You might also like

- English LiteracyDocument7 pagesEnglish LiteracyMehul RasadiyaNo ratings yet

- English Tense RanjitDocument1 pageEnglish Tense RanjitPrashant PatelNo ratings yet

- MR - Rasadiya Mehulkumar HimmatbhaiDocument5 pagesMR - Rasadiya Mehulkumar HimmatbhaiMehul RasadiyaNo ratings yet

- Lowe LintasDocument3 pagesLowe LintasMehul RasadiyaNo ratings yet

- DefinitionsDocument38 pagesDefinitionsMehul RasadiyaNo ratings yet

- VikasDocument2 pagesVikasMehul RasadiyaNo ratings yet

- Tata Tea CompanyDocument4 pagesTata Tea CompanyMehul RasadiyaNo ratings yet

- My SelfDocument2 pagesMy SelfMehul RasadiyaNo ratings yet

- Home Industry Information: PharmaceuticalsDocument6 pagesHome Industry Information: PharmaceuticalsMehul RasadiyaNo ratings yet

- Wich Haves Atlist For Products. Also Prepair A Grafic Art of The List For ProductsDocument1 pageWich Haves Atlist For Products. Also Prepair A Grafic Art of The List For ProductsMehul RasadiyaNo ratings yet

- Entrepreneur RATAN TATADocument9 pagesEntrepreneur RATAN TATAHimangi GuptaNo ratings yet

- Harshad Mehta & Ketan Parekh ScamDocument6 pagesHarshad Mehta & Ketan Parekh Scammeet22591No ratings yet

- Business Plans: Management Plans and Organizational ReshufflingDocument5 pagesBusiness Plans: Management Plans and Organizational ReshufflingMehul RasadiyaNo ratings yet

- Use of Computers in Swiss Banks PDFDocument10 pagesUse of Computers in Swiss Banks PDFMehul RasadiyaNo ratings yet

- Mobile Divides: Gender, Socioeconomic Status, and Mobile Phone Use in RwandaDocument13 pagesMobile Divides: Gender, Socioeconomic Status, and Mobile Phone Use in RwandaMehul RasadiyaNo ratings yet

- IMC Promotion Mix Tools Top Mind AwarenessDocument11 pagesIMC Promotion Mix Tools Top Mind AwarenessMehul RasadiyaNo ratings yet

- GTU Comprehensive ProjectDocument13 pagesGTU Comprehensive ProjectMohammed GheewalaNo ratings yet

- Swiss banks neglect IT innovation potentialDocument4 pagesSwiss banks neglect IT innovation potentialMehul RasadiyaNo ratings yet

- SimulaDocument42 pagesSimulaMehul RasadiyaNo ratings yet

- Print CV RipalDocument4 pagesPrint CV RipalMehul RasadiyaNo ratings yet

- Enhancing Business-Community Relations Tata Steel Case StudyDocument9 pagesEnhancing Business-Community Relations Tata Steel Case StudyMehul RasadiyaNo ratings yet

- Business Plan 1Document10 pagesBusiness Plan 1Sethra SenNo ratings yet

- Essar Oil (CMA)Document20 pagesEssar Oil (CMA)Mehul RasadiyaNo ratings yet

- WIPRO PreparationDocument45 pagesWIPRO Preparationpayal05bhuptaniNo ratings yet

- Human Resource PlanningDocument12 pagesHuman Resource PlanningleyajacobNo ratings yet

- Recruitment Process in AirtelDocument24 pagesRecruitment Process in AirtelKriti KhoslaNo ratings yet

- Simulation 4Document14 pagesSimulation 4Mehul RasadiyaNo ratings yet

- L'Oreal SWOTDocument18 pagesL'Oreal SWOTdearlatviaNo ratings yet

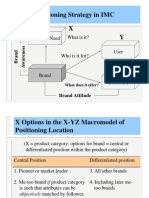

- Brand Positioning Strategy in IMC X Y: Category Need What Is It?Document10 pagesBrand Positioning Strategy in IMC X Y: Category Need What Is It?Mehul RasadiyaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)