You might also like

- EXID - Every Night Lyrics: RomanizedDocument4 pagesEXID - Every Night Lyrics: RomanizedYenyensmileNo ratings yet

- EXID - Every Night Lyrics: RomanizedDocument4 pagesEXID - Every Night Lyrics: RomanizedYenyensmileNo ratings yet

- CONTOH Surat Lamaran KerjaDocument5 pagesCONTOH Surat Lamaran KerjaElzaSafitriNo ratings yet

- The Roman Collections 2012Document38 pagesThe Roman Collections 2012Yenyensmile100% (1)

- Tutorial Use Hdri in Vray For Sketchup 8Document3 pagesTutorial Use Hdri in Vray For Sketchup 8YenyensmileNo ratings yet

- ResumeDocument2 pagesResumechristinaprinceNo ratings yet

- Resume TemplateDocument2 pagesResume TemplatevxmlqfNo ratings yet

- Animating 4-Legged Animals GuideDocument11 pagesAnimating 4-Legged Animals GuideGbenga SawyerrNo ratings yet

- CONTOH Surat Lamaran KerjaDocument5 pagesCONTOH Surat Lamaran KerjaElzaSafitriNo ratings yet

- ResumeDocument2 pagesResumechristinaprinceNo ratings yet

- Tutorial For Rendering Trees and Shrubs in 2d With PNG FormatsDocument5 pagesTutorial For Rendering Trees and Shrubs in 2d With PNG FormatsYenyensmileNo ratings yet

- FT Island - MadlyDocument1 pageFT Island - MadlyYenyensmileNo ratings yet

- Chapter 7Document98 pagesChapter 7Arlien GerosanibNo ratings yet

- Formula Sheet For Finman2 CB Decision CriteriaDocument2 pagesFormula Sheet For Finman2 CB Decision CriteriaRan MerroNo ratings yet

- Titman CH 11Document130 pagesTitman CH 11YenyensmileNo ratings yet

- Abnormal Stock Returns, For The Event Firm and Its Rivals, Following The Event Firm's Large One-Day Stock Price DropDocument22 pagesAbnormal Stock Returns, For The Event Firm and Its Rivals, Following The Event Firm's Large One-Day Stock Price DropSalviana ShuNo ratings yet

- Titman CH 10Document90 pagesTitman CH 10YenyensmileNo ratings yet

- The Next Big Thing - Samsung Galaxy S II (90 Sec Commerical)Document14 pagesThe Next Big Thing - Samsung Galaxy S II (90 Sec Commerical)YenyensmileNo ratings yet

- M02 Titman 2544318 11 FinMgt C02Document57 pagesM02 Titman 2544318 11 FinMgt C02kennethfarnumNo ratings yet

- Titman CH 09Document150 pagesTitman CH 09Yenyensmile100% (1)

- TKM CH 06Document135 pagesTKM CH 06sangarfreeNo ratings yet

- Performance Management ProcessDocument25 pagesPerformance Management ProcessShiena Marie BarbechoNo ratings yet

- Titman CH 04Document151 pagesTitman CH 04Yenyensmile0% (1)

- Chap 1Document49 pagesChap 1Andre ShieldsNo ratings yet

- Titman CH 05Document115 pagesTitman CH 05YenyensmileNo ratings yet

- 2AM - One Spring DayDocument1 page2AM - One Spring DayYenyensmileNo ratings yet

- Titman CH 03Document124 pagesTitman CH 03YenyensmileNo ratings yet

- SISTAR19 - Gone, Not Around Any LongerDocument1 pageSISTAR19 - Gone, Not Around Any LongerYenyensmileNo ratings yet

- Davichi - Because It's YouDocument1 pageDavichi - Because It's YouYenyensmileNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 08 Chapter 3Document79 pages08 Chapter 3Oii SaralNo ratings yet

- The Most Dangerous Organization in America ExposedDocument37 pagesThe Most Dangerous Organization in America ExposedDomenico Bevilacqua100% (1)

- The Currency Trader's Handbook: by Rob Booker, ©2002-2006Document23 pagesThe Currency Trader's Handbook: by Rob Booker, ©2002-2006Pandelis NikolopoulosNo ratings yet

- Trump's June 3, 2016 Tax BillDocument2 pagesTrump's June 3, 2016 Tax Billcrainsnewyork67% (3)

- CH 4: Apply Your Knowledge Decision Case 4-1: Accounting 9/e Solutions Manual 392Document15 pagesCH 4: Apply Your Knowledge Decision Case 4-1: Accounting 9/e Solutions Manual 392Loany Martinez100% (1)

- Real Estate Investments and The Inflation-Hedging Question: A ReviewDocument10 pagesReal Estate Investments and The Inflation-Hedging Question: A ReviewShanza KhalidNo ratings yet

- EpaymentDocument18 pagesEpaymentAbbas LalaniNo ratings yet

- Dutch Lady Company - Construct A Cash Budget (Task Group) - Kba2431a - Fin420Document12 pagesDutch Lady Company - Construct A Cash Budget (Task Group) - Kba2431a - Fin420MOHAMAD IZZANI OTHMANNo ratings yet

- Quizzes - Topic 6 - Leases - Xem L I Bài LàmDocument4 pagesQuizzes - Topic 6 - Leases - Xem L I Bài LàmHải YếnNo ratings yet

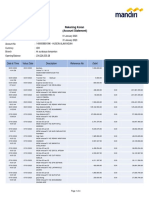

- Rek Koran Mandiri PT HAI Jan-April 2023Document14 pagesRek Koran Mandiri PT HAI Jan-April 2023wahyu suhartonoNo ratings yet

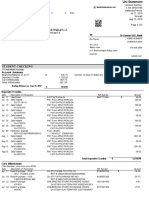

- mPassBook - 20230114 - 20230413 - 6005 UNLOCKEDDocument3 pagesmPassBook - 20230114 - 20230413 - 6005 UNLOCKEDAshish kumarNo ratings yet

- GGCADocument2 pagesGGCAPrakash BaldaniyaNo ratings yet

- US Bank StatementDocument4 pagesUS Bank StatementBlake Hudson100% (2)

- Clarkson Lumber SolutionDocument8 pagesClarkson Lumber Solutionpawangadiya1210No ratings yet

- PAN Application (881020124470496)Document2 pagesPAN Application (881020124470496)Sandeep SheoranNo ratings yet

- Fcma, Fpa, Ma (Economics), BSC Dubai, United Arab Emirates: Presentation byDocument42 pagesFcma, Fpa, Ma (Economics), BSC Dubai, United Arab Emirates: Presentation byAhmad Tariq Bhatti100% (1)

- Accounting 202 Strategic Business AnalysisDocument6 pagesAccounting 202 Strategic Business AnalysisJona Francisco0% (1)

- Chapter 1 Problems Working PapersDocument5 pagesChapter 1 Problems Working PapersZachLovingNo ratings yet

- Cfp-9353-Gryphon Graphite Chemical Industries LTDDocument2 pagesCfp-9353-Gryphon Graphite Chemical Industries LTDtheatresonicNo ratings yet

- Investment - Audit Program - HandoutsDocument2 pagesInvestment - Audit Program - HandoutsRoquessa Michel R. IgnaligNo ratings yet

- These Materials Were Produced For Insidesherpa and To Be Used For Educational and Training Purposes OnlyDocument2 pagesThese Materials Were Produced For Insidesherpa and To Be Used For Educational and Training Purposes OnlyTech Dealer50% (2)

- Statement of Changes in EquityDocument3 pagesStatement of Changes in EquitybarrylucasNo ratings yet

- Effects of Merchant Banking on Financial Growth of ICICIDocument62 pagesEffects of Merchant Banking on Financial Growth of ICICIij EducationNo ratings yet

- RBI's Credit Monitoring Arrangement and Tandon Committee recommendationsDocument4 pagesRBI's Credit Monitoring Arrangement and Tandon Committee recommendationsAbhi_IMK100% (1)

- Bond Pricing CalculatorDocument37 pagesBond Pricing CalculatorFurqan Farooq Vadharia100% (1)

- AR IBY IntegrationDocument36 pagesAR IBY IntegrationManikBahl1100% (2)

- Financial Analysis of Highway Project ModelsDocument3 pagesFinancial Analysis of Highway Project ModelsPayal ChauhanNo ratings yet

- Shubh Nivesh Brochure - BRDocument15 pagesShubh Nivesh Brochure - BRSumit RpNo ratings yet

- 2021 Annual Financial Report For The National Government Volume IDocument506 pages2021 Annual Financial Report For The National Government Volume IAliah MagumparaNo ratings yet

- Currency Exchange Rate and International Trade and Capital FlowsDocument39 pagesCurrency Exchange Rate and International Trade and Capital FlowsudNo ratings yet