You might also like

- Strategic Compensation PlannningDocument630 pagesStrategic Compensation PlannningArshdev Singh100% (1)

- The Roles of Financial Market and Financial InstitutionsDocument4 pagesThe Roles of Financial Market and Financial InstitutionstssuvroNo ratings yet

- CAT Accelerated Level 1Document4 pagesCAT Accelerated Level 1aliciarigonan100% (1)

- JGSOM Sanggu Majors & Minors ManualDocument23 pagesJGSOM Sanggu Majors & Minors ManualJM Delos ReyesNo ratings yet

- Environmental Awareness CampaignDocument2 pagesEnvironmental Awareness CampaignAshley MartellNo ratings yet

- Advertising and Sales Promotion CHAPTER 3Document17 pagesAdvertising and Sales Promotion CHAPTER 3Jean Greganta BaluyotNo ratings yet

- IDC IT Services Taxonomy 2019Document17 pagesIDC IT Services Taxonomy 2019Alexander RamírezNo ratings yet

- PESTLE Analysis CIPDDocument1 pagePESTLE Analysis CIPDAhmed RaajNo ratings yet

- Functions of Public FinanceDocument6 pagesFunctions of Public FinanceJefferson KagiriNo ratings yet

- Economics 151 RLS UP DilimanDocument3 pagesEconomics 151 RLS UP DilimanRafael SolisNo ratings yet

- Rizal's Early Life and EducationDocument16 pagesRizal's Early Life and EducationAlvinNo ratings yet

- REDUCING NUTRIENT AND PESTICIDE RUNOFFDocument9 pagesREDUCING NUTRIENT AND PESTICIDE RUNOFFslychn100% (1)

- Investment and Portfolio Chapter 4Document48 pagesInvestment and Portfolio Chapter 4MarjonNo ratings yet

- Paknana Cue Atbp. (Name of The Social Enterprise)Document26 pagesPaknana Cue Atbp. (Name of The Social Enterprise)Levi OrtizNo ratings yet

- Service Learning and Community ServiceDocument11 pagesService Learning and Community ServiceGela Nicole DalinaNo ratings yet

- Impacts of HazardsDocument10 pagesImpacts of HazardsCharline A. RadislaoNo ratings yet

- Card MriDocument22 pagesCard MritanudyNo ratings yet

- Chap 2 The Business MissionDocument27 pagesChap 2 The Business MissionFarith HanafiNo ratings yet

- NSTP - Disaster Risk Reduction and Management ConceptsDocument23 pagesNSTP - Disaster Risk Reduction and Management ConceptsSilver Kobe PerezNo ratings yet

- NEW PRODUCT DEVELOPMENT STAGESDocument37 pagesNEW PRODUCT DEVELOPMENT STAGESAditya MaluNo ratings yet

- Policy AdoptionDocument34 pagesPolicy AdoptionJay CaskeyyNo ratings yet

- Semi Final ExamDocument6 pagesSemi Final Examliza campilananNo ratings yet

- Bangko Sentral NG PilipinasDocument59 pagesBangko Sentral NG PilipinasAnn balledosNo ratings yet

- History of Swot AnalysisDocument42 pagesHistory of Swot Analysiscreation toolsNo ratings yet

- Philippine Tax System Changes Under RA 10963Document17 pagesPhilippine Tax System Changes Under RA 10963franz mallariNo ratings yet

- The Importance of Physical Activity and Exercise During The Covid-19 PandemicDocument1 pageThe Importance of Physical Activity and Exercise During The Covid-19 PandemicChryse CreativeNo ratings yet

- Chapter 10 Conflict and Negotiation SummaryDocument24 pagesChapter 10 Conflict and Negotiation SummaryJessica AlbaracinNo ratings yet

- Introduction International Trade TheoryDocument19 pagesIntroduction International Trade TheoryAnuranjanSinhaNo ratings yet

- Thesis Statement Template 13Document2 pagesThesis Statement Template 13Shreeja JhawarNo ratings yet

- YSLEP Monthly Formation MeetingDocument83 pagesYSLEP Monthly Formation MeetingLuzviminda DocotNo ratings yet

- NSTP FormatDocument3 pagesNSTP FormatJason PanganNo ratings yet

- Sesson 9 - The Care For God's CreationDocument21 pagesSesson 9 - The Care For God's CreationCaine de LeonNo ratings yet

- Module 3 - Product Life Cycle in Theory and PracticeDocument11 pagesModule 3 - Product Life Cycle in Theory and PracticeRonald Reagan AlonzoNo ratings yet

- PROJECT PLANNING AND DEVELOPMENT Powerpoint PresentationDocument43 pagesPROJECT PLANNING AND DEVELOPMENT Powerpoint PresentationRyan DagalangitNo ratings yet

- Evolution To Global MarketingDocument6 pagesEvolution To Global Marketingmohittiwarimahi100% (2)

- Module 3 Topic 1 Requirements For A New Cooperative 1Document32 pagesModule 3 Topic 1 Requirements For A New Cooperative 1haron franciscoNo ratings yet

- Empatía y Amabilidad: Humanity in The Midst of Chaos: Reflective EssayDocument3 pagesEmpatía y Amabilidad: Humanity in The Midst of Chaos: Reflective EssayDana IsabelleNo ratings yet

- Product TitleDocument9 pagesProduct TitleAlexis John Altona BetitaNo ratings yet

- Logical Judgment and PropositionsDocument17 pagesLogical Judgment and Propositionsprop andreomsNo ratings yet

- National Service Training Program: Prepared by Marjorie P. Garcia Faculty, CASDocument34 pagesNational Service Training Program: Prepared by Marjorie P. Garcia Faculty, CASJoyce Respicio0% (1)

- Course Syllabus DLSUDocument12 pagesCourse Syllabus DLSUJM Hernandez Villanueva100% (1)

- How To Write An Acknowledgement Letter?Document4 pagesHow To Write An Acknowledgement Letter?Catherine BribonNo ratings yet

- Readingd in Philippine History Fabro, Lesly Ann A. DEC. 15, 2020Document3 pagesReadingd in Philippine History Fabro, Lesly Ann A. DEC. 15, 2020Agyao Yam Faith100% (1)

- REED 203 With Shub 1Document119 pagesREED 203 With Shub 1John Mark CabanesNo ratings yet

- Measure Profitability & EfficiencyDocument2 pagesMeasure Profitability & EfficiencyMeghan Kaye LiwenNo ratings yet

- Workshop: Basic EconomicsDocument120 pagesWorkshop: Basic EconomicsAbrar HussainNo ratings yet

- Definition of Pricing StrategyDocument7 pagesDefinition of Pricing StrategyYvonne WongNo ratings yet

- Dependence Versus Self-Reliance?: Non-Governmental Organizations' Contiguous Beacon of Hope in The PhilippinesDocument8 pagesDependence Versus Self-Reliance?: Non-Governmental Organizations' Contiguous Beacon of Hope in The PhilippinesAlexa.BayNo ratings yet

- Finance ReflectionDocument7 pagesFinance ReflectionItai Francisco ViegasNo ratings yet

- Reflection Paper "How COVID-19 Affected Business Industries?"Document3 pagesReflection Paper "How COVID-19 Affected Business Industries?"Briann Sophia Reyes100% (1)

- Module Unit 1 Ma 326 Hbo BS MaDocument15 pagesModule Unit 1 Ma 326 Hbo BS MaFranciasNo ratings yet

- Impact of Green Marketing on Buying in KolkataDocument10 pagesImpact of Green Marketing on Buying in KolkataRahulNo ratings yet

- SOEN Chapter 1-6 Lecture NotesDocument34 pagesSOEN Chapter 1-6 Lecture NotesCristina Crong MorgiaNo ratings yet

- The Effect of Synchronous and Asynchronous Participation On Students' Performance in Online Accounting CoursesDocument31 pagesThe Effect of Synchronous and Asynchronous Participation On Students' Performance in Online Accounting CoursesHenry James NepomucenoNo ratings yet

- Cost of Capital NotesDocument34 pagesCost of Capital Notesyahspal singhNo ratings yet

- Module 2 General Functions of CreditDocument41 pagesModule 2 General Functions of CreditCaroline Grace Enteria MellaNo ratings yet

- Camilo FinalDocument26 pagesCamilo FinalBarry Rayven Cutaran100% (1)

- Promotion Push Strategy and Human Resource Managements Docs.Document6 pagesPromotion Push Strategy and Human Resource Managements Docs.Lizcel CastillaNo ratings yet

- Mutual Funds 10-17Document49 pagesMutual Funds 10-17I'm YouNo ratings yet

- Selection ProcessDocument21 pagesSelection ProcessJeremiNo ratings yet

- Understanding Culture and Moral DevelopmentDocument4 pagesUnderstanding Culture and Moral DevelopmentJane PadillaNo ratings yet

- Session 19 BudgetingDocument43 pagesSession 19 Budgetingmuskan mittalNo ratings yet

- 2012 PTFCU Interest Rate Risk PolicyDocument8 pages2012 PTFCU Interest Rate Risk PolicyMonkey2111No ratings yet

- Chapt 12A - PromotionDocument40 pagesChapt 12A - PromotionMonkey2111No ratings yet

- Commercial Bank Risk ManagementDocument51 pagesCommercial Bank Risk ManagementMonkey2111No ratings yet

- Oral Statements of Parties at The Second Substantive MeetingDocument12 pagesOral Statements of Parties at The Second Substantive MeetingMonkey2111No ratings yet

- CDBM 01Document5 pagesCDBM 01Hieu NguyenNo ratings yet

- EU Policies Impact on Trung Nguyen CoffeeDocument8 pagesEU Policies Impact on Trung Nguyen CoffeeMonkey2111No ratings yet

- VietinBank EngDocument152 pagesVietinBank EngMonkey2111No ratings yet

- MaritimeBank EngDocument55 pagesMaritimeBank EngMonkey2111No ratings yet

- Sacombank EngDocument96 pagesSacombank EngMonkey2111No ratings yet

- BE - 13 Economic & Monetary UnionDocument12 pagesBE - 13 Economic & Monetary UnionMonkey2111No ratings yet

- BE - 10 Competitive Strategies & Competition CommissionDocument17 pagesBE - 10 Competitive Strategies & Competition CommissionMonkey2111No ratings yet

- 7 Financial MarketsDocument140 pages7 Financial MarketsLe Thuy Dung100% (1)

- Business strategy processDocument8 pagesBusiness strategy processMonkey2111No ratings yet

- 1-Definition of Goals and Objectives v.2Document3 pages1-Definition of Goals and Objectives v.2Monkey2111No ratings yet

- The Economic Problem Opportunity Cost Production Possibility FrontiersDocument10 pagesThe Economic Problem Opportunity Cost Production Possibility FrontiersMonkey2111No ratings yet

- BE 4+Economic+SystemsDocument16 pagesBE 4+Economic+SystemsMonkey2111No ratings yet

- Introduction To BEDocument28 pagesIntroduction To BEMonkey2111No ratings yet

- The Economic Problem Opportunity Cost Production Possibility FrontiersDocument10 pagesThe Economic Problem Opportunity Cost Production Possibility FrontiersMonkey2111No ratings yet

- Responsibilities of Organization and Strategies Employed To Meet Objectives of StakeholdersDocument16 pagesResponsibilities of Organization and Strategies Employed To Meet Objectives of StakeholdersMonkey2111No ratings yet

- BE 2+mission Values Objectives,+Stakeholder+Mapping,+Objectives+of+StakeholdersDocument37 pagesBE 2+mission Values Objectives,+Stakeholder+Mapping,+Objectives+of+StakeholdersMonkey2111No ratings yet

- 01 2012 Risk ToleranceDocument21 pages01 2012 Risk ToleranceMonkey2111No ratings yet

- BE 4+Economic+SystemsDocument16 pagesBE 4+Economic+SystemsMonkey2111No ratings yet

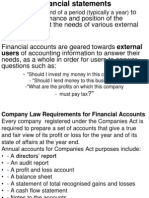

- Purpose of Financial StatementDocument22 pagesPurpose of Financial StatementMonkey2111No ratings yet

- Purpose of Financial StatementDocument22 pagesPurpose of Financial StatementMonkey2111No ratings yet

- ANalyse Budget ClassDocument14 pagesANalyse Budget ClassMonkey2111No ratings yet

- Impacting The Financial StatementsclassDocument23 pagesImpacting The Financial StatementsclassMonkey2111No ratings yet

- Chapt 6 - Marketing Segmentation and PositioningDocument37 pagesChapt 6 - Marketing Segmentation and PositioningMonkey2111No ratings yet

- Chapt 7 - ProductDocument41 pagesChapt 7 - ProductMonkey2111No ratings yet

- Chapt 10 - PricingDocument38 pagesChapt 10 - PricingMonkey2111No ratings yet

- MCQs SPMDocument20 pagesMCQs SPMSalman Habib100% (1)

- Brand Equity of Dettol Brand Equity of Dettol: Rohit Chugh Kankesh Sanjeev Chanika NagarajDocument32 pagesBrand Equity of Dettol Brand Equity of Dettol: Rohit Chugh Kankesh Sanjeev Chanika NagarajrohitchughNo ratings yet

- Control, Risk & Self Assessment by John BarretDocument30 pagesControl, Risk & Self Assessment by John Barretshecat260471100% (1)

- EIS-SM (New) July 21 Suggested Ans InterDocument16 pagesEIS-SM (New) July 21 Suggested Ans InterSPCNo ratings yet

- CIF Change Pointers and TransactionsDocument2 pagesCIF Change Pointers and Transactionsprincepunit79No ratings yet

- Tutorial Chapter 18Document3 pagesTutorial Chapter 18Rounamae lynethNo ratings yet

- Labor Relations Azucena Vol II FinalsDocument54 pagesLabor Relations Azucena Vol II FinalsMitzi PerdidoNo ratings yet

- Malik Animal Wanda (PVT.) LTD: Project Supply Chain ManagementDocument17 pagesMalik Animal Wanda (PVT.) LTD: Project Supply Chain ManagementUsman KhanNo ratings yet

- BOODMO - Trusted Online Portal For Spare Parts For The Carmakers in Indian MarketDocument10 pagesBOODMO - Trusted Online Portal For Spare Parts For The Carmakers in Indian MarketDeepam harodeNo ratings yet

- Akmen Bab 12Document3 pagesAkmen Bab 12Hafizh GalihNo ratings yet

- Advanced Work PackagesDocument24 pagesAdvanced Work Packagescfsolis100% (1)

- Product Lifecycle Management: A Catalyst For Business TransformationDocument12 pagesProduct Lifecycle Management: A Catalyst For Business TransformationgabrielhoyerlmNo ratings yet

- Job EvaluationDocument24 pagesJob EvaluationappusjNo ratings yet

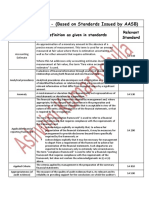

- Audit Dictionary - (Based On Standards Issued by AASB) : Definition As Given in Standards Relevant StandardDocument15 pagesAudit Dictionary - (Based On Standards Issued by AASB) : Definition As Given in Standards Relevant Standardshubham KumarNo ratings yet

- A Sample Compressed Workweek ProgramDocument2 pagesA Sample Compressed Workweek ProgramRoland CepedaNo ratings yet

- BeyondTechnology CreatingBusinessValuewithDataMeshDocument11 pagesBeyondTechnology CreatingBusinessValuewithDataMeshFrancisco DELGADO NIETONo ratings yet

- Resume - Nidhi AggarwalDocument3 pagesResume - Nidhi Aggarwalthatsnidhi_aggNo ratings yet

- Operation BlueprintDocument19 pagesOperation Blueprintjaijohnk100% (1)

- Chapter 4Document27 pagesChapter 4Zeeshan Ali100% (1)

- A Theoretical Framework For Managing Projects PDFDocument56 pagesA Theoretical Framework For Managing Projects PDFabubakkarNo ratings yet

- The Role of The Chief Information Security Officer (CISO) in OrganizationsDocument15 pagesThe Role of The Chief Information Security Officer (CISO) in OrganizationsOussama AkkariNo ratings yet

- Manprod Poltek SSW 1 Maret 2022Document107 pagesManprod Poltek SSW 1 Maret 2022Faradila KookieNo ratings yet

- Prashant ChawlaDocument3 pagesPrashant ChawlaSanjiv DesaiNo ratings yet

- GE6757 - Total Quality Management PDFDocument31 pagesGE6757 - Total Quality Management PDFVashnavi Ruthra100% (1)

- Cap Budge Questions & Answers DR MaphosaDocument38 pagesCap Budge Questions & Answers DR MaphosaCosta MusandipaNo ratings yet

- PLMDocument10 pagesPLMUmesh GoleNo ratings yet

- Oracle Financial AuditingT3Document171 pagesOracle Financial AuditingT3Bamidele KobaNo ratings yet