You might also like

- Fitness by Design V CirDocument3 pagesFitness by Design V Cirleighsiazon100% (1)

- Contract Accounting PDFDocument29 pagesContract Accounting PDFrachel100% (1)

- Accounting Standard-7: Construction ContractsDocument35 pagesAccounting Standard-7: Construction Contractsshaan0099No ratings yet

- The Contractor Payment Application Audit: Guidance for Auditing AIA Documents G702 & G703From EverandThe Contractor Payment Application Audit: Guidance for Auditing AIA Documents G702 & G703No ratings yet

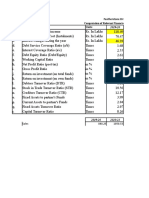

- Financial Statements Analysis On Renata LimitedDocument37 pagesFinancial Statements Analysis On Renata LimitedMd Forhad AliNo ratings yet

- Revenue Recognition for Construction ContractsDocument18 pagesRevenue Recognition for Construction ContractsPrincess SagreNo ratings yet

- Choosing Financial KPIs: Operating Profit per Passenger Predicts Airline SuccessDocument22 pagesChoosing Financial KPIs: Operating Profit per Passenger Predicts Airline Successgharab100% (1)

- Accounting Standard 7 Construction ContractsDocument35 pagesAccounting Standard 7 Construction Contractsvaish2u8862No ratings yet

- Chapter 8 - Notes - Part 2Document7 pagesChapter 8 - Notes - Part 2Xiena100% (1)

- Chapter 4 Revenue Recognition 2Document52 pagesChapter 4 Revenue Recognition 2Brennan DayacapNo ratings yet

- Contract CostingDocument15 pagesContract CostingUjjwal BeriwalNo ratings yet

- Week 10 Revenue Recognition-Long-term Construction Contract - ACTG341 Advanced Financial Accounting and Reporting 1Document12 pagesWeek 10 Revenue Recognition-Long-term Construction Contract - ACTG341 Advanced Financial Accounting and Reporting 1Marilou Arcillas PanisalesNo ratings yet

- Cost Accounting Contract CostingDocument25 pagesCost Accounting Contract CostingBhavika GuptaNo ratings yet

- CIMA F2 Text Supplement Construction PDFDocument18 pagesCIMA F2 Text Supplement Construction PDFSiang MingNo ratings yet

- Revenue Recognition - Construction Accounting MCQsDocument18 pagesRevenue Recognition - Construction Accounting MCQsSharmaineMirandaNo ratings yet

- Construction Contracts: Learning OutcomesDocument29 pagesConstruction Contracts: Learning Outcomessadaf_gul_7100% (1)

- Construction Contracts - Ias 11Document3 pagesConstruction Contracts - Ias 11Shariful HoqueNo ratings yet

- IFRS Construction ContractsDocument18 pagesIFRS Construction ContractsJamba WambulwaNo ratings yet

- Mega Project Assurance: Volume One - The Terminological DictionaryFrom EverandMega Project Assurance: Volume One - The Terminological DictionaryNo ratings yet

- Accounting For Long Term Construction ContractsDocument34 pagesAccounting For Long Term Construction Contracts수지100% (1)

- Accounting Cycle ReviewDocument40 pagesAccounting Cycle ReviewTornike JashiNo ratings yet

- Accounting Standard-7: Construction ContractsDocument23 pagesAccounting Standard-7: Construction Contractsarun666100% (3)

- As 7Document18 pagesAs 7VEDSHREE CHAUDHARINo ratings yet

- 7 - Long-Term Construction ContractsDocument6 pages7 - Long-Term Construction ContractsDarlene Faye Cabral RosalesNo ratings yet

- ACCOUNTING FOR SPECIAL TRANSACTIONS - Construction ContractsDocument29 pagesACCOUNTING FOR SPECIAL TRANSACTIONS - Construction ContractsDewdrop Mae RafananNo ratings yet

- Accounting For Construction Contracts As 7Document6 pagesAccounting For Construction Contracts As 7Ruthvik SharmaNo ratings yet

- Fa - Topic 3 Contract AccountDocument9 pagesFa - Topic 3 Contract AccountERICK ABDINo ratings yet

- IAS 11 Construction ContractsDocument15 pagesIAS 11 Construction ContractsIsrahayda LuNo ratings yet

- IPSAS 11 CIMA - F2 - Text - Supplement - ConstructionDocument18 pagesIPSAS 11 CIMA - F2 - Text - Supplement - ConstructionReview Cpa TNo ratings yet

- CH 08Document29 pagesCH 08Gebremedhin GebruNo ratings yet

- Accounting Seminar - Assignment CH 10 (Doni Rahmad & Fachriza Mizafin)Document5 pagesAccounting Seminar - Assignment CH 10 (Doni Rahmad & Fachriza Mizafin)Kazuyano DoniNo ratings yet

- Construction Contract - EDITED Reporting-ASTDocument70 pagesConstruction Contract - EDITED Reporting-ASTVatchdemonNo ratings yet

- Afar 2 Module CH 7Document12 pagesAfar 2 Module CH 7KezNo ratings yet

- Construction ContractsDocument33 pagesConstruction ContractsJaira Mae AustriaNo ratings yet

- MSU-Gensan Construction Contract AccountingDocument6 pagesMSU-Gensan Construction Contract Accountingtrixie maeNo ratings yet

- Construction ContractsDocument9 pagesConstruction ContractsMahir RahmanNo ratings yet

- Ch10 Construction ContractsDocument21 pagesCh10 Construction ContractsiKarloNo ratings yet

- Contract AccountDocument10 pagesContract AccountAhmad MustaqeemNo ratings yet

- Study Material On CMADocument9 pagesStudy Material On CMAjinendra8421001702No ratings yet

- 5 Long-Term Construction ContractDocument12 pages5 Long-Term Construction ContractMark TaysonNo ratings yet

- 5 Long Term Construction Contract 3e5ca4a29cf252303 Ffcc2ab83e9ecba CompressDocument12 pages5 Long Term Construction Contract 3e5ca4a29cf252303 Ffcc2ab83e9ecba Compressgelly studiesNo ratings yet

- ContrsctDocument23 pagesContrsctMohammed Naeem Mohammed NaeemNo ratings yet

- Ias 11 SummaryDocument6 pagesIas 11 Summarypradyp15No ratings yet

- IAS 11 Construction Contracts Summary With Example p4gDocument4 pagesIAS 11 Construction Contracts Summary With Example p4gvaradu1963No ratings yet

- Notes LTCCDocument2 pagesNotes LTCCMila Casandra CastañedaNo ratings yet

- Edu-Care Professional Academy:, 243, Sundaram Coplex, Bhanwerkuan Main Road, IndoreDocument10 pagesEdu-Care Professional Academy:, 243, Sundaram Coplex, Bhanwerkuan Main Road, IndoreCA Gourav Jashnani100% (1)

- Financial Reporting: IAS 11 - Construction ContractsDocument6 pagesFinancial Reporting: IAS 11 - Construction ContractsazmattullahNo ratings yet

- Chapter 22 Contract Costing - NoRestrictionDocument18 pagesChapter 22 Contract Costing - NoRestrictionMohammad SaadmanNo ratings yet

- Cotract Costing Project TopicDocument17 pagesCotract Costing Project TopicShravani Shrav100% (1)

- JK Shah BookDocument147 pagesJK Shah Bookka28000111222No ratings yet

- 6.1.1. Revenue Recognition - Construction ContractsDocument56 pages6.1.1. Revenue Recognition - Construction ContractsJhaister Ashley LayugNo ratings yet

- Contract Costing of Indian Security Force at BangaloreDocument17 pagesContract Costing of Indian Security Force at BangaloreShravani ShravNo ratings yet

- Lesson 9 Long Term ConstructionDocument13 pagesLesson 9 Long Term ConstructionheyheyNo ratings yet

- Construction ContractDocument7 pagesConstruction ContractnkaluNo ratings yet

- Contract Costing Methods & CalculationsDocument78 pagesContract Costing Methods & CalculationsVandana Sharma100% (1)

- Learn Cost Accounting Concepts for Contract CostingDocument32 pagesLearn Cost Accounting Concepts for Contract CostingPrince Nanaba EphsonNo ratings yet

- Job Costing and Contract Costing ExplainedDocument25 pagesJob Costing and Contract Costing ExplainedParminder Bajaj100% (1)

- Introduction To Accounting For Construction ContractsDocument4 pagesIntroduction To Accounting For Construction ContractsJohn TomNo ratings yet

- Contract Costing: Dr. Sitaram PandeyDocument17 pagesContract Costing: Dr. Sitaram Pandeyravi anandNo ratings yet

- General de Jesus CollegeDocument12 pagesGeneral de Jesus CollegeErwin Labayog MedinaNo ratings yet

- Accounting Standard 7Document5 pagesAccounting Standard 7abinash2830No ratings yet

- Deloitte VertDocument28 pagesDeloitte VertThoaNo ratings yet

- P1Ch1AS7AndASI29 PDFDocument50 pagesP1Ch1AS7AndASI29 PDFSree KanthNo ratings yet

- Revenue Ind AS 115Document54 pagesRevenue Ind AS 115amitguptasidNo ratings yet

- Tristar Bogus Purchases Cross ExamDocument7 pagesTristar Bogus Purchases Cross ExamYashu GoelNo ratings yet

- DVAT Amendment Act 2013 CI of Dated 28Document2 pagesDVAT Amendment Act 2013 CI of Dated 28Yashu GoelNo ratings yet

- Perfect Paradise Unclaimed LiabilitiesDocument8 pagesPerfect Paradise Unclaimed LiabilitiesYashu GoelNo ratings yet

- InstructionsDocument1 pageInstructionsYashu GoelNo ratings yet

- E Gaz 201355220Document4 pagesE Gaz 201355220Yashu GoelNo ratings yet

- DP 1Document13 pagesDP 1Yashu GoelNo ratings yet

- Notification CTTDocument6 pagesNotification CTTYashu GoelNo ratings yet

- Form No 4Document1 pageForm No 4Yashu GoelNo ratings yet

- Notification 40/2013Document1 pageNotification 40/2013Yashu GoelNo ratings yet

- Form No. 2 Notice of Demand: NotesDocument1 pageForm No. 2 Notice of Demand: NotesYashu GoelNo ratings yet

- Form No. 3 Appeal To The Commissioner of Income-Tax (Appeals) Designation of The Commissioner (Appeals)Document1 pageForm No. 3 Appeal To The Commissioner of Income-Tax (Appeals) Designation of The Commissioner (Appeals)Yashu GoelNo ratings yet

- Form 26QBDocument1 pageForm 26QBYashu GoelNo ratings yet

- Appendix Form No. 1 Return of Taxable Commodities TransactionsDocument3 pagesAppendix Form No. 1 Return of Taxable Commodities TransactionsYashu GoelNo ratings yet

- Form 16BDocument1 pageForm 16BYashu GoelNo ratings yet

- Finance Act 2013Document63 pagesFinance Act 2013Yashu GoelNo ratings yet

- 4 Accounting Concepts and ConventionsDocument20 pages4 Accounting Concepts and ConventionsHislord BrakohNo ratings yet

- Chart of Accounts and Journal Entries GuideDocument7 pagesChart of Accounts and Journal Entries GuideKristal Fialho Costa JolyNo ratings yet

- 2015 IKEA Annual Report Shows 18.75% Revenue GrowthDocument1 page2015 IKEA Annual Report Shows 18.75% Revenue GrowthGilang RamadhanNo ratings yet

- Financial Ratio Analysis of HealthsouthDocument11 pagesFinancial Ratio Analysis of Healthsouthfarha tabassumNo ratings yet

- USJR Private University Statement of ActivitiesDocument13 pagesUSJR Private University Statement of ActivitiesSy Him80% (5)

- Printicomm's acquisition of DigitechDocument7 pagesPrinticomm's acquisition of DigitechAK0% (1)

- Accounting Principles Review for Pet Shop BusinessDocument24 pagesAccounting Principles Review for Pet Shop BusinessAlma Dimaranan-Acuña83% (6)

- File 3Document77 pagesFile 3Othow Cham AballaNo ratings yet

- Akm 1Document7 pagesAkm 1Mohammad Alfiyan SyahrilNo ratings yet

- Electrona Corporation Financial Statements 1995-1998Document18 pagesElectrona Corporation Financial Statements 1995-1998Anonymous HVLVK4No ratings yet

- Imran ProfileDocument1 pageImran ProfileImran SaleemNo ratings yet

- Exam 1 AmDocument51 pagesExam 1 AmShanzah SaNo ratings yet

- Public Revenue Sources DefinedDocument11 pagesPublic Revenue Sources DefinedIfaz Mohammed Islam 1921237030No ratings yet

- 1-9 A Fundamental Analysis of Indian Automobile Industry With Special Reference To Tata, Maruti & Mahindra & Mahindra PDFDocument9 pages1-9 A Fundamental Analysis of Indian Automobile Industry With Special Reference To Tata, Maruti & Mahindra & Mahindra PDFMariyam KaziNo ratings yet

- Project Report - MSOPDocument52 pagesProject Report - MSOPAnupriya KalaivananNo ratings yet

- Tax 1 Vthsem Module 1,2, and 3Document97 pagesTax 1 Vthsem Module 1,2, and 3Sahana narayanNo ratings yet

- Wipro's Financial Performance Comparison 2009-2010Document46 pagesWipro's Financial Performance Comparison 2009-2010Abhishek KhareNo ratings yet

- Project Report On Aditya 1Document75 pagesProject Report On Aditya 1SanchitNo ratings yet

- Featherstone Dry Mix Pvt. Ltd. Serial Particulars Units: Sales 848.25 1050.53Document39 pagesFeatherstone Dry Mix Pvt. Ltd. Serial Particulars Units: Sales 848.25 1050.53saubhik goswamiNo ratings yet

- BSA-4A - Group-10 - ASSIGNMENT - 10-05-21 PRE-FINALDocument40 pagesBSA-4A - Group-10 - ASSIGNMENT - 10-05-21 PRE-FINALVeralou UrbinoNo ratings yet

- Record KeepingDocument11 pagesRecord Keepingr.jeyashankar9550No ratings yet

- Ratio Analysis Notes (Theory)Document3 pagesRatio Analysis Notes (Theory)Karishma KatiyarNo ratings yet

- Abm 3 Exam ReviewerDocument7 pagesAbm 3 Exam Reviewerjoshua korylle mahinayNo ratings yet

- Fin 3Document5 pagesFin 3Mary DenizeNo ratings yet

- Insurance Claims For Loss of Stock and Loss of Profit 2 PDFDocument22 pagesInsurance Claims For Loss of Stock and Loss of Profit 2 PDFEswari Gk100% (1)