You might also like

- Equifax FACT RPT 01152013Document21 pagesEquifax FACT RPT 01152013NextSecOfficial100% (2)

- Equifax Personal Solutions - Credit Reports PDFDocument11 pagesEquifax Personal Solutions - Credit Reports PDFTara Stewart80% (5)

- Equifax - FACT - RPT - 12302012 (2013 - 03 - 19 00 - 04 - 23 UTC)Document20 pagesEquifax - FACT - RPT - 12302012 (2013 - 03 - 19 00 - 04 - 23 UTC)Derrick Trueblood Tolliver100% (1)

- Credit Report - No Password PDFDocument5 pagesCredit Report - No Password PDFMohammed Abdul HoqueNo ratings yet

- Michelle Morrison - TransUnion Personal Credit ReportDocument23 pagesMichelle Morrison - TransUnion Personal Credit ReportchfthegodNo ratings yet

- PayStubDocument1 pagePayStubhaideegracebordadorNo ratings yet

- Patsy Hicks - TransUnion Personal Credit ReportDocument18 pagesPatsy Hicks - TransUnion Personal Credit ReportchfthegodNo ratings yet

- TransUnion Credit ReportDocument11 pagesTransUnion Credit ReportEdmond SevilleNo ratings yet

- Credit Report Summary for Regina L. DeFazioDocument9 pagesCredit Report Summary for Regina L. DeFaziolriege88No ratings yet

- Non-Negotiable: Nvidia CorporationDocument1 pageNon-Negotiable: Nvidia CorporationSteven LinNo ratings yet

- Transunion NewDocument8 pagesTransunion NewCaleb HolleyNo ratings yet

- Peter Hart - TransUnion Personal Credit Report - 20200721 PDFDocument12 pagesPeter Hart - TransUnion Personal Credit Report - 20200721 PDFSusu0% (1)

- Report Details Personal and Financial Information for Christopher StegerDocument28 pagesReport Details Personal and Financial Information for Christopher StegerChristopher StegerNo ratings yet

- Christopher Mulligan - TransUnion Personal Credit Report - 20140123Document8 pagesChristopher Mulligan - TransUnion Personal Credit Report - 20140123Richard MulliganNo ratings yet

- United States Bankruptcy Court Voluntary Petition: Central District of CaliforniaDocument65 pagesUnited States Bankruptcy Court Voluntary Petition: Central District of California11CV00233No ratings yet

- Creditreport 1561319714905 PDFDocument38 pagesCreditreport 1561319714905 PDFMustaffa ShabazzNo ratings yet

- Printable ReportDocument74 pagesPrintable Reportkarriem_johnsonNo ratings yet

- Northside Independent School District Pay AdviceDocument2 pagesNorthside Independent School District Pay AdviceJuan EnriqueNo ratings yet

- Wounded WearDocument3 pagesWounded Wearjrotc240007100% (1)

- James Scott Credit ReportDocument26 pagesJames Scott Credit Reportjamess07100% (1)

- Experian Credit Report: 0 Late AccountsDocument18 pagesExperian Credit Report: 0 Late Accountsmary hunterNo ratings yet

- Business Organizations Inquiry - Gamboa Electric IncorporatedDocument1 pageBusiness Organizations Inquiry - Gamboa Electric IncorporatedJaime AbeytiaNo ratings yet

- W2 2010Document2 pagesW2 2010Rick Nunns100% (2)

- SC Tax ReturnDocument12 pagesSC Tax ReturnCeleste KatzNo ratings yet

- Free Email Addresses - Web Based and Secure EmailDocument1 pageFree Email Addresses - Web Based and Secure Emailjessica messicaNo ratings yet

- US Tax ReturnDocument37 pagesUS Tax ReturnMySPNN100% (2)

- Creditreport 1552490650914Document24 pagesCreditreport 1552490650914Angel G Colon MoralesNo ratings yet

- Mercury Drug Citi Card: Minimum Amount Due : 34,859.75 Overlimit AmountDocument4 pagesMercury Drug Citi Card: Minimum Amount Due : 34,859.75 Overlimit AmountSchatz Rah JechaNo ratings yet

- Important ID and NumbersDocument2 pagesImportant ID and Numbersbluestar518No ratings yet

- Fasfa DocsDocument10 pagesFasfa DocsKira Rivera100% (1)

- Img 20140203 0001Document5 pagesImg 20140203 0001Brandon MooreNo ratings yet

- Usaa Federal Savings Bank: Account Number 1 0 3 4 - 0 9 7 6 - 7 Statement Date 1 0 0 2 / 0 9 / 0 9Document6 pagesUsaa Federal Savings Bank: Account Number 1 0 3 4 - 0 9 7 6 - 7 Statement Date 1 0 0 2 / 0 9 / 0 9Big CountryNo ratings yet

- Sara Barz - TransUnion Personal Credit Report - 20141116 PDFDocument14 pagesSara Barz - TransUnion Personal Credit Report - 20141116 PDFSaraBarz50% (2)

- Report Created On: 08/02/2020 With SSN, DOB, Addresses, Phone NumbersDocument4 pagesReport Created On: 08/02/2020 With SSN, DOB, Addresses, Phone NumbersBruce WaynneNo ratings yet

- 15 1 03 003887Document1 page15 1 03 003887Aryan ChaudharyNo ratings yet

- Transaction Details for Corporate Card July 2008-February 2010/TITLEDocument20 pagesTransaction Details for Corporate Card July 2008-February 2010/TITLEKheldz Picache100% (2)

- 20 TR 08894502584200889450Document2 pages20 TR 08894502584200889450Josh JasperNo ratings yet

- Report PDFDocument2 pagesReport PDFJBStringerNo ratings yet

- AMEX - Application FormDocument1 pageAMEX - Application FormdharsinimayaNo ratings yet

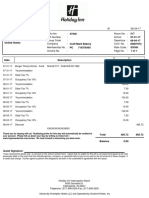

- Hotel invoice for Arshia AliDocument1 pageHotel invoice for Arshia AliIrshad AliNo ratings yet

- Michael D Nieves - TransUnion Personal Credit Report - 20140730Document5 pagesMichael D Nieves - TransUnion Personal Credit Report - 20140730chfthegodNo ratings yet

- Gary Steger D G2 GRVI-506 19th Avenue - 506 19th Avenue Grubstake Properties VI San Mateo, CA 94401Document6 pagesGary Steger D G2 GRVI-506 19th Avenue - 506 19th Avenue Grubstake Properties VI San Mateo, CA 94401Gary SNo ratings yet

- The Texas A&M University System: Statement of Earnings For: Jadhav, Sangramsinh PDocument1 pageThe Texas A&M University System: Statement of Earnings For: Jadhav, Sangramsinh PSangram JadhavNo ratings yet

- Please Sign PPP Origination Application - PDF BDocument12 pagesPlease Sign PPP Origination Application - PDF BpayneNo ratings yet

- DDDDDocument21 pagesDDDDRed Rapture67% (3)

- WAHPBC PayStub Lawanda GardinerDocument1 pageWAHPBC PayStub Lawanda GardinerwahpbcNo ratings yet

- Pay Stub 6.1to6.30Document1 pagePay Stub 6.1to6.30Lorin WagnerNo ratings yet

- Credit ReportDocument10 pagesCredit ReportAubree GatesNo ratings yet

- SBA PPP Loan Calculator - CARES ActDocument2 pagesSBA PPP Loan Calculator - CARES ActJay Mike100% (2)

- AccountExtract PDFDocument3 pagesAccountExtract PDFD Ann HoppieNo ratings yet

- Mark Strauss - TransUnion Personal Credit Report - 20170709Document18 pagesMark Strauss - TransUnion Personal Credit Report - 20170709Anonymous XmPLtmTvfGNo ratings yet

- 21 Il 00126975270200012690Document2 pages21 Il 00126975270200012690harryNo ratings yet

- Electronic Filing Instructions For Your 2016 Michigan Tax ReturnDocument4 pagesElectronic Filing Instructions For Your 2016 Michigan Tax Returngrace kruegerNo ratings yet

- CertainGovernmentPayments1099G JamesSmith-654202001310815Document4 pagesCertainGovernmentPayments1099G JamesSmith-654202001310815ireaditallNo ratings yet

- Drivers License UV Markings Per StateDocument2 pagesDrivers License UV Markings Per StateSome OneNo ratings yet

- CreditReport 1Document17 pagesCreditReport 1Janest TongNo ratings yet

- Methods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeFrom EverandMethods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeNo ratings yet

- Loan Denial Letter BreakdownDocument3 pagesLoan Denial Letter BreakdownJason MoberlyNo ratings yet

- RAKFUNDING BASE PROSPECTUSDocument272 pagesRAKFUNDING BASE PROSPECTUSeliforuNo ratings yet

- Extreme Privacy: Personal Data Removal Workbook & Credit Freeze GuideDocument36 pagesExtreme Privacy: Personal Data Removal Workbook & Credit Freeze Guideblacksun_moon100% (2)

- Final+Bios Sudha WRK OnDocument16 pagesFinal+Bios Sudha WRK OnJigisha VasaNo ratings yet

- Credit - What Is It, & Why Is It Important?: There Are Four Basic Types of Consumer CreditDocument4 pagesCredit - What Is It, & Why Is It Important?: There Are Four Basic Types of Consumer CreditCarolNo ratings yet

- Pfin5 5th Edition Billingsley Solutions ManualDocument22 pagesPfin5 5th Edition Billingsley Solutions Manualthoabangt69100% (29)

- Credit RepairDocument2 pagesCredit RepairMoriel Mohammad El0% (2)

- KT CPC Financial Sector Development Strategy 2016 2025 EnglishDocument133 pagesKT CPC Financial Sector Development Strategy 2016 2025 EnglishHo Sy VietNo ratings yet

- Dispute To Creditor For Charge OffDocument4 pagesDispute To Creditor For Charge Offrodney75% (20)

- RHED Financing Application Form 1Document2 pagesRHED Financing Application Form 1Kenneth InuiNo ratings yet

- Pdpa CraDocument3 pagesPdpa CraAdyrah RahmanNo ratings yet

- Extreme Privacy: What It Takes To Disappear in AmericaDocument34 pagesExtreme Privacy: What It Takes To Disappear in Americaalessandra100% (1)

- SAP Credit Management: Functional Overview SAP Credit Management in S/4HANADocument5 pagesSAP Credit Management: Functional Overview SAP Credit Management in S/4HANAccst74100% (1)

- Project Report On Credit RatingDocument15 pagesProject Report On Credit RatingShambhu Kumar100% (4)

- TransUnion Credit ReportDocument34 pagesTransUnion Credit ReportMilan HarrisonNo ratings yet

- PBB Consent DisclosureDocument1 pagePBB Consent DisclosureMohd ZuhairiNo ratings yet

- 21st Century LiteraciesDocument27 pages21st Century LiteraciesYuki SeishiroNo ratings yet

- Notice of Intent To File A Lawsuit2Document3 pagesNotice of Intent To File A Lawsuit2FreedomofMind100% (3)

- Habib Bank Limited Personal LoanDocument2 pagesHabib Bank Limited Personal LoanKhawar A BalochNo ratings yet

- 151-6 Exhibit S & A Loans ForgivenDocument41 pages151-6 Exhibit S & A Loans Forgivenlarry-612445No ratings yet

- Credit AppraisalDocument49 pagesCredit AppraisalRam Vishrojwar50% (2)

- 4-CONSUMER CREDIT (PART 1) (Introduction To Consumer Credit)Document31 pages4-CONSUMER CREDIT (PART 1) (Introduction To Consumer Credit)Muhamad IhsanNo ratings yet

- BCC Study GuideDocument44 pagesBCC Study GuideTemne HardawayNo ratings yet

- SKS - Microfinance.ltd - Annual.report.2011 12Document120 pagesSKS - Microfinance.ltd - Annual.report.2011 12Nikhil BoggarapuNo ratings yet

- Dun & Brad StreetDocument7 pagesDun & Brad StreetAbhilas DasNo ratings yet

- Unionbank Loan Application FormDocument1 pageUnionbank Loan Application Formperrybc427No ratings yet

- Credit Explained Leaflet 2005Document24 pagesCredit Explained Leaflet 2005ericagen53No ratings yet

- CRS DocumentDocument63 pagesCRS DocumentSalmanFatehAliNo ratings yet

- Rental Application SummaryDocument3 pagesRental Application SummaryAbhay KumarNo ratings yet

- Https WWW - DiscovercardDocument2 pagesHttps WWW - DiscovercardKarthik V KalyaniNo ratings yet

- Declined Rental Application Due to Credit ReportDocument3 pagesDeclined Rental Application Due to Credit ReportToolie BeeNo ratings yet