You might also like

- 50 Reasons Why North East Business Is GreatDocument1 page50 Reasons Why North East Business Is GreatWales_OnlineNo ratings yet

- Williams Commission: The Report of The Commission On Public Service Governance and Delivery in WalesDocument105 pagesWilliams Commission: The Report of The Commission On Public Service Governance and Delivery in WalesWales_OnlineNo ratings yet

- Wales Top 300 2013Document5 pagesWales Top 300 2013Wales_Online100% (1)

- Stage 5 Tour of BritainDocument4 pagesStage 5 Tour of BritainWales_OnlineNo ratings yet

- Part 1 of The Jillings Report Into Child Abuse in North WalesDocument175 pagesPart 1 of The Jillings Report Into Child Abuse in North WalesWales_OnlineNo ratings yet

- Empowerment and Responsibility: Devolving Financial Powers To WalesDocument30 pagesEmpowerment and Responsibility: Devolving Financial Powers To WalesWales_OnlineNo ratings yet

- Susanne Llewellyn-Jones002 PDFDocument1 pageSusanne Llewellyn-Jones002 PDFWales_OnlineNo ratings yet

- Susanne Llewellyn-Jones Coverage in The South Wales Echo, 18 August 1980Document1 pageSusanne Llewellyn-Jones Coverage in The South Wales Echo, 18 August 1980Wales_OnlineNo ratings yet

- Susanne Llewellyn-Jones Coverage in The South Wales EchoDocument1 pageSusanne Llewellyn-Jones Coverage in The South Wales EchoWales_OnlineNo ratings yet

- Susanne Llewellyn-Jones Coverage in The South Wales Echo, 15 June 1990Document1 pageSusanne Llewellyn-Jones Coverage in The South Wales Echo, 15 June 1990Wales_OnlineNo ratings yet

- Part 2 of The Jillings Report Into Child Abuse in North WalesDocument143 pagesPart 2 of The Jillings Report Into Child Abuse in North WalesWales_OnlineNo ratings yet

- Stage 4 Tour of BritainDocument4 pagesStage 4 Tour of BritainWales_OnlineNo ratings yet

- Top300 GraphicDocument1 pageTop300 GraphicWales_OnlineNo ratings yet

- Top300 241Document1 pageTop300 241Wales_OnlineNo ratings yet

- 2013 02 13 FINAL Silk Evidence PDF - EnglishDocument31 pages2013 02 13 FINAL Silk Evidence PDF - EnglishWales_Online0% (1)

- Fly Tipping 6Document1 pageFly Tipping 6Wales_OnlineNo ratings yet

- CNN 130111 Yewtree Report PDF Wdf93652Document39 pagesCNN 130111 Yewtree Report PDF Wdf93652Censored News NowNo ratings yet

- Top300 121Document1 pageTop300 121Wales_OnlineNo ratings yet

- Football Agent Fees 2011Document7 pagesFootball Agent Fees 2011Wales_OnlineNo ratings yet

- Top300 1Document1 pageTop300 1Wales_OnlineNo ratings yet

- Improving Schools - Executive SummaryDocument12 pagesImproving Schools - Executive SummaryWales_OnlineNo ratings yet

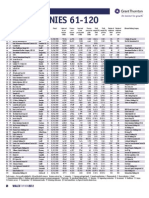

- Top300 61Document1 pageTop300 61Wales_OnlineNo ratings yet

- Pembrokeshire County Council: Independent Review Pupil Referral UnitDocument29 pagesPembrokeshire County Council: Independent Review Pupil Referral UnitWales_OnlineNo ratings yet

- Flytipping WalesDocument8 pagesFlytipping WalesWales_OnlineNo ratings yet

- Young Drivers BookletDocument8 pagesYoung Drivers BookletWales_OnlineNo ratings yet

- Fly Tipping 5Document3 pagesFly Tipping 5Wales_OnlineNo ratings yet

- Ministerial Letter On Councillors' RemunerationDocument2 pagesMinisterial Letter On Councillors' RemunerationWales_OnlineNo ratings yet

- Fly Tipping 4Document1 pageFly Tipping 4Wales_OnlineNo ratings yet

- Fly Tipping 3Document1 pageFly Tipping 3Wales_OnlineNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Electrical Energy Audit and SafetyDocument13 pagesElectrical Energy Audit and SafetyRam Kapur100% (1)

- Evolution of Local Bodies in IndiaDocument54 pagesEvolution of Local Bodies in Indiaanashwara.pillaiNo ratings yet

- Simple Present: Positive SentencesDocument16 pagesSimple Present: Positive SentencesPablo Chávez LópezNo ratings yet

- Straight and Crooked ThinkingDocument208 pagesStraight and Crooked Thinkingmekhanic0% (1)

- 8D6N Europe WonderDocument2 pages8D6N Europe WonderEthan ExpressivoNo ratings yet

- Kanter v. BarrDocument64 pagesKanter v. BarrTodd Feurer100% (1)

- What Does The Bible Say About Hell?Document12 pagesWhat Does The Bible Say About Hell?revjackhowell100% (2)

- Rabindranath Tagore's Portrayal of Aesthetic and Radical WomanDocument21 pagesRabindranath Tagore's Portrayal of Aesthetic and Radical WomanShilpa DwivediNo ratings yet

- United States Court of Appeals, Tenth CircuitDocument5 pagesUnited States Court of Appeals, Tenth CircuitScribd Government DocsNo ratings yet

- Transformation of The Goddess Tara With PDFDocument16 pagesTransformation of The Goddess Tara With PDFJim Weaver100% (1)

- English JAMB Questions and Answers 2023Document5 pagesEnglish JAMB Questions and Answers 2023Samuel BlessNo ratings yet

- Wires and Cables: Dobaindustrial@ethionet - EtDocument2 pagesWires and Cables: Dobaindustrial@ethionet - EtCE CERTIFICATENo ratings yet

- Unit 2 Management of EthicsDocument19 pagesUnit 2 Management of Ethics088jay Isamaliya0% (1)

- Introduction To Asset Pricing ModelDocument8 pagesIntroduction To Asset Pricing ModelHannah NazirNo ratings yet

- CHAPTER-1 FeasibilityDocument6 pagesCHAPTER-1 FeasibilityGlads De ChavezNo ratings yet

- QC 006 Sejarah SenibinaDocument22 pagesQC 006 Sejarah SenibinaRamsraj0% (1)

- Green CHMDocument11 pagesGreen CHMShj OunNo ratings yet

- Essential Rabbi Nachman meditation and personal prayerDocument9 pagesEssential Rabbi Nachman meditation and personal prayerrm_pi5282No ratings yet

- Pakistan Money MarketDocument2 pagesPakistan Money MarketOvais AdenwallaNo ratings yet

- A History of Oracle Cards in Relation To The Burning Serpent OracleDocument21 pagesA History of Oracle Cards in Relation To The Burning Serpent OracleGiancarloKindSchmidNo ratings yet

- ICS ModulesDocument67 pagesICS ModulesJuan RiveraNo ratings yet

- Taiping's History as Malaysia's "City of Everlasting PeaceDocument6 pagesTaiping's History as Malaysia's "City of Everlasting PeaceIzeliwani Haji IsmailNo ratings yet

- Illustrative Bank Branch Audit FormatDocument4 pagesIllustrative Bank Branch Audit Formatnil sheNo ratings yet

- Volume 42, Issue 52 - December 30, 2011Document44 pagesVolume 42, Issue 52 - December 30, 2011BladeNo ratings yet

- Comprehensive Disaster Management Programme (CDMP II) 2013 Year-End ReviewDocument18 pagesComprehensive Disaster Management Programme (CDMP II) 2013 Year-End ReviewCDMP BangladeshNo ratings yet

- Theresa Abbott's Story of Corruption and Abuse by Those Meant to Protect HerDocument35 pagesTheresa Abbott's Story of Corruption and Abuse by Those Meant to Protect HerJoyce EileenNo ratings yet

- Module 6 ObliCon Form Reformation and Interpretation of ContractsDocument6 pagesModule 6 ObliCon Form Reformation and Interpretation of ContractsAngelica BesinioNo ratings yet

- Ancient To Roman EducationDocument5 pagesAncient To Roman EducationJonie Abilar100% (1)

- AC4301 FinalExam 2020-21 SemA AnsDocument9 pagesAC4301 FinalExam 2020-21 SemA AnslawlokyiNo ratings yet

- Jffii - Google SearchDocument2 pagesJffii - Google SearchHAMMAD SHAHNo ratings yet