You might also like

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersRating: 5 out of 5 stars5/5 (5)

- Understanding Business Accounting For DummiesFrom EverandUnderstanding Business Accounting For DummiesRating: 3.5 out of 5 stars3.5/5 (8)

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Economics - Paper 02Document7 pagesEconomics - Paper 02lalNo ratings yet

- Reading Price & Volume Across Multiple Timeframes - Dr. Gary DaytonDocument7 pagesReading Price & Volume Across Multiple Timeframes - Dr. Gary Daytonmr1232375% (8)

- Corporate Finance 9th Edition Solutions Manual Chapter 15Document11 pagesCorporate Finance 9th Edition Solutions Manual Chapter 15agctdna501750% (2)

- Managing Cash and Bank AccountsDocument15 pagesManaging Cash and Bank AccountsFalola Feyisola Richard100% (1)

- Unit # 9 Books of AccountsDocument81 pagesUnit # 9 Books of AccountsZaheer Ahmed SwatiNo ratings yet

- Donner Case Study - MBA 621Document37 pagesDonner Case Study - MBA 621varunragav85No ratings yet

- ASPD 2 Scrapped FinalDocument115 pagesASPD 2 Scrapped FinaliqraNo ratings yet

- Dimensions of Industrial MarketingDocument45 pagesDimensions of Industrial Marketing9986212378100% (2)

- Project On Finalization of Partnership FirmDocument38 pagesProject On Finalization of Partnership Firmvenkynaidu67% (3)

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Hotel Discount GridDocument85 pagesHotel Discount Gridmanishpandey1972No ratings yet

- Journalizing TransactionsDocument38 pagesJournalizing TransactionsPratyush mishraNo ratings yet

- What Is A Cash Book?: Double/two Column Cash Book Triple/three Column Cash BookDocument7 pagesWhat Is A Cash Book?: Double/two Column Cash Book Triple/three Column Cash BookAiman KhanNo ratings yet

- Thomas Rowe Price Investment PhilosophyDocument4 pagesThomas Rowe Price Investment PhilosophyKaran Uppal100% (1)

- Quality Improvement and Statistical Process ControlDocument64 pagesQuality Improvement and Statistical Process ControlSakthi Tharan SNo ratings yet

- Special journals optimize recording transactionsDocument25 pagesSpecial journals optimize recording transactionsYuu100% (1)

- Dip Fin TallyDocument73 pagesDip Fin Tallyceasor007100% (1)

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- Seven Quality ToolsDocument64 pagesSeven Quality Tools9986212378No ratings yet

- The Nature of Industrial BuyingDocument40 pagesThe Nature of Industrial Buying99862123780% (1)

- Business Model Canvas PosterDocument1 pageBusiness Model Canvas PosterVu LeNo ratings yet

- Accounting Calculations - Learning of FundamentalsDocument7 pagesAccounting Calculations - Learning of FundamentalsRobinHood TiwariNo ratings yet

- +1 Accountancy English Chapter 5Document14 pages+1 Accountancy English Chapter 5kalkikaliNo ratings yet

- Journal Accounts To Trial BalanceDocument47 pagesJournal Accounts To Trial Balancebhaskyban100% (1)

- Mba Faaunit - IIDocument15 pagesMba Faaunit - IINaresh GuduruNo ratings yet

- Subsidiary BooksDocument7 pagesSubsidiary BooksRashmi PatelNo ratings yet

- Trial Balance SummaryDocument14 pagesTrial Balance SummarybharathdevareddyNo ratings yet

- What Are The Different Types of Subsidiary Books Usually Maintained by A Firm?Document11 pagesWhat Are The Different Types of Subsidiary Books Usually Maintained by A Firm?sweet19girlNo ratings yet

- 5) JournalDocument24 pages5) JournalRay ChNo ratings yet

- Format of Journal, Ledger and Trial BalanceDocument18 pagesFormat of Journal, Ledger and Trial BalanceSHENUNo ratings yet

- Accounting For Management: Mba 1 Semester Amity Global Business School Ms. Kavitha MenonDocument41 pagesAccounting For Management: Mba 1 Semester Amity Global Business School Ms. Kavitha Menongurudeep25100% (3)

- Accounting 1 Module 9 - The Books of Accounts - Journals Part 1Document19 pagesAccounting 1 Module 9 - The Books of Accounts - Journals Part 1Blanche MargateNo ratings yet

- Diario GeneralDocument28 pagesDiario GeneralMariel PaulinoNo ratings yet

- Ncert Fm-Ac-xi Chapter 4Document59 pagesNcert Fm-Ac-xi Chapter 4shaannivasNo ratings yet

- Accounting CycleDocument2 pagesAccounting CyclepoornapavanNo ratings yet

- Coperative Society FinalDocument41 pagesCoperative Society Finalvenkynaidu100% (1)

- Journal EntriesDocument40 pagesJournal EntriesPai100% (4)

- Binayak Academy,: Gandhi Nagar 1 Line, Near NCC Office, BerhampurDocument16 pagesBinayak Academy,: Gandhi Nagar 1 Line, Near NCC Office, BerhampurkunjapNo ratings yet

- Befa Unit IVDocument12 pagesBefa Unit IVNaresh Guduru93% (15)

- CH-2 Financial Accounting ConceptsDocument40 pagesCH-2 Financial Accounting Conceptsnemik007No ratings yet

- Special journals streamline accounting transactionsDocument14 pagesSpecial journals streamline accounting transactionsCriziel Ann LealNo ratings yet

- Some Cash and Bank TransactionsDocument11 pagesSome Cash and Bank TransactionsSameer ShindeNo ratings yet

- Subsidiary BooksDocument15 pagesSubsidiary BooksJohnPrajwalMendoncaNo ratings yet

- Accounting BooksDocument30 pagesAccounting BooksAshley Keith CadizNo ratings yet

- Books of AccountDocument26 pagesBooks of AccountAngelica Ross de LunaNo ratings yet

- QuesDocument4 pagesQuesSreejith NairNo ratings yet

- 2.2 - LedgerDocument3 pages2.2 - LedgerABHAYNo ratings yet

- Accounts Journals TB P10Document22 pagesAccounts Journals TB P10varadu1963No ratings yet

- Financial Accounting: Reference Books: Accountancy by D. K. Goel Rajesh Goel OR Double Entry Book Keeping by T. S. GrewalDocument27 pagesFinancial Accounting: Reference Books: Accountancy by D. K. Goel Rajesh Goel OR Double Entry Book Keeping by T. S. GrewalBhawna SinghNo ratings yet

- Lecture Notes: Book KeepingDocument15 pagesLecture Notes: Book KeepingSachin D Salankey100% (1)

- Account2 BDocument20 pagesAccount2 BamitpriyashankarNo ratings yet

- Financial Statement AnalysisDocument20 pagesFinancial Statement AnalysisPowerPoint GoNo ratings yet

- 2 - Account - IBBIDocument33 pages2 - Account - IBBIRajwinder Singh Bansal100% (1)

- Ledger and Trial BalanceDocument1 pageLedger and Trial BalanceFaizan ChNo ratings yet

- Fabm1 Wk 2 Session 2 Journals and LedgersDocument43 pagesFabm1 Wk 2 Session 2 Journals and LedgersDomingo Princess JoyNo ratings yet

- Unit 2Document69 pagesUnit 2Simardeep SalujaNo ratings yet

- Define JournalDocument6 pagesDefine JournalOrbin SunnyNo ratings yet

- Books of Accounts: A. JournalDocument3 pagesBooks of Accounts: A. JournalMylen Noel Elgincolin ManlapazNo ratings yet

- Explain Bank Reconciliation Statement. Why Is It PreparedDocument6 pagesExplain Bank Reconciliation Statement. Why Is It Preparedjoker.dutta100% (1)

- Unit 1 Recording of Transactions Lesson-4 Journal StructureDocument23 pagesUnit 1 Recording of Transactions Lesson-4 Journal StructureAmit RawalNo ratings yet

- Book of Accounts WD ActivityDocument3 pagesBook of Accounts WD ActivityChristopher SelebioNo ratings yet

- Dpa1013 Note Chapter 2cDocument18 pagesDpa1013 Note Chapter 2cMohd Noor HamamNo ratings yet

- Ledger PostingDocument19 pagesLedger PostingAbhishek PatilNo ratings yet

- Module 2 Accounts NotesDocument10 pagesModule 2 Accounts Notesveraji3735No ratings yet

- Books of Accounts: Rodmarc P. Sanchez, J.DDocument44 pagesBooks of Accounts: Rodmarc P. Sanchez, J.DDodgeSanchezNo ratings yet

- Accounts PDFDocument46 pagesAccounts PDFArushi Singh100% (1)

- Subsidiary books record transactionsDocument7 pagesSubsidiary books record transactionsRajaRajeswari.LNo ratings yet

- FABM Q3 L5. SLEM 5 - W5 - 2S - Q3 - Books of AccountsDocument14 pagesFABM Q3 L5. SLEM 5 - W5 - 2S - Q3 - Books of AccountsSophia MagdaraogNo ratings yet

- Chapter 6Document57 pagesChapter 6api-358995037100% (1)

- 32 Thinking Hats Explanation and ExerciseDocument3 pages32 Thinking Hats Explanation and ExerciseCharu SharmaNo ratings yet

- Unix & Shell Programming - MCA34Document160 pagesUnix & Shell Programming - MCA34api-3732063100% (1)

- 5 Force ModelDocument2 pages5 Force Model9986212378No ratings yet

- 3D PrintingDocument26 pages3D Printing9986212378No ratings yet

- Merchant BankerDocument7 pagesMerchant Banker9986212378No ratings yet

- Fund Based ServicesDocument6 pagesFund Based Services9986212378No ratings yet

- Decision Making in POMDocument2 pagesDecision Making in POM9986212378No ratings yet

- Performance EvaluationDocument68 pagesPerformance Evaluation9986212378No ratings yet

- Reliance Money: A Reliance Capital CompanyDocument34 pagesReliance Money: A Reliance Capital Company9986212378No ratings yet

- Stock Holding Corporation of India LTD, BangaloreDocument17 pagesStock Holding Corporation of India LTD, Bangalore9986212378No ratings yet

- Evaluation of Portfolio PerformanceDocument80 pagesEvaluation of Portfolio Performance9986212378No ratings yet

- Financial Strategies: Components of F-StrategiesDocument11 pagesFinancial Strategies: Components of F-Strategies9986212378No ratings yet

- Internal & External Equity in Compensation SystemsDocument16 pagesInternal & External Equity in Compensation Systems9986212378No ratings yet

- Module 5Document26 pagesModule 59986212378No ratings yet

- Public Relations: Activities and events to create a positive public imageDocument1 pagePublic Relations: Activities and events to create a positive public image9986212378No ratings yet

- 1Document14 pages19986212378No ratings yet

- Buying Center RolesDocument14 pagesBuying Center Roles9986212378No ratings yet

- Venture CapitalDocument10 pagesVenture Capital9986212378No ratings yet

- Module 1 SDocument16 pagesModule 1 S9986212378No ratings yet

- EFFIE 2002 Case StudiesDocument16 pagesEFFIE 2002 Case Studies9986212378100% (1)

- ImfDocument38 pagesImf9986212378No ratings yet

- Choice of Right Distributors & Channel LogisticsDocument12 pagesChoice of Right Distributors & Channel Logistics9986212378No ratings yet

- Marketing Implications of Identifying Buying Center MembersDocument6 pagesMarketing Implications of Identifying Buying Center Members9986212378100% (1)

- Short-Term Finance and PlanningDocument25 pagesShort-Term Finance and Planningjoe2005No ratings yet

- Financial ManagementDocument13 pagesFinancial Management9986212378No ratings yet

- Short-Term Finance and PlanningDocument25 pagesShort-Term Finance and Planningjoe2005No ratings yet

- Ma. Theresa R. TrinidadDocument3 pagesMa. Theresa R. TrinidadJoshua CalaNo ratings yet

- Quiz 2 Chpts 3 4Document14 pagesQuiz 2 Chpts 3 4Jayden Galing100% (1)

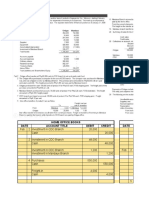

- Home Office Books Mandaue Books Date Account Title Debit Credit DateDocument27 pagesHome Office Books Mandaue Books Date Account Title Debit Credit DateVon Andrei MedinaNo ratings yet

- Assignment Chapter 14Document7 pagesAssignment Chapter 14Yousry El-FoweyNo ratings yet

- Eac694 Group Case Study Yates Control SystemDocument11 pagesEac694 Group Case Study Yates Control SystemVisha KupusamyNo ratings yet

- IMC Advertising Management Presentation1Document20 pagesIMC Advertising Management Presentation1TobalyntiNo ratings yet

- 0-1 Int MKT Course Syllabus (Spring 2023) - Marking GridDocument24 pages0-1 Int MKT Course Syllabus (Spring 2023) - Marking GridHoàng Nam NguyễnNo ratings yet

- Unit 2 - Financial Modelling PDFDocument16 pagesUnit 2 - Financial Modelling PDFDeepakOjhaNo ratings yet

- Name: - Date: - : Table: Consumer Surplus and Phantom TicketsDocument12 pagesName: - Date: - : Table: Consumer Surplus and Phantom TicketsRacaz EwingNo ratings yet

- BA Courses UEHDocument5 pagesBA Courses UEHHoàngNguyênNguyễnNo ratings yet

- Because Cooking Souffl S Is Incredibly Difficult The Supply of Souffl SDocument2 pagesBecause Cooking Souffl S Is Incredibly Difficult The Supply of Souffl Strilocksp SinghNo ratings yet

- Cia 1 FRMDocument4 pagesCia 1 FRMIMRAN KHAN 2127815No ratings yet

- Chandni Pie Coca-Cola ProjectDocument61 pagesChandni Pie Coca-Cola ProjectRaghunath AgarwallaNo ratings yet

- Pepsi's Kurkure Snack Research QuestionnaireDocument4 pagesPepsi's Kurkure Snack Research Questionnairezeshan_channa50% (2)

- Formal Negotiating: Some Questions Answered in This Chapter AreDocument24 pagesFormal Negotiating: Some Questions Answered in This Chapter AreNguyễn Phi YếnNo ratings yet

- Kort Notes ISA'sDocument49 pagesKort Notes ISA'skateNo ratings yet

- AT Quizzer (CPAR) - Audit SamplingDocument2 pagesAT Quizzer (CPAR) - Audit SamplingPrincessNo ratings yet

- Full Name: Mai Thị Loan Class: 12KT201: Accounting ExercisesDocument9 pagesFull Name: Mai Thị Loan Class: 12KT201: Accounting Exercisesthanhyu13No ratings yet

- SM Chapter 8Document7 pagesSM Chapter 8Mustafa AhmedNo ratings yet

- BBS Final Year ProjectDocument39 pagesBBS Final Year ProjectSamsher Kunwar100% (2)

- 05 Coordinate Sales PerformanceDocument14 pages05 Coordinate Sales PerformanceSAMUALE ASSEFA MEKURIYANo ratings yet

- Marketplace Positioning in Indonesia Based On Consumer PerceptionDocument8 pagesMarketplace Positioning in Indonesia Based On Consumer PerceptionUkay MasdukayNo ratings yet