-3820619No ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- L28 29 Non Financial Measures of Performance EvaluationDocument11 pagesL28 29 Non Financial Measures of Performance Evaluationapi-3820619100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- L20 Bench MarkingDocument6 pagesL20 Bench Markingapi-3820619No ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- L31 Total Cost ManagementDocument13 pagesL31 Total Cost Managementapi-3820619No ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- L22 Scope of MCS SP OP MC TransparencyDocument1 pageL22 Scope of MCS SP OP MC Transparencyapi-3820619No ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- L23 BudgetingDocument11 pagesL23 Budgetingapi-3820619No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

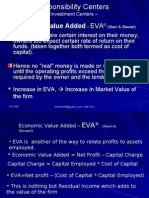

- L19 RC Problems On ROI and EVADocument8 pagesL19 RC Problems On ROI and EVAapi-3820619100% (2)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- L16 Problem On Transfer PricingDocument20 pagesL16 Problem On Transfer Pricingapi-382061990% (20)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- L17 RC Investment Center ROIDocument13 pagesL17 RC Investment Center ROIapi-3820619100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- L15 L16 Problems On TPDocument15 pagesL15 L16 Problems On TPapi-3820619No ratings yet

- L10 RC Revenue and Eng ExpensesDocument14 pagesL10 RC Revenue and Eng Expensesapi-3820619No ratings yet

- L18 RC Invest Centers EVADocument13 pagesL18 RC Invest Centers EVAapi-3820619No ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- L12 Problem On Profitability Measures For Profit CenterDocument8 pagesL12 Problem On Profitability Measures For Profit Centerapi-3820619No ratings yet

- L14 TP Cost Based MethodDocument9 pagesL14 TP Cost Based Methodapi-3820619No ratings yet

- L15 Other Methods of TPDocument2 pagesL15 Other Methods of TPapi-3820619No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- XL100 RC Disc Exp Added in L10Document5 pagesXL100 RC Disc Exp Added in L10api-3820619No ratings yet

- L9 Input Output RelationshipDocument6 pagesL9 Input Output Relationshipapi-3820619No ratings yet

- L13 TP MKT Based MethodDocument8 pagesL13 TP MKT Based Methodapi-3820619No ratings yet

- XL330 JIT RemovedDocument2 pagesXL330 JIT Removedapi-3820619No ratings yet

- XL260 Ratio RemovedDocument20 pagesXL260 Ratio Removedapi-3820619No ratings yet

- XL260 Variance RemovedDocument11 pagesXL260 Variance Removedapi-3820619No ratings yet

- L8 MCS Formal ProcessDocument3 pagesL8 MCS Formal Processapi-3820619100% (1)

- L7 Goal Congruence MCS Form ProcessDocument10 pagesL7 Goal Congruence MCS Form Processapi-3820619100% (7)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Program Management Office (Pgmo) : Keane White PaperDocument19 pagesProgram Management Office (Pgmo) : Keane White PaperOsama A. AliNo ratings yet

- 3-Import ExportDocument13 pages3-Import ExportStephiel SumpNo ratings yet

- A Closed-Form GARCH Option Pricing ModelDocument34 pagesA Closed-Form GARCH Option Pricing ModelBhuwanNo ratings yet

- Topic 4 AnnuityDocument22 pagesTopic 4 AnnuityNanteni GanesanNo ratings yet

- Core Areas of Corporate Strategy: Èc V ( (Èc V (ÈcvDocument16 pagesCore Areas of Corporate Strategy: Èc V ( (Èc V (ÈcvSandip NandyNo ratings yet

- CSR PresentationDocument19 pagesCSR PresentationBhavi007No ratings yet

- My Report Internal AssessmentDocument18 pagesMy Report Internal AssessmentGlenn John BalongagNo ratings yet

- 8 Fair Value Measurement 6/12: 7.5 Capital DisclosuresDocument9 pages8 Fair Value Measurement 6/12: 7.5 Capital Disclosuresusman aliNo ratings yet

- Section 2. Original Certificates of Title Shall Be Reconstituted From Such of TheDocument2 pagesSection 2. Original Certificates of Title Shall Be Reconstituted From Such of TheAlexylle ConcepcionNo ratings yet

- Top Law Firm in Dubai, UAE - RAALCDocument20 pagesTop Law Firm in Dubai, UAE - RAALCraalc uaeNo ratings yet

- FINC2011 Corporate Finance I: Semester 2, 2019Document1 pageFINC2011 Corporate Finance I: Semester 2, 2019Jackson ChenNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Quiz Cash FlowDocument3 pagesQuiz Cash FlowMumbo Jumbo100% (1)

- FICO Configuration Transaction CodesDocument3 pagesFICO Configuration Transaction CodesSoumitra MondalNo ratings yet

- Diagnosing Seaweed Value Chains in Sumenep, MaduraDocument66 pagesDiagnosing Seaweed Value Chains in Sumenep, MaduraEly John KarimelaNo ratings yet

- Clearance Procedures for ImportsDocument36 pagesClearance Procedures for ImportsNina Bianca Espino100% (1)

- Three Innate Powers of the StateDocument30 pagesThree Innate Powers of the StateayasueNo ratings yet

- Sustainability 13 03746 v2Document15 pagesSustainability 13 03746 v2thyb2015571No ratings yet

- Solution Manual Chapter 1Document52 pagesSolution Manual Chapter 1octorp77% (13)

- 6939 - Cash and Accruals BasisDocument5 pages6939 - Cash and Accruals BasisAljur SalamedaNo ratings yet

- Atlantic City Recovery Plan in Brief 10.24.2016 - FINALDocument23 pagesAtlantic City Recovery Plan in Brief 10.24.2016 - FINALPress of Atlantic CityNo ratings yet

- Pre-Incorporation Founders Agreement SummaryDocument13 pagesPre-Incorporation Founders Agreement SummaryAmal Mulia100% (2)

- 中国经济中长期发展和转型 国际视角的思考与建议Document116 pages中国经济中长期发展和转型 国际视角的思考与建议penweiNo ratings yet

- SGC Composition and FunctionsDocument2 pagesSGC Composition and FunctionsDecember Cool100% (5)

- Capital Budgeting Practices in PunjabDocument20 pagesCapital Budgeting Practices in PunjabChandna MaryNo ratings yet

- Level of Financial Literacy (HUMSS 4, Macrohon Group)Document37 pagesLevel of Financial Literacy (HUMSS 4, Macrohon Group)Charyl MorenoNo ratings yet

- CV Marius Horincar 2010Document5 pagesCV Marius Horincar 2010Stoicescu VladNo ratings yet

- CXC 20180206 PDFDocument16 pagesCXC 20180206 PDFJoshua BlackNo ratings yet

- Solutions For Non-Constant Growth Stock ValuationsDocument2 pagesSolutions For Non-Constant Growth Stock ValuationsNguyễn Bá Khánh TùngNo ratings yet

- Chapter 5 - Sources of CapitalDocument42 pagesChapter 5 - Sources of CapitalLIEW YU LIANGNo ratings yet

- Tissue Paper Converting Unit Rs. 36.22 Million Mar-2020Document29 pagesTissue Paper Converting Unit Rs. 36.22 Million Mar-2020Rana Muhammad Ayyaz Rasul100% (1)