You might also like

- Law Assignment-02Document11 pagesLaw Assignment-02Bushra NaumanNo ratings yet

- Unilever Pakistan Strategic AnalysisDocument10 pagesUnilever Pakistan Strategic Analysis5210937No ratings yet

- Macroeconomic Theories of Inflation PDFDocument4 pagesMacroeconomic Theories of Inflation PDFBushra Nauman100% (1)

- Factors Behind Pakistan's Recent InflationDocument18 pagesFactors Behind Pakistan's Recent InflationBushra NaumanNo ratings yet

- Group1-The Interview ProcessDocument11 pagesGroup1-The Interview ProcessBushra NaumanNo ratings yet

- Lecture - 3 FinalDocument34 pagesLecture - 3 FinalBushra NaumanNo ratings yet

- Agricultural Policy PDFDocument6 pagesAgricultural Policy PDFBushra NaumanNo ratings yet

- Causes of InflationDocument25 pagesCauses of InflationBushra NaumanNo ratings yet

- Analysis of Musharraf Era 1999-2008Document37 pagesAnalysis of Musharraf Era 1999-2008Bushra NaumanNo ratings yet

- Agricultural PolicyDocument5 pagesAgricultural PolicyBushra NaumanNo ratings yet

- Chapter 4 Consumption, Saving, and InvestmentDocument35 pagesChapter 4 Consumption, Saving, and InvestmentBushra NaumanNo ratings yet

- No 03. Chapter 2: Measuring Macroeconomic VariablesDocument23 pagesNo 03. Chapter 2: Measuring Macroeconomic VariablesBushra NaumanNo ratings yet

- Chapter 9 - Performance Management and Appraisal (080809)Document49 pagesChapter 9 - Performance Management and Appraisal (080809)Bushra Nauman100% (4)

- Lecture - 3 FinalDocument34 pagesLecture - 3 FinalBushra NaumanNo ratings yet

- Chapter 12 LeadershipDocument70 pagesChapter 12 LeadershipBushra Nauman100% (3)

- Ethics in ResearchDocument2 pagesEthics in ResearchBushra NaumanNo ratings yet

- Chapter 5 Skills Behaviours and CompetenciesDocument15 pagesChapter 5 Skills Behaviours and CompetenciesBushra NaumanNo ratings yet

- Business Research Methods ZikmundDocument28 pagesBusiness Research Methods ZikmundSyed Rehan AhmedNo ratings yet

- A Diamond PersonalityDocument12 pagesA Diamond PersonalityBushra NaumanNo ratings yet

- Barriers To CommunicationDocument2 pagesBarriers To CommunicationBushra NaumanNo ratings yet

- Perceptual and Language DifferencesDocument2 pagesPerceptual and Language DifferencesBushra Nauman100% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- An Analysis of Personal Financial Lit Among College StudentsDocument22 pagesAn Analysis of Personal Financial Lit Among College StudentsRamanarayana BharadwajNo ratings yet

- Insurance: M.J.Malik-Sba-Ahmedabad-09879094925MWPADocument21 pagesInsurance: M.J.Malik-Sba-Ahmedabad-09879094925MWPAkrunalk2003100% (1)

- Assume That You Recently Graduated With A Degree in FinanceDocument1 pageAssume That You Recently Graduated With A Degree in FinanceAmit PandeyNo ratings yet

- Understanding Macro Economics PerformanceDocument118 pagesUnderstanding Macro Economics PerformanceViral SavlaNo ratings yet

- EuroCham Vietnam Newsletter Q1 2012Document28 pagesEuroCham Vietnam Newsletter Q1 2012European Chamber of Commerce in VietnamNo ratings yet

- Zonal OfficeDocument1 pageZonal OfficeDeeprajNo ratings yet

- Confirmation Form (R1 CAR)Document3 pagesConfirmation Form (R1 CAR)Pisto PalubosNo ratings yet

- RURAL Banking in India ProjectDocument107 pagesRURAL Banking in India Projectdevendra68% (28)

- Sum of The Charts: "Trading Places": Technical AnalysisDocument31 pagesSum of The Charts: "Trading Places": Technical AnalysisArtur SilvaNo ratings yet

- Historical Development of The Banking SystemDocument8 pagesHistorical Development of The Banking SystemHustice FreedNo ratings yet

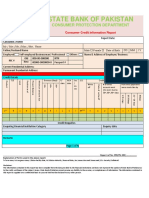

- Consumer Credit Report Format.Document3 pagesConsumer Credit Report Format.Naeem RaoNo ratings yet

- Chapter-1 Introduction To Project Report: Comparative AnalysisDocument42 pagesChapter-1 Introduction To Project Report: Comparative AnalysisamoghvkiniNo ratings yet

- Batch 19 1st Preboard (P1)Document12 pagesBatch 19 1st Preboard (P1)Mike Oliver Nual100% (1)

- Interim Order in The Matter of Mr. Anirudh SethiDocument14 pagesInterim Order in The Matter of Mr. Anirudh SethiShyam SunderNo ratings yet

- Loan Account Statement For LUCHD00037184487Document4 pagesLoan Account Statement For LUCHD00037184487abhishek parasarNo ratings yet

- BCG Corporate Treasury Insights 2015Document19 pagesBCG Corporate Treasury Insights 2015thesrajesh7120100% (1)

- Your Steps To A 720 Credit ScoreDocument15 pagesYour Steps To A 720 Credit Scorecharlesthurston100% (3)

- Credit Transactions - Syllabus PDFDocument5 pagesCredit Transactions - Syllabus PDFMarviah Vanessa HernandezNo ratings yet

- Digital Payments and Their Impact On The IndianDocument20 pagesDigital Payments and Their Impact On The Indiannivethitha aNo ratings yet

- A Comparative Study On Financial Literacy Among Arts and Science College Students Ijariie3989Document5 pagesA Comparative Study On Financial Literacy Among Arts and Science College Students Ijariie3989Shobiga V100% (1)

- Province of Antique Unadjusted Trial Balance As of August 2017 All FundsDocument4 pagesProvince of Antique Unadjusted Trial Balance As of August 2017 All FundsDom Minix del RosarioNo ratings yet

- Chapter #2 International Financial Management. MBADocument10 pagesChapter #2 International Financial Management. MBAAsad Abbas KhadimNo ratings yet

- Determinants of Financial Performance of Commercial Banks in EthiopiaDocument8 pagesDeterminants of Financial Performance of Commercial Banks in Ethiopiamesfin DemiseNo ratings yet

- DALDA AR QuestionaireDocument8 pagesDALDA AR QuestionaireAnum ImranNo ratings yet

- Chapter 6 2Document7 pagesChapter 6 2ArkokhanNo ratings yet

- Template Koreksi TK Norek 17041510Document7 pagesTemplate Koreksi TK Norek 17041510Dian Abdi WinataNo ratings yet

- Annuities Practice Problems Prepared by Pamela Peterson DrakeDocument3 pagesAnnuities Practice Problems Prepared by Pamela Peterson DrakeJohn AlagaoNo ratings yet

- Gyanmgeneralawarenessjuly2016 160702101738Document101 pagesGyanmgeneralawarenessjuly2016 160702101738Ishaan DodaNo ratings yet

- Common Error-2 (Bank P.O. Year Wise) Presentable FormatDocument22 pagesCommon Error-2 (Bank P.O. Year Wise) Presentable FormatDhananjay Chandra0% (1)

- Chapter 7 Posting To The LedgerDocument12 pagesChapter 7 Posting To The LedgerBLANKNo ratings yet