You might also like

- Using Personality Traits To Understand Behavior: For Personality Puzzle 4 Edition Ch. 7Document7 pagesUsing Personality Traits To Understand Behavior: For Personality Puzzle 4 Edition Ch. 7Aman Singh RajputNo ratings yet

- Ipl 2Document35 pagesIpl 2Aman Singh RajputNo ratings yet

- Barter SystemDocument27 pagesBarter SystemimadNo ratings yet

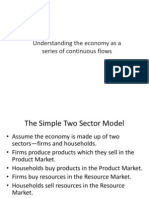

- Understanding The Economy As A Series of Continuous FlowsDocument12 pagesUnderstanding The Economy As A Series of Continuous FlowsAman Singh RajputNo ratings yet

- What Is Macroeconomics? Its OriginDocument55 pagesWhat Is Macroeconomics? Its OriginAman Singh RajputNo ratings yet

- Chapter 12Document27 pagesChapter 12Sajid BhatNo ratings yet

- Keynes' Evolution of Macroeconomics from Say's Law to Aggregate DemandDocument70 pagesKeynes' Evolution of Macroeconomics from Say's Law to Aggregate DemandAman Singh Rajput100% (1)

- Chapter 5Document10 pagesChapter 5Aman Singh RajputNo ratings yet

- Chapter 8Document28 pagesChapter 8Aman Singh RajputNo ratings yet

- Income Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YDocument31 pagesIncome Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YAman Singh RajputNo ratings yet

- Properties of CorrelationDocument2 pagesProperties of CorrelationAman Singh RajputNo ratings yet

- MIS PresentationDocument11 pagesMIS PresentationAman Singh RajputNo ratings yet

- Baumols TheoryDocument35 pagesBaumols TheoryAman Singh Rajput100% (1)

- Alternative To Profit MaximisationDocument11 pagesAlternative To Profit MaximisationAman Singh RajputNo ratings yet

- Manageral EconomicsDocument7 pagesManageral EconomicsimadNo ratings yet

- MIS PresentationDocument11 pagesMIS PresentationAman Singh RajputNo ratings yet

- Product Line Pricing or Multi Product PricingDocument2 pagesProduct Line Pricing or Multi Product PricingAman Singh RajputNo ratings yet

- Baumol's Sales Revenue Maximization Model ExplainedDocument10 pagesBaumol's Sales Revenue Maximization Model ExplainedAman Singh RajputNo ratings yet

- New Product PricingDocument18 pagesNew Product PricingAman Singh RajputNo ratings yet

- Demand ForecastingDocument15 pagesDemand ForecastingAman Singh RajputNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Lalit Narayan Mithila University: Kameshwaranagar, DarbhangaDocument2 pagesLalit Narayan Mithila University: Kameshwaranagar, Darbhangafida mohammadNo ratings yet

- CYB1: Introduction to Cyber Crimes & Banking SecurityDocument37 pagesCYB1: Introduction to Cyber Crimes & Banking Securityanand guptaNo ratings yet

- GR No. 82978Document1 pageGR No. 82978shezeharadeyahoocomNo ratings yet

- SEC Ruling on ASB Rehabilitation PlanDocument4 pagesSEC Ruling on ASB Rehabilitation PlanDenise Capacio LirioNo ratings yet

- Here's Your December 2019 Bank Statement.: Karen Lehman 9936 Gantt RD Red Level AL 36474Document6 pagesHere's Your December 2019 Bank Statement.: Karen Lehman 9936 Gantt RD Red Level AL 36474Karen Lehman100% (1)

- Santana International LLC TradelinesDocument2 pagesSantana International LLC Tradelinesapi-320842283No ratings yet

- Landman Right of Way Agent in Oklahoma City OK Resume David ManningDocument2 pagesLandman Right of Way Agent in Oklahoma City OK Resume David ManningDavid ManningNo ratings yet

- TRSMGT Assignment Case On Valuation of BanksDocument5 pagesTRSMGT Assignment Case On Valuation of BanksKrishna TejNo ratings yet

- Topic 1 Part 1 PDFDocument32 pagesTopic 1 Part 1 PDFsaherhcc4686100% (1)

- Hist Panel EURIBOR Jul 2010Document12 pagesHist Panel EURIBOR Jul 2010JaphyNo ratings yet

- Advanced Finance, Banking and Insurance SamenvattingDocument50 pagesAdvanced Finance, Banking and Insurance SamenvattingLisa TielemanNo ratings yet

- VAT and SD Act 2012 EnglishDocument91 pagesVAT and SD Act 2012 EnglishMonjurul HassanNo ratings yet

- 2014 December Statement PDFDocument1 page2014 December Statement PDFMishaal ShaukatNo ratings yet

- Money Word ListDocument2 pagesMoney Word ListFehér Imola100% (1)

- CDB Consultancy Services Evaluation Report TemplateDocument32 pagesCDB Consultancy Services Evaluation Report TemplateEngr Shahid AbbasNo ratings yet

- British MoneyDocument2 pagesBritish MoneyСофія Вячеславівна ДемировськаNo ratings yet

- BWR assigns BBB rating to Manikaran PowerDocument2 pagesBWR assigns BBB rating to Manikaran PowerCA Rakesh JhaNo ratings yet

- MHA IB Security Asst. and ExecutiveDocument18 pagesMHA IB Security Asst. and ExecutiveTopRankersNo ratings yet

- Find Simple and Compound Interest Rates for Business InvestmentsDocument1 pageFind Simple and Compound Interest Rates for Business InvestmentsBear GummyNo ratings yet

- Payment, Clearing and Settlements Systems in The Euro AreaDocument78 pagesPayment, Clearing and Settlements Systems in The Euro AreaasalihovicNo ratings yet

- E Receipt For State Bank Collect PaymentDocument1 pageE Receipt For State Bank Collect PaymentAyush MukhopadhyayNo ratings yet

- Securitization: An Overview of Concepts, Process, Instruments and RegulationsDocument17 pagesSecuritization: An Overview of Concepts, Process, Instruments and Regulationskhus1985No ratings yet

- Importance of the Five Cs of Finance for CreditworthinessDocument3 pagesImportance of the Five Cs of Finance for Creditworthinessccm internNo ratings yet

- Peer To Peer LendingDocument16 pagesPeer To Peer Lendingykbharti101100% (1)

- FF68 Manual Check DepositDocument10 pagesFF68 Manual Check DepositvittoriojayNo ratings yet

- BillDesk Payment GatewayDocument1 pageBillDesk Payment GatewayDeba MalikNo ratings yet

- E Bucks Gold BusinessDocument40 pagesE Bucks Gold BusinessDanielle Toni Dee NdlovuNo ratings yet

- Parcor Quiz 2Document4 pagesParcor Quiz 2JOY LYN REFUGIONo ratings yet

- Icici ChallanDocument1 pageIcici ChallanKimet Chhendipada AngulNo ratings yet

- Mastercard CaseStudyDocument20 pagesMastercard CaseStudyapi-3757737No ratings yet