You might also like

- Top Ten QuickBooks Tips and TricksDocument52 pagesTop Ten QuickBooks Tips and Tricksjaalcivar100% (2)

- Overview & Financial Analysis On City BankDocument28 pagesOverview & Financial Analysis On City BankMickey Mathew D'CostaNo ratings yet

- Understanding Business Accounting For DummiesFrom EverandUnderstanding Business Accounting For DummiesRating: 3.5 out of 5 stars3.5/5 (8)

- E Cash Payment SystemDocument29 pagesE Cash Payment Systemhareesh64kumar100% (2)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Cfa Books - The Analysis and Use of Financial Statements - Resume - White, Sondhi, WhiteDocument18 pagesCfa Books - The Analysis and Use of Financial Statements - Resume - White, Sondhi, Whiteshare7575100% (3)

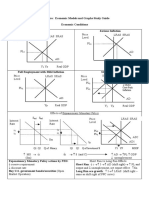

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideGabriel Jimenez100% (7)

- NC-III Bookkeeping ReviewerDocument33 pagesNC-III Bookkeeping ReviewerNovelyn Gamboa92% (52)

- Csec Poa Handout 3Document32 pagesCsec Poa Handout 3Taariq Abdul-MajeedNo ratings yet

- +functions of Commercial BanksDocument15 pages+functions of Commercial Banksredarrow05No ratings yet

- Statements 6792Document4 pagesStatements 6792muchas guataNo ratings yet

- Intermediate Accounting IFRS Edition Chapter 07 Cash and ReceivablesDocument109 pagesIntermediate Accounting IFRS Edition Chapter 07 Cash and ReceivablesAnnisayuniarz100% (4)

- Products and Services Provided by BanksDocument61 pagesProducts and Services Provided by BanksVinay GovilkarNo ratings yet

- Ejercito vs. Sandiganbayan (Special Division)Document106 pagesEjercito vs. Sandiganbayan (Special Division)Evangeline VillajuanNo ratings yet

- BoA Estmt PDF PDF Financial Transaction Deposit AccountDocument1 pageBoA Estmt PDF PDF Financial Transaction Deposit AccountAnthony AndersonNo ratings yet

- Accounts and Notes Receivable NotesDocument50 pagesAccounts and Notes Receivable NotesJimsy Antu67% (3)

- Statement of Financial Position: Fundamentals of Accountancy, Business and Management 2Document55 pagesStatement of Financial Position: Fundamentals of Accountancy, Business and Management 2Arminda Villamin75% (4)

- Cash & Internal ControlDocument17 pagesCash & Internal Controlginish12No ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- Cima F1 Chapter 4Document20 pagesCima F1 Chapter 4MichelaRosignoli100% (1)

- Monzo Bank Statement 2022 05 01-2022 05 02 3891Document3 pagesMonzo Bank Statement 2022 05 01-2022 05 02 3891AlexNo ratings yet

- Accounting Revision Notes 0452Document18 pagesAccounting Revision Notes 0452Hassan AsgharNo ratings yet

- August 2021Document1 pageAugust 2021Julio DelarozaNo ratings yet

- Financial Assets: Unit - 4Document7 pagesFinancial Assets: Unit - 4naseer ahmedNo ratings yet

- Acb3 01Document41 pagesAcb3 01lidetu100% (3)

- CH 07Document99 pagesCH 07homeboimartinNo ratings yet

- Chapter 7Document22 pagesChapter 7Genanew AbebeNo ratings yet

- Accounting For ManagersDocument10 pagesAccounting For ManagersThandapani PalaniNo ratings yet

- About The AuthorDocument11 pagesAbout The AuthorYassi CurtisNo ratings yet

- Financial Accounting and Reporting by Fayieee Prelim To MidtermDocument31 pagesFinancial Accounting and Reporting by Fayieee Prelim To MidtermEnalyn AldeNo ratings yet

- Financial Health: What Is 'Working Capital'Document6 pagesFinancial Health: What Is 'Working Capital'Abhishek BanerjeeNo ratings yet

- Fin621 Hira Khan QuizzDocument16 pagesFin621 Hira Khan QuizzMadiha KhanNo ratings yet

- QuesDocument4 pagesQuesSreejith NairNo ratings yet

- Basics Accounting ConceptsDocument25 pagesBasics Accounting ConceptsMamun Enamul HasanNo ratings yet

- Chapter 3-Cash&ReceivablesDocument22 pagesChapter 3-Cash&ReceivablesDr. Mohammad Noor Alam100% (1)

- 1. Decrease cash2. Decrease cash 3. Increase cash4. Decrease cashDocument17 pages1. Decrease cash2. Decrease cash 3. Increase cash4. Decrease cashInbasaat PirzadaNo ratings yet

- COMPLETED Book 7 BSBFIA303 - Accounts Payable and ReceivableDocument10 pagesCOMPLETED Book 7 BSBFIA303 - Accounts Payable and Receivabletanika0% (2)

- Class NotesDocument45 pagesClass NotesNaveed Whatsapp Status100% (1)

- Abm 003 - ReviewerDocument12 pagesAbm 003 - ReviewerMary Beth Dela CruzNo ratings yet

- Financial Accounting Asia Global 2Nd Edition Williams Test Bank Full Chapter PDFDocument67 pagesFinancial Accounting Asia Global 2Nd Edition Williams Test Bank Full Chapter PDFlovellhebe2v0vn100% (11)

- Fabm 2 Week 1Document60 pagesFabm 2 Week 1Camille Cornelio100% (1)

- Accounting 301 Lecture Notes: Autumn 2013 Paul Febry, CPADocument16 pagesAccounting 301 Lecture Notes: Autumn 2013 Paul Febry, CPABella EveNo ratings yet

- CH 07Document109 pagesCH 07Bayoe AjipNo ratings yet

- Accounts Project 11thDocument6 pagesAccounts Project 11thRishi VithlaniNo ratings yet

- CH 3Document25 pagesCH 3yared gebrewoldNo ratings yet

- Revenue Recognition and Receivables ExplainedDocument24 pagesRevenue Recognition and Receivables ExplainedKapil GoyalNo ratings yet

- Accounting NotesDocument4 pagesAccounting NotesMedinaHashimliNo ratings yet

- Unit 2Document69 pagesUnit 2Simardeep SalujaNo ratings yet

- Basic Components of The Balance Sheet Include:: Reading 26 Understanding Balance SheetsDocument10 pagesBasic Components of The Balance Sheet Include:: Reading 26 Understanding Balance Sheetsnaveen.ibs100% (1)

- Intermediate Accounting 1 NotesDocument18 pagesIntermediate Accounting 1 NotesLyka EstradaNo ratings yet

- Nefas Silk Poly Technic College: Learning GuideDocument43 pagesNefas Silk Poly Technic College: Learning GuideNigussie BerhanuNo ratings yet

- Porter Chapter 7 SolnsDocument42 pagesPorter Chapter 7 SolnsAbhishekThyagarajanNo ratings yet

- Accrual Level 4 Best NoteDocument21 pagesAccrual Level 4 Best NoterresaNo ratings yet

- Financial Statement (Balance Sheet, Trading Account, Profit and Loss Account), Ratio AnalysisDocument52 pagesFinancial Statement (Balance Sheet, Trading Account, Profit and Loss Account), Ratio AnalysisRkred237No ratings yet

- Preparation of Balance SheetDocument5 pagesPreparation of Balance SheetPrakashMhatre100% (1)

- Chapter6 - Trial balance and Preparation of Final Accounts яDocument13 pagesChapter6 - Trial balance and Preparation of Final Accounts яshreya taluja100% (1)

- Chapter 04Document60 pagesChapter 04peregrinum100% (2)

- Bank ReconciliationDocument4 pagesBank Reconciliationknowledge musendekwaNo ratings yet

- Intermediate Accounting: Eleventh Canadian EditionDocument62 pagesIntermediate Accounting: Eleventh Canadian EditionthisisfakedNo ratings yet

- In Final Fulfillment of The Curriculum Requirements inDocument56 pagesIn Final Fulfillment of The Curriculum Requirements inangelonoyasam16No ratings yet

- Bank Reconciliation Statement: Names of Sub-UnitsDocument6 pagesBank Reconciliation Statement: Names of Sub-UnitsHermann Schmidt EbengaNo ratings yet

- Explain Bank Reconciliation Statement. Why Is It PreparedDocument6 pagesExplain Bank Reconciliation Statement. Why Is It Preparedjoker.dutta100% (1)

- 100 Basic Accounting Terms For Interview - Accounting CapitalDocument17 pages100 Basic Accounting Terms For Interview - Accounting CapitalRaghunath JhaNo ratings yet

- IFA Chapter 3Document97 pagesIFA Chapter 3kqk07829No ratings yet

- Test Bank For Financial and Managerial Accounting For Mbas 4th Edition EastonDocument36 pagesTest Bank For Financial and Managerial Accounting For Mbas 4th Edition Eastonuprightteel.rpe20h100% (45)

- Cash and Receivables Key PointsDocument64 pagesCash and Receivables Key PointssevtenNo ratings yet

- PorterSM03final FinAccDocument60 pagesPorterSM03final FinAccGemini_0804100% (1)

- Accounting StandardsDocument22 pagesAccounting StandardsSapna Prashant SharmaNo ratings yet

- Entrepreneurship: Quarter 2: Module 7 & 8Document15 pagesEntrepreneurship: Quarter 2: Module 7 & 8Winston MurphyNo ratings yet

- Financial Statements ExplainedDocument2 pagesFinancial Statements ExplainedSambuttNo ratings yet

- Explanatory Notes and Other Disclosures: Mcgraw-Hill/Irwin © 2008 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument18 pagesExplanatory Notes and Other Disclosures: Mcgraw-Hill/Irwin © 2008 The Mcgraw-Hill Companies, Inc., All Rights ReserveddanterozaNo ratings yet

- The Income Statement and The Statement of Cash FlowsDocument31 pagesThe Income Statement and The Statement of Cash FlowsdanterozaNo ratings yet

- Fundamental Financial AccountingDocument29 pagesFundamental Financial AccountingdanterozaNo ratings yet

- Fundamental Financial Accounting Key Terms and Concepts Chapter 8 - Accounting For and Presentation of Owners' EquityDocument2 pagesFundamental Financial Accounting Key Terms and Concepts Chapter 8 - Accounting For and Presentation of Owners' EquitydanterozaNo ratings yet

- Accounting For and Presentation of LiabilitiesDocument32 pagesAccounting For and Presentation of LiabilitiesdanterozaNo ratings yet

- Fundamental Financial Accounting Key Terms and Concepts Chapter 7 - Accounting For and Presentation of LiabilitiesDocument2 pagesFundamental Financial Accounting Key Terms and Concepts Chapter 7 - Accounting For and Presentation of LiabilitiesdanterozaNo ratings yet

- Accounting For and Presentation of Property, Plant, and Equipment, and Other Noncurrent AssetsDocument61 pagesAccounting For and Presentation of Property, Plant, and Equipment, and Other Noncurrent AssetsdanterozaNo ratings yet

- Accounting For and Presentation of Owners' EquityDocument26 pagesAccounting For and Presentation of Owners' EquitydanterozaNo ratings yet

- The Bookkeeping Process and Transaction AnalysisDocument54 pagesThe Bookkeeping Process and Transaction AnalysisdanterozaNo ratings yet

- Fundamental Financial Accounting Key Terms and Concepts Chapter 10 - Corporate Governance, Explanatory Notes, and Other DisclosuresDocument2 pagesFundamental Financial Accounting Key Terms and Concepts Chapter 10 - Corporate Governance, Explanatory Notes, and Other DisclosuresdanterozaNo ratings yet

- Fundamental Financial Accounting Key Terms and Concepts Chapter 6 - Accounting For and Presentation of Property, PlantDocument2 pagesFundamental Financial Accounting Key Terms and Concepts Chapter 6 - Accounting For and Presentation of Property, PlantdanterozaNo ratings yet

- Key Terms and Concepts - CH 09Document2 pagesKey Terms and Concepts - CH 09danterozaNo ratings yet

- Key Terms and Concepts - CH 04Document1 pageKey Terms and Concepts - CH 04danterozaNo ratings yet

- Fundamental Financial Accounting Key Terms and Concepts Chapter 5 - Accounting For and Presentation of Current AssetsDocument3 pagesFundamental Financial Accounting Key Terms and Concepts Chapter 5 - Accounting For and Presentation of Current AssetsdanterozaNo ratings yet

- Homeworks 1 and 2Document4 pagesHomeworks 1 and 2danterozaNo ratings yet

- Key Terms and Concepts - CH 01Document2 pagesKey Terms and Concepts - CH 01danterozaNo ratings yet

- Chap003 RevisedDocument15 pagesChap003 RevisedAnith KumarNo ratings yet

- Key Terms and Concepts - CH 02Document3 pagesKey Terms and Concepts - CH 02danterozaNo ratings yet

- Financial Statements and Accounting Concepts/PrinciplesDocument30 pagesFinancial Statements and Accounting Concepts/PrinciplesdanterozaNo ratings yet

- ASE SyllabusDocument3 pagesASE SyllabusdanterozaNo ratings yet

- Fundamental Financial AccountingDocument29 pagesFundamental Financial AccountingdanterozaNo ratings yet

- Financial Statements and Accounting Concepts/PrinciplesDocument18 pagesFinancial Statements and Accounting Concepts/PrinciplesdanterozaNo ratings yet

- Accounting For and Presentation of Property, Plant, and Equipment, and Other Noncurrent AssetsDocument54 pagesAccounting For and Presentation of Property, Plant, and Equipment, and Other Noncurrent AssetsdanterozaNo ratings yet

- Financial Statements and Accounting Concepts/PrinciplesDocument27 pagesFinancial Statements and Accounting Concepts/PrinciplesdanterozaNo ratings yet

- 8 April Course Lecture - DR LordDocument52 pages8 April Course Lecture - DR LorddanterozaNo ratings yet

- Money Account Fee Schedule: All Fees Amount DetailsDocument2 pagesMoney Account Fee Schedule: All Fees Amount DetailsCarmen PeñaNo ratings yet

- Difference Between Intermittent & Continuous Production SystemDocument3 pagesDifference Between Intermittent & Continuous Production SystemAhmad ShahirNo ratings yet

- Caiib Paper 4 Banking Regulations and Business Laws Capsule AmbitiousDocument223 pagesCaiib Paper 4 Banking Regulations and Business Laws Capsule AmbitiouselliaCruzNo ratings yet

- 11 Exemptions Notes For StudentsDocument43 pages11 Exemptions Notes For StudentsAmanNo ratings yet

- ebankING Uttara BankDocument79 pagesebankING Uttara Bankনীল রহমানNo ratings yet

- 6months Axis StatementDocument10 pages6months Axis Statementjitesh.rajwarNo ratings yet

- Mhasibu Loan Form 2021 .Document5 pagesMhasibu Loan Form 2021 .samNo ratings yet

- Fabm2 - Q2 - M2Document17 pagesFabm2 - Q2 - M2Christopher AbundoNo ratings yet

- Fundamentals of Accountancy, Business and Management 2Document71 pagesFundamentals of Accountancy, Business and Management 2Carmina DongcayanNo ratings yet

- Issues: 15012, July 22, 1975 Recognizing The Debtor-Creditor Relationship of The Bank and TheDocument7 pagesIssues: 15012, July 22, 1975 Recognizing The Debtor-Creditor Relationship of The Bank and TheLisa BautistaNo ratings yet

- Axis BankDocument5 pagesAxis Bankvaibhav tanejaNo ratings yet

- LANDBANK iAccess FAQs: Everything You Need to Know About LANDBANK's Online Banking ServiceDocument13 pagesLANDBANK iAccess FAQs: Everything You Need to Know About LANDBANK's Online Banking ServiceallanjulesNo ratings yet

- Statement of AccountDocument52 pagesStatement of AccountKhalil AfghanNo ratings yet

- Account Statement 160223 150323Document7 pagesAccount Statement 160223 150323SAGAR jangraNo ratings yet

- Act201 CH 8Document10 pagesAct201 CH 8Disya DzakiyyahNo ratings yet

- Cash account audit of Makati CorporationDocument8 pagesCash account audit of Makati CorporationGlizette SamaniegoNo ratings yet

- Banking Act Chapter SummaryDocument48 pagesBanking Act Chapter SummaryShepherd NhangaNo ratings yet

- Deposist AccountDocument6 pagesDeposist AccountwaheedarifNo ratings yet

- STATMENTDocument63 pagesSTATMENTNaveen PandeyNo ratings yet