You might also like

- Finance ColgateDocument104 pagesFinance ColgatecharvitrivediNo ratings yet

- Ratio Analysis - Tata and M Amp MDocument38 pagesRatio Analysis - Tata and M Amp MNani BhupalamNo ratings yet

- NML Financial Analysis ReportDocument6 pagesNML Financial Analysis ReportBabar KhanNo ratings yet

- Comparative Financial Analysis of DaburDocument28 pagesComparative Financial Analysis of DaburManish Verma100% (2)

- Corporate Finance Paper MidDocument2 pagesCorporate Finance Paper MidAjmal KhanNo ratings yet

- Starting Fast Food Restaurant in PakistanDocument18 pagesStarting Fast Food Restaurant in Pakistanraza320% (1)

- Financial Statement AnalysisDocument1 pageFinancial Statement Analysispip_lokare35No ratings yet

- Automobile Industry Financial AnalysisDocument26 pagesAutomobile Industry Financial AnalysisSaiyd Ihtixam AehsunNo ratings yet

- Sandip Voltas ReportDocument43 pagesSandip Voltas ReportsandipNo ratings yet

- A Study On Financial Performance Analysis Ppt-MuthusamiDocument16 pagesA Study On Financial Performance Analysis Ppt-MuthusamiSwarna RavichandranNo ratings yet

- Assignment On Ratio AnalysisDocument3 pagesAssignment On Ratio AnalysisMahmudul Hasan TusharNo ratings yet

- Selected Ratios For Three Different Companies That Operate inDocument1 pageSelected Ratios For Three Different Companies That Operate indhanya1995No ratings yet

- Assignment On Financial Statement Ratio Analysis PDFDocument27 pagesAssignment On Financial Statement Ratio Analysis PDFJosine JonesNo ratings yet

- Financial Statement ANalysis of National Foods Limited Pakistan From 2005-2009Document97 pagesFinancial Statement ANalysis of National Foods Limited Pakistan From 2005-2009shahid Ali88% (8)

- DCF Valuation: Merger Is A Special Type of Capital Budgeting DecisionDocument13 pagesDCF Valuation: Merger Is A Special Type of Capital Budgeting DecisionAkhilesh Kumar100% (1)

- Ratio Analysis and Its TypesDocument9 pagesRatio Analysis and Its Typessiva_j_1No ratings yet

- Linear ProgrammingDocument27 pagesLinear ProgrammingBerkshire Hathway cold100% (1)

- Capital Structure and Leverages-ProblemsDocument7 pagesCapital Structure and Leverages-ProblemsUday GowdaNo ratings yet

- Exide Battery EFE and IFE Matrix AnalysisDocument2 pagesExide Battery EFE and IFE Matrix AnalysisRehan Mansoor100% (1)

- Inventory Management HHDocument7 pagesInventory Management HHRadhe ShyamNo ratings yet

- Cost of Capital Coleman Technologies Is Considering A Major..Document7 pagesCost of Capital Coleman Technologies Is Considering A Major..Legend WritersNo ratings yet

- Analysis of Financial StatementsDocument49 pagesAnalysis of Financial Statementsnimra farooq0% (1)

- Capital Structure Analysis of Lafarge SuDocument21 pagesCapital Structure Analysis of Lafarge SuRakibul IslamNo ratings yet

- Vertical and Horizontal AnalysisDocument32 pagesVertical and Horizontal AnalysismericarNo ratings yet

- PV Problem Set With AnswersDocument2 pagesPV Problem Set With AnswersArun S BharadwajNo ratings yet

- Tata Steel - Financial AnalysisDocument38 pagesTata Steel - Financial AnalysisCyriac Thomas69% (13)

- Britannia Industries Ltd. (India) Ratio AnalysisDocument35 pagesBritannia Industries Ltd. (India) Ratio AnalysisMansiShahNo ratings yet

- Financial Analysis of Hero CyclesDocument106 pagesFinancial Analysis of Hero CyclesD Attitude Kid50% (12)

- Financial management questionsDocument2 pagesFinancial management questionsjeganrajrajNo ratings yet

- Presentation on Marketing Mix Analysis of Sepnil Hand SanitizerDocument8 pagesPresentation on Marketing Mix Analysis of Sepnil Hand Sanitizernizam uddinNo ratings yet

- Mini CaseDocument13 pagesMini CaseVaibhav Goyal0% (1)

- Mcom BookDocument30 pagesMcom BookHarshNo ratings yet

- Coca-Cola's Market Strategy in BhubaneswarDocument35 pagesCoca-Cola's Market Strategy in BhubaneswarManas MishraNo ratings yet

- Solved Problems: OlutionDocument5 pagesSolved Problems: OlutionSavoir PenNo ratings yet

- Riphah International UniversityDocument17 pagesRiphah International UniversitySameera ZamanNo ratings yet

- Analyze Financial Health with Ratio AnalysisDocument3 pagesAnalyze Financial Health with Ratio AnalysisNeha BatraNo ratings yet

- RATIO HavellsDocument22 pagesRATIO HavellsMandeep BatraNo ratings yet

- Project Work of Accounts (055) Ratio Analysis: Submitted By-Avishkaar JainDocument30 pagesProject Work of Accounts (055) Ratio Analysis: Submitted By-Avishkaar JainAvishkaar JainNo ratings yet

- Samsung Financial Performance PresentationDocument28 pagesSamsung Financial Performance PresentationMazed100% (1)

- Nature and Significance of Capital Market ClsDocument20 pagesNature and Significance of Capital Market ClsSneha Bajpai100% (2)

- Swot Matrix ItcDocument3 pagesSwot Matrix ItcRiya PandeyNo ratings yet

- Corporate Finance Assignment Ultratech EIC AnalysisDocument19 pagesCorporate Finance Assignment Ultratech EIC AnalysisAditya Bikram SinghNo ratings yet

- Ashok LeylandDocument13 pagesAshok LeylandDiptiNo ratings yet

- Afs RatioDocument47 pagesAfs Ratiojawad100% (2)

- P2 RevisionDocument16 pagesP2 RevisionfirefxyNo ratings yet

- Analyze Customer Profitability Using BCG Matrix for Derrick's Ice CreamDocument5 pagesAnalyze Customer Profitability Using BCG Matrix for Derrick's Ice CreamAditi GuptaNo ratings yet

- Questions On LeasingDocument5 pagesQuestions On Leasingriteshsoni100% (2)

- EngroDocument73 pagesEngrogoldenguy90100% (3)

- Tata Motors:cost of CapitalDocument10 pagesTata Motors:cost of CapitalAnkit GuptaNo ratings yet

- Print Point & Yuno PackagingDocument1 pagePrint Point & Yuno PackagingAGNIK DUTTA 22100% (1)

- Haleeb Dairy Queen MilkDocument34 pagesHaleeb Dairy Queen Milkumer749100% (2)

- Capital Structure and Cost of CapitalDocument24 pagesCapital Structure and Cost of CapitalRakesh Krishnan100% (2)

- Maruti Suzuki India Ltd: A Financial Analysis PresentationDocument20 pagesMaruti Suzuki India Ltd: A Financial Analysis PresentationSushant TanejaNo ratings yet

- Welc0Me To OUR Presentation: Topic: Financial Ratios Analysis ofDocument26 pagesWelc0Me To OUR Presentation: Topic: Financial Ratios Analysis ofChoudhary OsamaNo ratings yet

- Coca-Cola Financial Ratios AnalysisDocument26 pagesCoca-Cola Financial Ratios Analysisradislamy-1No ratings yet

- Corporate Finance:: School of Economics and ManagementDocument13 pagesCorporate Finance:: School of Economics and ManagementNgouem LudovicNo ratings yet

- Ratio AnalysisDocument11 pagesRatio Analysisdanita88No ratings yet

- Financial Statement Analysis Case StudyDocument20 pagesFinancial Statement Analysis Case StudyadiscriNo ratings yet

- Why Are Ratios UsefulDocument11 pagesWhy Are Ratios UsefulKriza Sevilla Matro100% (3)

- BNL Stores' Declining ProfitabilityDocument16 pagesBNL Stores' Declining ProfitabilityAMBWANI NAREN MAHESHNo ratings yet

- Final Report On Customer Satisfaction in PIADocument19 pagesFinal Report On Customer Satisfaction in PIAWajid Ali50% (4)

- Internship Report On UBLDocument45 pagesInternship Report On UBLWajid Ali100% (1)

- Health Care Services & Government Spending in PakistanDocument6 pagesHealth Care Services & Government Spending in PakistanWajid AliNo ratings yet

- Sales Force Management in English Pharmaceutical Industries Lah ReDocument19 pagesSales Force Management in English Pharmaceutical Industries Lah ReWajid AliNo ratings yet

- Slides of Coca-Cola's Reward System in Relation To PerformanceDocument21 pagesSlides of Coca-Cola's Reward System in Relation To PerformanceWajid Ali100% (2)

- Country at A Glance "Saudi Arabia"Document1 pageCountry at A Glance "Saudi Arabia"Wajid AliNo ratings yet

- Selling in PEL Pakistan LimitedDocument43 pagesSelling in PEL Pakistan LimitedWajid AliNo ratings yet

- Coca-Cola's Reward System in Relation To PerformanceDocument17 pagesCoca-Cola's Reward System in Relation To PerformanceWajid Ali92% (12)

- Nike Case Study (Building A Global Brand Image)Document24 pagesNike Case Study (Building A Global Brand Image)Wajid Ali0% (1)

- Organizational Behavior at KFCDocument28 pagesOrganizational Behavior at KFCWajid Ali90% (10)

- Final Project of Strategic Marketing On Shell Pakistan Ltd.Document49 pagesFinal Project of Strategic Marketing On Shell Pakistan Ltd.Wajid Ali100% (1)

- WTO Vs GATT and Its Applicability in PakistanDocument6 pagesWTO Vs GATT and Its Applicability in PakistanWajid AliNo ratings yet

- Business Plan For Dairy Farm (Entrepreneurship)Document48 pagesBusiness Plan For Dairy Farm (Entrepreneurship)Wajid Ali71% (7)

- Islamic Mutual Fun Industry in PakistanDocument48 pagesIslamic Mutual Fun Industry in PakistanWajid AliNo ratings yet

- Brand Revitalization Strategies For LG Mobiles & RC Cola in PakistanDocument28 pagesBrand Revitalization Strategies For LG Mobiles & RC Cola in PakistanWajid AliNo ratings yet

- Prohibition of Interest (Riba) in Different ReligionsDocument18 pagesProhibition of Interest (Riba) in Different ReligionsWajid Ali100% (10)

- Pepsi Co. Marketing ProjectDocument17 pagesPepsi Co. Marketing ProjectWajid AliNo ratings yet

- Presentation On World Call Telecommunication Ltd. PakistanDocument94 pagesPresentation On World Call Telecommunication Ltd. PakistanWajid AliNo ratings yet

- Communication Tools of Coca ColaDocument16 pagesCommunication Tools of Coca ColaWajid Ali79% (14)

- LUX Vs DOVE Brand PositioningDocument5 pagesLUX Vs DOVE Brand PositioningWajid Ali86% (14)

- Coca-Cola BCG MatrixDocument7 pagesCoca-Cola BCG MatrixWajid Ali92% (13)

- Interesting Facts About English LanguageDocument11 pagesInteresting Facts About English LanguageWajid AliNo ratings yet

- HR Practices in Coca ColaDocument43 pagesHR Practices in Coca ColaWajid Ali91% (55)

- Secondary Association Factors of Diet CokeDocument8 pagesSecondary Association Factors of Diet CokeWajid Ali100% (5)

- Blue Whale Interesting FactsDocument16 pagesBlue Whale Interesting FactsWajid AliNo ratings yet

- Discharge of Contract, Breach and RemediesDocument21 pagesDischarge of Contract, Breach and RemediesWajid AliNo ratings yet

- A Project Report On World Call Telecommunication Limited Pakistan.Document48 pagesA Project Report On World Call Telecommunication Limited Pakistan.Wajid Ali0% (1)

- (Business Law) : Question # 1 What Is Law? and Explain The Sources of Law?Document4 pages(Business Law) : Question # 1 What Is Law? and Explain The Sources of Law?Wajid AliNo ratings yet

- Nishi Sir's Accounts-NotesDocument34 pagesNishi Sir's Accounts-Notesapi-375803189% (9)

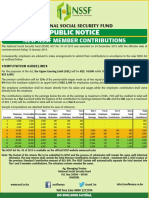

- Public Notice: New NSSF Member ContributionsDocument1 pagePublic Notice: New NSSF Member ContributionsDiana Dekatrinah KatrineNo ratings yet

- Why Students Choose ABM CoursesDocument6 pagesWhy Students Choose ABM CoursesJhas MinNo ratings yet

- TrustDocument8 pagesTrustSaravananNo ratings yet

- Integrated Strategy Optimisation for Complex Mining OperationsDocument8 pagesIntegrated Strategy Optimisation for Complex Mining OperationsCarlos A. Espinoza MNo ratings yet

- Financial ManagementDocument238 pagesFinancial ManagementJherzy Henry Elijorde FloresNo ratings yet

- ARVINDDocument1 pageARVINDSourabh YadavNo ratings yet

- Detailed Analysis of Tds For Contractor 194c by KC Singhal AdvocateDocument27 pagesDetailed Analysis of Tds For Contractor 194c by KC Singhal AdvocateAnkit SainiNo ratings yet

- PWC PreSIP Diptimaya SarangiDocument15 pagesPWC PreSIP Diptimaya SarangiChandan KumarNo ratings yet

- Article On CompensationDocument9 pagesArticle On CompensationAhmadNo ratings yet

- Investors ClinicDocument21 pagesInvestors ClinicDeepa SolankiNo ratings yet

- ITC Research ReportDocument4 pagesITC Research ReportMrRishabh97No ratings yet

- Business startup costs template analysisDocument5 pagesBusiness startup costs template analysisSANDAMARNo ratings yet

- Philippine Tax Treaty Relief ApplicationDocument2 pagesPhilippine Tax Treaty Relief ApplicationKoji ZerofourNo ratings yet

- Agile Resilient Stronger: ASOS PLC Annual Report and Accounts 2020Document63 pagesAgile Resilient Stronger: ASOS PLC Annual Report and Accounts 2020Swapna Wedding Castle EramaloorNo ratings yet

- Ch1 - What Is Strategy - Why Is It ImportantDocument37 pagesCh1 - What Is Strategy - Why Is It ImportantFrancis Jonathan F. PepitoNo ratings yet

- Financial Management Module 1Document24 pagesFinancial Management Module 1Anees SalihNo ratings yet

- McNETHS FOODS Egg Powder Business PlanDocument29 pagesMcNETHS FOODS Egg Powder Business PlanD J Ben UzeeNo ratings yet

- Travel Expenses Report: Date Description of Expenses AmountDocument3 pagesTravel Expenses Report: Date Description of Expenses AmountDenNo ratings yet

- Applying FI Mar2016Document53 pagesApplying FI Mar2016Vikas Arora100% (1)

- Asia Construction Outlook - 2014Document14 pagesAsia Construction Outlook - 2014Praveen GopalNo ratings yet

- Unit 1 - IAS 8: Accounting Policies, Changes in Accounting Estimates and Errors Class Presentation - Daniel KamothoDocument41 pagesUnit 1 - IAS 8: Accounting Policies, Changes in Accounting Estimates and Errors Class Presentation - Daniel KamothoJansher Khan DawarNo ratings yet

- JD of Sales TLDocument9 pagesJD of Sales TLChetanRaj ForeverforyouNo ratings yet

- Financial Analysis and Horizontal Analysis of Donato EnterprisesDocument3 pagesFinancial Analysis and Horizontal Analysis of Donato EnterprisesZham JavierNo ratings yet

- Ys%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaDocument28 pagesYs%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaSanaka LogesNo ratings yet

- MP2 Registration FormDocument1 pageMP2 Registration FormFrancis AjeroNo ratings yet

- Overview of Project Analysis and PhasesDocument18 pagesOverview of Project Analysis and Phasessamuel debebeNo ratings yet

- 501 CDocument20 pages501 CEn Mahaksapatalika0% (1)

- Multiplex and Single Screen Cinemas India Sample 090625070013 Phpapp01Document10 pagesMultiplex and Single Screen Cinemas India Sample 090625070013 Phpapp01iamsmartNo ratings yet

- Nestlé Audit Committee OversightDocument2 pagesNestlé Audit Committee OversightDisha ShekarNo ratings yet