You might also like

- NGAS: New Government Accounting SystemDocument56 pagesNGAS: New Government Accounting SystemVenianNo ratings yet

- Accounting For LGUsDocument34 pagesAccounting For LGUsKath O100% (1)

- Chapter 1 - New Government Accounting System (Ngas)Document28 pagesChapter 1 - New Government Accounting System (Ngas)MA ValdezNo ratings yet

- Ngas Vol 1 To 6 Acctng PoliciesDocument184 pagesNgas Vol 1 To 6 Acctng PoliciesresurgumNo ratings yet

- Chapter 5 Accounting For Disbursements and Related TransactionsDocument2 pagesChapter 5 Accounting For Disbursements and Related TransactionsJaps100% (1)

- CHAPTER 2 - Unified Accounts Code StructureDocument56 pagesCHAPTER 2 - Unified Accounts Code StructureRafael VictoriaNo ratings yet

- Introduction to Government Accounting and the Philippine Budget ProcessDocument20 pagesIntroduction to Government Accounting and the Philippine Budget ProcessLaong laan100% (1)

- Pre-1. Introduction To Government AccountingDocument24 pagesPre-1. Introduction To Government AccountingPaupauNo ratings yet

- Government Accounting and Budgeting Module at Don Mariano Marcos Memorial State UniversityDocument36 pagesGovernment Accounting and Budgeting Module at Don Mariano Marcos Memorial State UniversityErika MonisNo ratings yet

- Concept of Funds-Dr. Loida M. CancinoDocument81 pagesConcept of Funds-Dr. Loida M. CancinoAricirtap Abenoja JoyceNo ratings yet

- The PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingDocument98 pagesThe PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingJhopel Casagnap EmanNo ratings yet

- Government Accounting ManualDocument62 pagesGovernment Accounting ManualDez Za100% (1)

- Revenue and Other Receipts - ScriptDocument30 pagesRevenue and Other Receipts - ScriptChristine Leal-Estender100% (2)

- Govt Acctg Manual ExplainedDocument3 pagesGovt Acctg Manual ExplainedLabLab ChattoNo ratings yet

- Ac 518 Hand-Outs Government Accounting and Auditing TNCR: The National Government of The PhilippinesDocument53 pagesAc 518 Hand-Outs Government Accounting and Auditing TNCR: The National Government of The PhilippinesHarley Gumapon100% (1)

- Conducting Cash Exams Step-by-StepDocument22 pagesConducting Cash Exams Step-by-StepBon Carlo Medina MelocotonNo ratings yet

- PPE Accounting GuideDocument35 pagesPPE Accounting GuideShane KimNo ratings yet

- Accounting for Government, Not-for-Profits and Specialized IndustriesDocument58 pagesAccounting for Government, Not-for-Profits and Specialized IndustriesSandra DoriaNo ratings yet

- The Accounting Policies: Government Accounting Manual For Local Government UnitsDocument259 pagesThe Accounting Policies: Government Accounting Manual For Local Government UnitsKyla Ramos Diamsay100% (1)

- AA 4102 1st Hand OutDocument9 pagesAA 4102 1st Hand OutMana XDNo ratings yet

- Government Accounting & Non-Profit Organizations PPEDocument38 pagesGovernment Accounting & Non-Profit Organizations PPENoeline ParafinaNo ratings yet

- GAM-property Plant and EquipmentDocument83 pagesGAM-property Plant and EquipmentRobert CastilloNo ratings yet

- Presentation of Financial Statements Standard for Philippine Public SectorDocument18 pagesPresentation of Financial Statements Standard for Philippine Public SectorAnonymous bEDr3JhGNo ratings yet

- Government AccountingDocument32 pagesGovernment AccountingLaika Mae D. CariñoNo ratings yet

- 001 Government AccountingDocument75 pages001 Government AccountingMark Brian Parantar100% (1)

- Introduction to Government AccountingDocument55 pagesIntroduction to Government AccountingSixto July100% (1)

- BLGF ESRE Harmonization Guidelines March 2012Document54 pagesBLGF ESRE Harmonization Guidelines March 2012LalaLanibaNo ratings yet

- Government Accounting Ch1Document31 pagesGovernment Accounting Ch1John Evan Raymund Besid100% (1)

- Module 1 - Overview of Government AccountingDocument5 pagesModule 1 - Overview of Government AccountingJebong CaguitlaNo ratings yet

- T08 - Government Accounting PDFDocument9 pagesT08 - Government Accounting PDFAken Lieram Ats AnaNo ratings yet

- The Budget ProcessDocument22 pagesThe Budget ProcessFrank James100% (1)

- Government Accounting Overview of Government AccountingDocument77 pagesGovernment Accounting Overview of Government AccountingMichael Brian Torres100% (1)

- Understanding the UACS Code StructureDocument5 pagesUnderstanding the UACS Code StructureJamila Zarsuelo100% (1)

- DBM BudgetDocument85 pagesDBM BudgetGab Pogi100% (1)

- Implementing Government Disbursement ControlsDocument12 pagesImplementing Government Disbursement ControlsMerlina Cuare100% (1)

- 08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsDocument22 pages08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsGil DavinNo ratings yet

- Government Accounting: Accounting For Non-Profit OrganizationsDocument88 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsDe GuzmanNo ratings yet

- Topic Outline For Public Accounting and BudgetingDocument8 pagesTopic Outline For Public Accounting and Budgetingsabel sardillaNo ratings yet

- Principles of Business Taxes - PPTDocument19 pagesPrinciples of Business Taxes - PPTAlex CruzNo ratings yet

- Overview Obnbn PPSASDocument44 pagesOverview Obnbn PPSASJenofDulwn0% (1)

- Government Accounting OverviewDocument18 pagesGovernment Accounting OverviewCherrie Arianne Fhaye Naraja100% (1)

- 139 Governmental Accounting HO PDFDocument6 pages139 Governmental Accounting HO PDFSankalp Singh100% (1)

- Government Accounting Auditing & ProcurementDocument97 pagesGovernment Accounting Auditing & Procurementjamie c100% (1)

- Government Accounting ReportDocument48 pagesGovernment Accounting ReportReina Regina S. CamusNo ratings yet

- COA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsDocument6 pagesCOA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsJonson PalmaresNo ratings yet

- Audit Plan TESDA-DSF LongDocument10 pagesAudit Plan TESDA-DSF LongRussel SarachoNo ratings yet

- Features of the Government Accounting ManualDocument30 pagesFeatures of the Government Accounting ManualMay Joy ManagdagNo ratings yet

- Audit Report Real Property TaxDocument6 pagesAudit Report Real Property TaxJomar Villena0% (1)

- TMAP - DOF-BLGF Policy UpdatesDocument35 pagesTMAP - DOF-BLGF Policy UpdatesPena Tn100% (1)

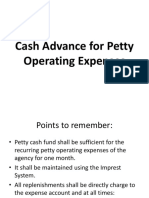

- Cash Advance For Petty Operating ExpensesDocument25 pagesCash Advance For Petty Operating ExpensesGuiller C. Magsumbol100% (2)

- General Accounting Plan Local Government Units: Table 1Document1 pageGeneral Accounting Plan Local Government Units: Table 1Pee-Jay Inigo UlitaNo ratings yet

- Government AccountingDocument10 pagesGovernment AccountingRampotz Ü EchizenNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument12 pagesAccounting For Disbursements and Related TransactionsJustine GuilingNo ratings yet

- Chapter 03 The Government Accounting ProcessDocument20 pagesChapter 03 The Government Accounting ProcessRygiem Dela CruzNo ratings yet

- Example 2 St. Paul Hospital: Net Revenues 4,620,000Document1 pageExample 2 St. Paul Hospital: Net Revenues 4,620,000Von Andrei MedinaNo ratings yet

- Local Budget ProcessDocument3 pagesLocal Budget ProcessLoreen Tonett100% (1)

- Philippine Government Accounting StandardsDocument9 pagesPhilippine Government Accounting StandardsShien AgucayNo ratings yet

- Basic Features and PoliciesDocument3 pagesBasic Features and PoliciesNest ImperialNo ratings yet

- Local Government Accounting PoliciesDocument4 pagesLocal Government Accounting PoliciesGarcia, Ralph Gio P.No ratings yet

- LGU NGAS Ch1 2intro&FeaturesVol1Document7 pagesLGU NGAS Ch1 2intro&FeaturesVol1jhamez16No ratings yet

- Govt Acctg Ch2 Budgetary AcctsDocument58 pagesGovt Acctg Ch2 Budgetary AcctsRachel Sanculi Lustina100% (1)

- Government Accounting for Non-Profit Entities & Specialized IndustriesDocument63 pagesGovernment Accounting for Non-Profit Entities & Specialized IndustriesRachel Sanculi Lustina86% (7)

- XXX Sample of ERM Framework September 2011Document14 pagesXXX Sample of ERM Framework September 2011Rachel Sanculi LustinaNo ratings yet

- Accounting and Budgeting Policies for Local Government UnitsDocument34 pagesAccounting and Budgeting Policies for Local Government UnitsRachel Sanculi LustinaNo ratings yet

- Government Accounting for Non-Profit Entities & Specialized IndustriesDocument63 pagesGovernment Accounting for Non-Profit Entities & Specialized IndustriesRachel Sanculi Lustina86% (7)

- CBCP Monitor Vol14-N12Document20 pagesCBCP Monitor Vol14-N12Areopagus Communications, Inc.No ratings yet

- Catalogo Generale Cuscinetti A Sfere e A Rulli: CorporationDocument412 pagesCatalogo Generale Cuscinetti A Sfere e A Rulli: CorporationAlessandro ManzoniNo ratings yet

- Depository ReceiptsDocument2 pagesDepository Receiptskurdiausha29No ratings yet

- VMware VSphere ICM 6.7 Lab ManualDocument142 pagesVMware VSphere ICM 6.7 Lab Manualitnetman93% (29)

- People VS Hon. Bienvenido TanDocument3 pagesPeople VS Hon. Bienvenido Tanjoy dayagNo ratings yet

- 02 Formal RequisitesDocument8 pages02 Formal Requisitescmv mendozaNo ratings yet

- General and Subsidiary Ledgers ExplainedDocument57 pagesGeneral and Subsidiary Ledgers ExplainedSavage NicoNo ratings yet

- Dyslexia and The BrainDocument5 pagesDyslexia and The BrainDebbie KlippNo ratings yet

- Doctrine of Basic Structure DebateDocument36 pagesDoctrine of Basic Structure DebateSaurabhNo ratings yet

- Achievements of Fatima JinnahDocument5 pagesAchievements of Fatima JinnahmuhammadrafayNo ratings yet

- Module 3 Accounting Cycle Journal EntriesDocument18 pagesModule 3 Accounting Cycle Journal EntriesRoel CababaoNo ratings yet

- Summer Reviewer - Edited 2018Document256 pagesSummer Reviewer - Edited 2018Isabelle Poblete-MelocotonNo ratings yet

- Catherine A. Brown 2017 - Non-Discrimination and Trade in Services - The Role of Tax TreatiesDocument287 pagesCatherine A. Brown 2017 - Non-Discrimination and Trade in Services - The Role of Tax Treatieshodienvietanh2015535016No ratings yet

- The Episteme Journal of Linguistics and Literature Vol 1 No 2 - 4-An Analysis of Presupposition On President Barack ObamaDocument33 pagesThe Episteme Journal of Linguistics and Literature Vol 1 No 2 - 4-An Analysis of Presupposition On President Barack ObamaFebyNo ratings yet

- Oracle Application Express Installation Guide PDFDocument221 pagesOracle Application Express Installation Guide PDFmarcosperez81No ratings yet

- Costing For Maintenance CloudDocument10 pagesCosting For Maintenance CloudYuda PrawiraNo ratings yet

- LIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDocument1 pageLIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDarrenNo ratings yet

- Assigned Cases SpreadsheetDocument13 pagesAssigned Cases SpreadsheetJulius David UbaldeNo ratings yet

- Electrical FoundationDocument2 pagesElectrical FoundationterrenceNo ratings yet

- GoguryeoDocument29 pagesGoguryeoEneaGjonajNo ratings yet

- Ad Intelligence BDocument67 pagesAd Intelligence BSyed IqbalNo ratings yet

- Anarchy (c.1)Document33 pagesAnarchy (c.1)Hidde WeeversNo ratings yet

- Ass. 15 - Gender and Development - Questionnaire - FTC 1.4 StudentsDocument5 pagesAss. 15 - Gender and Development - Questionnaire - FTC 1.4 StudentsKriza mae alvarezNo ratings yet

- Midterm Examination in Capital MarketsDocument3 pagesMidterm Examination in Capital MarketsNekki Joy LangcuyanNo ratings yet

- Test BDocument5 pagesTest Bhjgdjf cvsfdNo ratings yet

- Principles of Islamic Banking at Al-Arafah BankDocument21 pagesPrinciples of Islamic Banking at Al-Arafah BanksupershefatNo ratings yet

- Unified Soil Classification SystemDocument4 pagesUnified Soil Classification SystemRoch battousai100% (1)

- Twelve Reasons To Understand 1 Corinthians 7:21-23 As A Call To Gain Freedom Philip B. Payne © 2009Document10 pagesTwelve Reasons To Understand 1 Corinthians 7:21-23 As A Call To Gain Freedom Philip B. Payne © 2009NinthCircleOfHellNo ratings yet

- Department of Education: Sto. Niño National High SchoolDocument3 pagesDepartment of Education: Sto. Niño National High SchoolMackie BarcebalNo ratings yet

- 2019 Fusion For Energy Financial RegulationDocument60 pages2019 Fusion For Energy Financial Regulationale tof4eNo ratings yet