You might also like

- MGT411-Latest Solved MCQS by MeDocument62 pagesMGT411-Latest Solved MCQS by MeWaqas SherwaniNo ratings yet

- Asset Backed SecuritiesDocument179 pagesAsset Backed SecuritiesShivani NidhiNo ratings yet

- Treasury Management AssignmentDocument28 pagesTreasury Management AssignmentThanh LexNo ratings yet

- Needham Bit Coin ReportDocument31 pagesNeedham Bit Coin ReportAlex100% (1)

- 2015-11-02 PDF JP Morgan Special Report - Proposed FRTB Ruling Endangers Securitized Products MarketsDocument10 pages2015-11-02 PDF JP Morgan Special Report - Proposed FRTB Ruling Endangers Securitized Products MarketsDivya Krishna BirthrayNo ratings yet

- 4 6032630305691534636 PDFDocument254 pages4 6032630305691534636 PDFDennisNo ratings yet

- Foreign Exchange Risk ManagementDocument12 pagesForeign Exchange Risk ManagementDinesh KumarNo ratings yet

- ANZ Chattel MortgageDocument10 pagesANZ Chattel Mortgagelovekimsohyun89No ratings yet

- Government Influence On Exchange Rate in BangladeshDocument22 pagesGovernment Influence On Exchange Rate in BangladeshOmar50% (2)

- Financial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksDocument5 pagesFinancial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksAnamMalikNo ratings yet

- Accenture Banking Retail LendingDocument16 pagesAccenture Banking Retail LendingRaunak MotwaniNo ratings yet

- Economic Order Quantity ModelsDocument7 pagesEconomic Order Quantity ModelsP Singh KarkiNo ratings yet

- Leman BrothersDocument7 pagesLeman Brothersblueeagle477952No ratings yet

- What Is Financial RiskDocument9 pagesWhat Is Financial RiskDeboit BhattacharjeeNo ratings yet

- Chapter 11 - Computation of Taxable Income and TaxDocument22 pagesChapter 11 - Computation of Taxable Income and TaxMichelle Tan100% (1)

- MF0007 Treasury Management MQPDocument11 pagesMF0007 Treasury Management MQPNikhil Rana0% (1)

- NettingDocument17 pagesNettingAnshulGupta100% (1)

- Microproject On Hotel Management SystemDocument13 pagesMicroproject On Hotel Management SystemYuvraj DeshmukhNo ratings yet

- Financial Management QuestionsDocument3 pagesFinancial Management Questionsjagdish002No ratings yet

- Evolution and Function of MoneyDocument14 pagesEvolution and Function of MoneyGhulam HasnainNo ratings yet

- Securities and MarketsDocument51 pagesSecurities and MarketsBilal JavedNo ratings yet

- Concepts of Value and ReturnDocument38 pagesConcepts of Value and ReturnVaishnav KumarNo ratings yet

- Treasury Management AssignmentDocument4 pagesTreasury Management AssignmentJed Bentillo100% (1)

- The Development of Asset Securitisation in MalaysiaDocument14 pagesThe Development of Asset Securitisation in MalaysiaAK FleurNo ratings yet

- SEBI Role and FunctionsDocument28 pagesSEBI Role and FunctionsAnurag Singh100% (4)

- C.A IPCC Ratio AnalysisDocument6 pagesC.A IPCC Ratio AnalysisAkash Gupta100% (2)

- Primary Role of Company AuditorDocument5 pagesPrimary Role of Company AuditorAshutosh GoelNo ratings yet

- Investment BankingDocument15 pagesInvestment BankingRahul singhNo ratings yet

- Chapter 06Document25 pagesChapter 06Farjana Hossain DharaNo ratings yet

- Capital MarketDocument15 pagesCapital Marketरजनीश कुमारNo ratings yet

- Financial Markets and Resource MobilizationDocument13 pagesFinancial Markets and Resource MobilizationFred Raphael Ilomo100% (3)

- Money Mkt.Document9 pagesMoney Mkt.Kajal ChaudharyNo ratings yet

- Financial Markets and Institutionschap 2Document8 pagesFinancial Markets and Institutionschap 2Ini IchiiiNo ratings yet

- Introduction To Financial MarketDocument30 pagesIntroduction To Financial Marketmaria evangelistaNo ratings yet

- Money and Banking: Chapter - 8Document36 pagesMoney and Banking: Chapter - 8Nihar NanyamNo ratings yet

- International Financial MarketDocument36 pagesInternational Financial MarketSmitaNo ratings yet

- Alibaba ProductsDocument4 pagesAlibaba ProductsYash SurekaNo ratings yet

- Understanding Multiple Deposit Creation and The Money SupplyDocument36 pagesUnderstanding Multiple Deposit Creation and The Money SupplyJames EstradaNo ratings yet

- Chapter 11 The Money MarketsDocument8 pagesChapter 11 The Money Marketslasha KachkachishviliNo ratings yet

- Financial Management Tutorial QuestionsDocument8 pagesFinancial Management Tutorial QuestionsStephen Olieka100% (2)

- Banking Quiz on Assets, Liabilities, Basel Accords & MoreDocument5 pagesBanking Quiz on Assets, Liabilities, Basel Accords & Morenatasha100% (1)

- ICWAI Dividend Policy-Financial Management & International Finance Study Material DownloadDocument35 pagesICWAI Dividend Policy-Financial Management & International Finance Study Material DownloadsuccessgurusNo ratings yet

- Financial Management Assignment 1Document12 pagesFinancial Management Assignment 1parvathy ShanmughanNo ratings yet

- Chap 006Document14 pagesChap 006Adi SusiloNo ratings yet

- Solutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 8Document4 pagesSolutions To Problems: Smart/Gitman/Joehnk, Fundamentals of Investing, 12/e Chapter 8Ahmed El KhateebNo ratings yet

- New Edited Cash ManagementDocument59 pagesNew Edited Cash Managementdominic wurdaNo ratings yet

- Analyzing Developing Country Debt Using the Basic Transfer MechanismDocument5 pagesAnalyzing Developing Country Debt Using the Basic Transfer MechanismJade Marie FerrolinoNo ratings yet

- Settlement SystemsDocument6 pagesSettlement SystemsRachana PatilNo ratings yet

- BTR Functions Draft 6-1-15Document16 pagesBTR Functions Draft 6-1-15Hanna PentiñoNo ratings yet

- Chapter 6 Review QuestionsDocument3 pagesChapter 6 Review Questionsapi-242667057100% (1)

- Factoring & ForfaitingDocument2 pagesFactoring & ForfaitingYashNo ratings yet

- FIN 413 - Midterm #2 SolutionsDocument6 pagesFIN 413 - Midterm #2 SolutionsWesley CheungNo ratings yet

- Raising Capital: A Survey of Non-Bank Sources of CapitalDocument34 pagesRaising Capital: A Survey of Non-Bank Sources of CapitalRoy Joshua100% (1)

- 1 Financial MarketDocument35 pages1 Financial MarketSachinGoelNo ratings yet

- Core Risks in BankingDocument9 pagesCore Risks in BankingVenkatsubramanian R IyerNo ratings yet

- Sources of international financing and analysisDocument6 pagesSources of international financing and analysisSabha Pathy100% (2)

- FIN204 AnswersDocument9 pagesFIN204 Answerssiddhant jainNo ratings yet

- Leon County Sheriff'S Office Daily Booking Report 4-Jan-2022 Page 1 of 3Document3 pagesLeon County Sheriff'S Office Daily Booking Report 4-Jan-2022 Page 1 of 3WCTV Digital TeamNo ratings yet

- Presidential Commission On Good Government v. GutierrezDocument12 pagesPresidential Commission On Good Government v. GutierrezJanine OlivaNo ratings yet

- TOR Custom Clearance in Ethiopia SCIDocument12 pagesTOR Custom Clearance in Ethiopia SCIDaniel GemechuNo ratings yet

- ISPS Code Awareness TrainingDocument57 pagesISPS Code Awareness Trainingdiegocely700615100% (1)

- Twelve Reasons To Understand 1 Corinthians 7:21-23 As A Call To Gain Freedom Philip B. Payne © 2009Document10 pagesTwelve Reasons To Understand 1 Corinthians 7:21-23 As A Call To Gain Freedom Philip B. Payne © 2009NinthCircleOfHellNo ratings yet

- ST TuesDocument34 pagesST Tuesdoug smitherNo ratings yet

- Assigned Cases SpreadsheetDocument13 pagesAssigned Cases SpreadsheetJulius David UbaldeNo ratings yet

- 2019 Fusion For Energy Financial RegulationDocument60 pages2019 Fusion For Energy Financial Regulationale tof4eNo ratings yet

- Riverscape Fact SheetDocument5 pagesRiverscape Fact SheetSharmaine FalcisNo ratings yet

- The People in The Trees: Also by Hanya YanagiharaDocument5 pagesThe People in The Trees: Also by Hanya YanagiharaMirNo ratings yet

- Bill of Supply For Electricity: Tariff Category:Domestic (Residential)Document2 pagesBill of Supply For Electricity: Tariff Category:Domestic (Residential)Praveen OjhaNo ratings yet

- Kings and ChroniclesDocument18 pagesKings and ChroniclesRamita Udayashankar83% (6)

- Ethics of UtilitarianismDocument26 pagesEthics of UtilitarianismAngelene MangubatNo ratings yet

- Analysis of Freedom of Trade and Commerce in India Under The Indian ConstitutionDocument19 pagesAnalysis of Freedom of Trade and Commerce in India Under The Indian ConstitutionHari DuttNo ratings yet

- Court of Appeals Upholds Dismissal of Forcible Entry CaseDocument6 pagesCourt of Appeals Upholds Dismissal of Forcible Entry CaseJoseph Dimalanta DajayNo ratings yet

- Metro Manila Development Authority v. Viron Transportation Co., Inc., G.R. No. 170656Document2 pagesMetro Manila Development Authority v. Viron Transportation Co., Inc., G.R. No. 170656catrina lobatonNo ratings yet

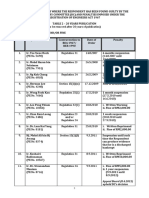

- LIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDocument1 pageLIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDarrenNo ratings yet

- Safety Residential WarrantyDocument1 pageSafety Residential WarrantyJanan AhmadNo ratings yet

- Doe V Doe Trevi LawsuitDocument30 pagesDoe V Doe Trevi LawsuitSaintNo ratings yet

- 17Mb221 Industrial Relations and Labour LawsDocument2 pages17Mb221 Industrial Relations and Labour LawsshubhamNo ratings yet

- Meredith WhitneyDocument13 pagesMeredith WhitneyFortuneNo ratings yet

- Sing To The Dawn 2Document4 pagesSing To The Dawn 2Nur Nabilah80% (5)

- (RBI) OdtDocument2 pages(RBI) OdtSheethal HGNo ratings yet

- Role of Jamaat Islami in Shaping Pakistan PoliticsDocument15 pagesRole of Jamaat Islami in Shaping Pakistan PoliticsEmranRanjhaNo ratings yet

- NC LiabilitiesDocument12 pagesNC LiabilitiesErin LumogdangNo ratings yet

- SAP ACH ConfigurationDocument49 pagesSAP ACH ConfigurationMohammadGhouse100% (4)

- Ownership Dispute Over Corporation's RecordsDocument2 pagesOwnership Dispute Over Corporation's RecordsFrancisco Ashley AcedilloNo ratings yet

- MOA Establishes 50-Hectare Model Agroforestry FarmDocument8 pagesMOA Establishes 50-Hectare Model Agroforestry FarmENRO NRRGNo ratings yet

- Written ComplianceDocument2 pagesWritten ComplianceKriselle Joy ManaloNo ratings yet

- People VS Hon. Bienvenido TanDocument3 pagesPeople VS Hon. Bienvenido Tanjoy dayagNo ratings yet