You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Title: Business Plan For The Establishment of A Micro-Brewery (Craft Beer) in Freetown Sierra LeoneDocument41 pagesTitle: Business Plan For The Establishment of A Micro-Brewery (Craft Beer) in Freetown Sierra LeoneKishin Sham MahtaniNo ratings yet

- Title: Business Plan For The Establishment of A Micro-Brewery (Craft Beer) in Freetown Sierra LeoneDocument41 pagesTitle: Business Plan For The Establishment of A Micro-Brewery (Craft Beer) in Freetown Sierra LeoneKishin Sham MahtaniNo ratings yet

- Research Proposal PresentationDocument12 pagesResearch Proposal PresentationjahkuttaNo ratings yet

- Research in The Business EnvironmentDocument21 pagesResearch in The Business EnvironmentKishin Sham MahtaniNo ratings yet

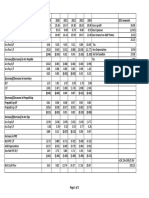

- Company Valuation FHCDocument1 pageCompany Valuation FHCKishin Sham MahtaniNo ratings yet

- New Enterprise Creation U1Document73 pagesNew Enterprise Creation U1Kishin Sham MahtaniNo ratings yet

- Company Valuation FHC2Document2 pagesCompany Valuation FHC2Kishin Sham MahtaniNo ratings yet

- Corporate Finance - Kishin Sham MahtaniDocument9 pagesCorporate Finance - Kishin Sham MahtaniKishin Sham MahtaniNo ratings yet

- Final Assignment International BusinessDocument19 pagesFinal Assignment International BusinessKishin Sham MahtaniNo ratings yet

- Rania - S Coffee Morning 5.3.2014Document1 pageRania - S Coffee Morning 5.3.2014Kishin Sham MahtaniNo ratings yet

- 4CSK1 041110003 Tma3Document5 pages4CSK1 041110003 Tma3Kishin Sham MahtaniNo ratings yet

- Driving Directions To Grand Kampar HotelDocument2 pagesDriving Directions To Grand Kampar HotelKishin Sham MahtaniNo ratings yet

- 4CSK1 041100356 Tma1Document8 pages4CSK1 041100356 Tma1Kishin Sham MahtaniNo ratings yet

- Chap02 - Using IT For Competitive AdvantageDocument32 pagesChap02 - Using IT For Competitive AdvantageAzizah SyarifNo ratings yet

- BBM 205 Study ScheduleDocument2 pagesBBM 205 Study ScheduleKishin Sham MahtaniNo ratings yet

- Microsoft Word - BBM104 July 2011 TMA2Document4 pagesMicrosoft Word - BBM104 July 2011 TMA2Kishin Sham MahtaniNo ratings yet

- Microeconomics TMA analyzes market equilibriumDocument33 pagesMicroeconomics TMA analyzes market equilibriumKishin Sham MahtaniNo ratings yet

- BBM102 Tma2Document7 pagesBBM102 Tma2Kishin Sham MahtaniNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Comparison of loan and deposit schemes of Indian Overseas Bank and Development Credit Bank of IndiaDocument13 pagesComparison of loan and deposit schemes of Indian Overseas Bank and Development Credit Bank of IndiaKaran GujralNo ratings yet

- 4-CONSUMER CREDIT (PART 1) (Introduction To Consumer Credit)Document31 pages4-CONSUMER CREDIT (PART 1) (Introduction To Consumer Credit)Nur DinieNo ratings yet

- Departamento Del Tesoro de Estados Unidos: Notificación de Hallazgo Sobre La Banca Privada de Andora Es Una Institución Financiera de Preocupación de Lavado de Dinero.Document10 pagesDepartamento Del Tesoro de Estados Unidos: Notificación de Hallazgo Sobre La Banca Privada de Andora Es Una Institución Financiera de Preocupación de Lavado de Dinero.ProdavinciNo ratings yet

- Social ResponsibilityDocument10 pagesSocial ResponsibilityMark Ed MontoyaNo ratings yet

- Zain - Management TeamDocument2 pagesZain - Management TeamalbidaiaNo ratings yet

- 1 - GREPA v. CA G.R. No. 113899 October 13, 1999Document2 pages1 - GREPA v. CA G.R. No. 113899 October 13, 1999Emrico CabahugNo ratings yet

- Foreign Exchange Rate and PoliciesDocument24 pagesForeign Exchange Rate and PoliciesbharatNo ratings yet

- Banking For Muggles 101Document6 pagesBanking For Muggles 101Kurt KlingbeilNo ratings yet

- IBPS Clerk Main 2016 Capsule by AffairscloudDocument91 pagesIBPS Clerk Main 2016 Capsule by AffairscloudMadhu SekharNo ratings yet

- Atm Using FingerprintDocument5 pagesAtm Using FingerprintShivaNo ratings yet

- L Williams trial balance transactionsDocument3 pagesL Williams trial balance transactionsKaung SattNo ratings yet

- MHA Bank Challan Fee Deposit InstructionsDocument1 pageMHA Bank Challan Fee Deposit Instructionsmanish shekharNo ratings yet

- Evidence 6 7Document3 pagesEvidence 6 7Jennifer JohnsonNo ratings yet

- Cab Report Mid SipDocument74 pagesCab Report Mid SipSawarmal ChoudharyNo ratings yet

- Holiday Home Booking 10 Oct 2016Document2 pagesHoliday Home Booking 10 Oct 2016NityapriyaSrivastavaNo ratings yet

- The Bank of KhyberDocument15 pagesThe Bank of KhyberNaila Mehboob100% (2)

- Intro & SwotDocument26 pagesIntro & SwotPuneet Singh DhaniNo ratings yet

- Standard Bank online banking payment confirmationDocument1 pageStandard Bank online banking payment confirmationEmmanuel EgbebuNo ratings yet

- Engro Fertilizers Profile 2018Document148 pagesEngro Fertilizers Profile 2018Asif AliNo ratings yet

- Cardiff Cash Management V2.0Document108 pagesCardiff Cash Management V2.0elsa7er2000No ratings yet

- Corporation Bank ProjectDocument65 pagesCorporation Bank ProjectAjay MasseyNo ratings yet

- Lordofwar Ocr Part3Document721 pagesLordofwar Ocr Part3Ky HendersonNo ratings yet

- QuestionnaireDocument5 pagesQuestionnaireharpalchudasama1100% (10)

- Akhuwat Foundation Services BreakdownDocument30 pagesAkhuwat Foundation Services BreakdownAdeel KhanNo ratings yet

- Chapter 7Document61 pagesChapter 7souravkiller4uNo ratings yet

- Lecture 2Document31 pagesLecture 2Daanyal Ibn UmarNo ratings yet

- Yu Lim Vs YuDocument6 pagesYu Lim Vs YusandrasulitNo ratings yet

- SBI initiates coverage with performer ratingDocument20 pagesSBI initiates coverage with performer ratingPraharsh SinghNo ratings yet

- Confirmation Page PDFDocument1 pageConfirmation Page PDFsaralabitmNo ratings yet

- Tianjin PlasticsDocument9 pagesTianjin PlasticsmalikatjuhNo ratings yet