You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Poka Yoke BDocument31 pagesPoka Yoke BjaymuscatNo ratings yet

- PowerPoint Do and DontsDocument25 pagesPowerPoint Do and Dontsaksh_teddyNo ratings yet

- Y-Site Drug Compatibility TableDocument6 pagesY-Site Drug Compatibility TableArvenaa SubramaniamNo ratings yet

- TG Comply With WP Hygiene Proc 270812 PDFDocument224 pagesTG Comply With WP Hygiene Proc 270812 PDFEmelita MendezNo ratings yet

- MS For The Access Control System Installation and TerminationDocument21 pagesMS For The Access Control System Installation and Terminationwaaji snapNo ratings yet

- Reporting of Counterfeit NotesDocument12 pagesReporting of Counterfeit Notesaksh_teddy100% (1)

- Cost Analysis Format-Exhaust DyeingDocument1 pageCost Analysis Format-Exhaust DyeingRezaul Karim TutulNo ratings yet

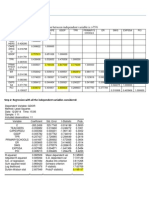

- Nagaland: Highlighted The Values Where Correlation Between Independent Variable Is 75%Document3 pagesNagaland: Highlighted The Values Where Correlation Between Independent Variable Is 75%aksh_teddyNo ratings yet

- Aam Aadmi PartyDocument2 pagesAam Aadmi Partyaksh_teddyNo ratings yet

- Starbucks Success Factors and Changing Customer Perceptions in the 1990sDocument1 pageStarbucks Success Factors and Changing Customer Perceptions in the 1990saksh_teddyNo ratings yet

- Customer ServiceDocument1 pageCustomer Serviceaksh_teddy100% (1)

- Five ForcesDocument2 pagesFive Forcesaksh_teddyNo ratings yet

- Questions For Starbucks CaseDocument1 pageQuestions For Starbucks Caseaksh_teddyNo ratings yet

- TataMotors-Mr Rakesh SharmaDocument14 pagesTataMotors-Mr Rakesh Sharmaaksh_teddyNo ratings yet

- Customer ServiceDocument1 pageCustomer Serviceaksh_teddy100% (1)

- Common Stock BasicsDocument64 pagesCommon Stock BasicsJagateeswaran KanagarajNo ratings yet

- Sugar NewDocument9 pagesSugar Newaksh_teddyNo ratings yet

- Walmart Stores Inc. Assignment: Industry Attractiveness, Competitive Advantages, and Sustainability (39 charactersDocument1 pageWalmart Stores Inc. Assignment: Industry Attractiveness, Competitive Advantages, and Sustainability (39 charactersaksh_teddyNo ratings yet

- Mobile Banking TransactionsDocument6 pagesMobile Banking Transactionsaksh_teddyNo ratings yet

- Types of Synergies: Modular, Sequential & ReciprocalDocument5 pagesTypes of Synergies: Modular, Sequential & Reciprocalaksh_teddyNo ratings yet

- How To Answer ProblemsDocument1 pageHow To Answer Problemsaksh_teddyNo ratings yet

- Case Jai Jaikumar TakeawaysDocument5 pagesCase Jai Jaikumar Takeawaysaksh_teddyNo ratings yet

- RatioanalysisDocument23 pagesRatioanalysisaksh_teddyNo ratings yet

- Reference MaterialDocument5 pagesReference MaterialRipudaman KochharNo ratings yet

- Sukh Karta DukhhartaDocument4 pagesSukh Karta Dukhhartaaksh_teddyNo ratings yet

- CV GUIDELINESDocument2 pagesCV GUIDELINESaksh_teddyNo ratings yet

- QSR Industry Growth in IndiaDocument4 pagesQSR Industry Growth in Indiaaksh_teddyNo ratings yet

- RF Interface PDocument30 pagesRF Interface Paksh_teddyNo ratings yet

- It Trends in Banking SectorDocument6 pagesIt Trends in Banking Sectoraksh_teddyNo ratings yet

- ABB Case Matrix StructureDocument20 pagesABB Case Matrix Structureaksh_teddyNo ratings yet

- Anti Ragging AffidavitDocument4 pagesAnti Ragging AffidavitsambitpgdbaNo ratings yet

- Recent Trends in The Insurance SectorDocument16 pagesRecent Trends in The Insurance SectorOladipupo Mayowa PaulNo ratings yet

- Bharti AirtelDocument1 pageBharti Airtelaksh_teddyNo ratings yet

- QuestionDocument2 pagesQuestionaksh_teddyNo ratings yet

- Apple Led Cinema Display 24inchDocument84 pagesApple Led Cinema Display 24inchSantos MichelNo ratings yet

- Service Manual: DCR-DVD150E/DVD450E/DVD650/ DVD650E/DVD850/DVD850EDocument71 pagesService Manual: DCR-DVD150E/DVD450E/DVD650/ DVD650E/DVD850/DVD850EJonathan Da SilvaNo ratings yet

- Klasifikasi Industri Perusahaan TercatatDocument39 pagesKlasifikasi Industri Perusahaan TercatatFz FuadiNo ratings yet

- Refractomax 521 Refractive Index Detector: FeaturesDocument2 pagesRefractomax 521 Refractive Index Detector: FeaturestamiaNo ratings yet

- BurhanresumeDocument1 pageBurhanresumeAbdul Rangwala0% (1)

- Ap22 FRQ World History ModernDocument13 pagesAp22 FRQ World History ModernDylan DanovNo ratings yet

- IPR GUIDE COVERS PATENTS, TRADEMARKS AND MOREDocument22 pagesIPR GUIDE COVERS PATENTS, TRADEMARKS AND MOREShaheen TajNo ratings yet

- Chapter-5-Entrepreneurial-Marketing Inoceno de Ocampo EvangelistaDocument63 pagesChapter-5-Entrepreneurial-Marketing Inoceno de Ocampo EvangelistaMelgrey InocenoNo ratings yet

- Education, A Vital Principle For Digital Library Development in IranDocument23 pagesEducation, A Vital Principle For Digital Library Development in Iranrasuli9No ratings yet

- Asset-V1 RICE+46 6 4010+2021 Q1+type@asset+block@MCQs For HO SDH New WBCS 2nd SM 2nd Class Constitution QDocument5 pagesAsset-V1 RICE+46 6 4010+2021 Q1+type@asset+block@MCQs For HO SDH New WBCS 2nd SM 2nd Class Constitution QSourin bisalNo ratings yet

- Frequently Asked Questions (And Answers) About eFPSDocument10 pagesFrequently Asked Questions (And Answers) About eFPSghingker_blopNo ratings yet

- MONETARY POLICY OBJECTIVES AND APPROACHESDocument2 pagesMONETARY POLICY OBJECTIVES AND APPROACHESMarielle Catiis100% (1)

- Schoology App Login DirectionsDocument5 pagesSchoology App Login Directionsapi-234989244No ratings yet

- E HANAAW 12 Sample QuestionDocument16 pagesE HANAAW 12 Sample QuestionsuryaNo ratings yet

- Impact of COVIDDocument29 pagesImpact of COVIDMalkOo AnjumNo ratings yet

- OspndDocument97 pagesOspndhoangdo11122002No ratings yet

- Deploy A REST API Using Serverless, Express and Node - JsDocument13 pagesDeploy A REST API Using Serverless, Express and Node - JszaninnNo ratings yet

- Folic AcidDocument5 pagesFolic Acidjyoti singhNo ratings yet

- Sonydsp v77 SM 479622 PDFDocument41 pagesSonydsp v77 SM 479622 PDFmorvetrNo ratings yet

- Air Purification Solution - TiPE Nano Photocatalyst PDFDocument2 pagesAir Purification Solution - TiPE Nano Photocatalyst PDFPedro Ortega GómezNo ratings yet

- Money and Financial InstitutionsDocument26 pagesMoney and Financial InstitutionsSorgot Ilie-Liviu100% (1)

- Siemens ProjectDocument17 pagesSiemens ProjectMayisha Alamgir100% (1)

- Pg-586-591 - Annexure 13.1 - AllEmployeesDocument7 pagesPg-586-591 - Annexure 13.1 - AllEmployeesaxomprintNo ratings yet

- Feb 21Document8 pagesFeb 21thestudentageNo ratings yet