You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- TESTBANK MANAGEMENT ACCOUNTING - Chapter10Document41 pagesTESTBANK MANAGEMENT ACCOUNTING - Chapter10King Mercado100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Digitisation Big Data and The Transformation of Accounting InformationDocument23 pagesDigitisation Big Data and The Transformation of Accounting InformationKomathi Mathi100% (1)

- Solution Manual For Managerial Accounting 10th Edition by HiltonDocument19 pagesSolution Manual For Managerial Accounting 10th Edition by Hiltona46078460233% (3)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Cost-Volume Profit AnalysisDocument26 pagesCost-Volume Profit AnalysisClarizza20% (5)

- 4 and 5Document3 pages4 and 5Mela carlonNo ratings yet

- Retail Brand ManagementDocument8 pagesRetail Brand Managementapi-3716588100% (6)

- 4th ClassDocument13 pages4th Classapi-3716588No ratings yet

- Industry Analysis and Competitive AnalysisDocument6 pagesIndustry Analysis and Competitive Analysisapi-3716588No ratings yet

- Commercial Banking - 1Document31 pagesCommercial Banking - 1api-3716588No ratings yet

- Retail ConsumerDocument11 pagesRetail Consumerapi-3716588100% (2)

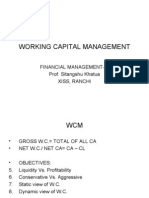

- Working Capital Management: Financial Management - Ii Prof. Sitangshu Khatua Xiss, RanchiDocument10 pagesWorking Capital Management: Financial Management - Ii Prof. Sitangshu Khatua Xiss, Ranchiapi-3716588No ratings yet

- Retail StrategyDocument27 pagesRetail Strategyapi-3716588100% (17)

- Introduction To RetailDocument13 pagesIntroduction To Retailapi-3716588100% (2)

- Acma - 5-6Document7 pagesAcma - 5-6api-3716588No ratings yet

- Trade FinanceDocument40 pagesTrade Financeapi-371658880% (5)

- Medium & Long Term FinanceDocument67 pagesMedium & Long Term Financeapi-3716588100% (2)

- Indian Investment AbroadDocument17 pagesIndian Investment Abroadapi-3716588No ratings yet

- Foreign Investment in IndiaDocument43 pagesForeign Investment in Indiaapi-3716588100% (2)

- Acma - 9-10Document3 pagesAcma - 9-10api-3716588No ratings yet

- DerivativesDocument53 pagesDerivativesapi-3716588100% (1)

- Acma - 7-8Document8 pagesAcma - 7-8api-3716588No ratings yet

- 6 Gap 1Document10 pages6 Gap 1api-3716588No ratings yet

- MFI-Ch1a (Ec Growth & Fin Inst)Document5 pagesMFI-Ch1a (Ec Growth & Fin Inst)api-3716588No ratings yet

- Management of Financial Institutions Syllabus 2006-08Document7 pagesManagement of Financial Institutions Syllabus 2006-08api-3716588No ratings yet

- MFI CH 1b (Financial System & Fin Inst)Document4 pagesMFI CH 1b (Financial System & Fin Inst)api-3716588No ratings yet

- MFI CH 1c (Money MKT & Cap MKT Inst)Document12 pagesMFI CH 1c (Money MKT & Cap MKT Inst)api-3716588No ratings yet

- ExerciseDocument2 pagesExerciseapi-3716588No ratings yet

- Commercial BankingDocument7 pagesCommercial Bankingapi-3716588100% (1)

- 5 Cust PerceptionsDocument20 pages5 Cust Perceptionsapi-3716588100% (2)

- Central Banking System & RBIDocument50 pagesCentral Banking System & RBIapi-3716588No ratings yet

- 2 Intro To Serv MarDocument23 pages2 Intro To Serv Marapi-3716588100% (2)

- 1 Course Contents Serv MarDocument12 pages1 Course Contents Serv Marapi-3716588100% (2)

- 3rd Class FinDocument14 pages3rd Class Finapi-3716588No ratings yet

- Solution Manual For Managerial Accounting: Creating Value in A Dynamic Business Environment, 12th Edition, Ronald Hilton, David PlattDocument36 pagesSolution Manual For Managerial Accounting: Creating Value in A Dynamic Business Environment, 12th Edition, Ronald Hilton, David Plattdoomsmanaventailti63q100% (17)

- Job Orede CostingDocument13 pagesJob Orede Costingአረጋዊ ሐይለማርያምNo ratings yet

- Pile cp2Document108 pagesPile cp2casarokarNo ratings yet

- Cost Management TechniquesDocument12 pagesCost Management TechniquesRavi MaheshwariNo ratings yet

- A MANGO Final 2015 16 Annual Report and Accounts Unsigned For Web PDFDocument41 pagesA MANGO Final 2015 16 Annual Report and Accounts Unsigned For Web PDFladyfngrNo ratings yet

- Management Accounting Advantages for MSMEsDocument10 pagesManagement Accounting Advantages for MSMEsTin Bernadette DominicoNo ratings yet

- Joint ProbabilityDocument8 pagesJoint Probability203 764 SwathiNo ratings yet

- Coursehero Com Solved Miller Toy Company Manufactures A PlasticDocument3 pagesCoursehero Com Solved Miller Toy Company Manufactures A PlasticAlphaNo ratings yet

- Report On Cost of ProductionDocument34 pagesReport On Cost of ProductionUnique OmarNo ratings yet

- BOB Finance & Credit Specialist Officer SII Model Question Paper 4Document147 pagesBOB Finance & Credit Specialist Officer SII Model Question Paper 4Pranav KumarNo ratings yet

- CIMA P1 Free Study Notes for November 2019 ExamsDocument112 pagesCIMA P1 Free Study Notes for November 2019 ExamsNassib SongoroNo ratings yet

- Flexible BudgetingDocument12 pagesFlexible BudgetingrajyalakshmiNo ratings yet

- Chapter 5 - Product and Service Costing: Job-Order SystemDocument71 pagesChapter 5 - Product and Service Costing: Job-Order SystemIllion Illion0% (1)

- Chap002 Basic Cost ManagementDocument36 pagesChap002 Basic Cost ManagementAneukphon Ryan Pramanda IsniNo ratings yet

- ACCOUNTING AND FINANCE Exit ExamDocument10 pagesACCOUNTING AND FINANCE Exit Examhaile93% (44)

- Nobles Acct10 Tif 21Document205 pagesNobles Acct10 Tif 21Marqaz MarqazNo ratings yet

- Latihan CVPDocument2 pagesLatihan CVPAchmad RidwanNo ratings yet

- Unit 1 - Introduction To Cost and Management AccountingDocument18 pagesUnit 1 - Introduction To Cost and Management AccountingAayushi KothariNo ratings yet

- Finance & Accounting Books Vikas PublicationsDocument26 pagesFinance & Accounting Books Vikas PublicationsShiva Johri100% (1)

- Scoman1 Final Outputs 1Document10 pagesScoman1 Final Outputs 1Kent Chester CooNo ratings yet

- Cost and Management Accounting - Course OutlineDocument9 pagesCost and Management Accounting - Course OutlineJajJay100% (1)

- Chapter 3 Solutions Comm 305Document77 pagesChapter 3 Solutions Comm 305mike100% (1)

- Chapter 2 Problem SolutionsDocument5 pagesChapter 2 Problem SolutionsHoàng HuyNo ratings yet

- SCDL Assignments Question Bank - Principle N Practices 1Document4 pagesSCDL Assignments Question Bank - Principle N Practices 1Tarun Chhabra100% (1)

- Final Exam FRC - M. Gerry Naufal. R. G. - 29123123Document19 pagesFinal Exam FRC - M. Gerry Naufal. R. G. - 29123123m.gerryNo ratings yet