You might also like

- Production Planning via Linear Programming Optimization for J.P. MolassesDocument15 pagesProduction Planning via Linear Programming Optimization for J.P. MolassesmarianaNo ratings yet

- Transfer PricingDocument57 pagesTransfer PricingbijoyendasNo ratings yet

- Optimizing Combustion ControlsDocument5 pagesOptimizing Combustion ControlsskluxNo ratings yet

- Strategic Managemnt SeminarDocument62 pagesStrategic Managemnt SeminarAthira AnuNo ratings yet

- Advanced Approach For Residue FCC - Residue FCC AdditivesDocument7 pagesAdvanced Approach For Residue FCC - Residue FCC Additivessaleh4060No ratings yet

- Control Emissions From Refinery FlaresDocument35 pagesControl Emissions From Refinery FlaresAli YousefNo ratings yet

- Administrative Pricing Mechanism (APM)Document14 pagesAdministrative Pricing Mechanism (APM)Amber Chourasia50% (2)

- Attock Oil RefineryDocument2 pagesAttock Oil RefineryOvais HussainNo ratings yet

- Charles Zishiri's Total Loss Control Case StudyDocument6 pagesCharles Zishiri's Total Loss Control Case StudyCalleb ZuvaNo ratings yet

- Optimisation Problems (I)Document2 pagesOptimisation Problems (I)Ahasa FarooqNo ratings yet

- The Journal of Energy and Development: "Crude Oil Market Risk Evaluations Under The Presence of The COVID-19 Pandemic,"Document22 pagesThe Journal of Energy and Development: "Crude Oil Market Risk Evaluations Under The Presence of The COVID-19 Pandemic,"The International Research Center for Energy and Economic Development (ICEED)No ratings yet

- Fuel Oil Quality Testing with API Gravity, BSW, and ColorDocument3 pagesFuel Oil Quality Testing with API Gravity, BSW, and ColorThomas KerlNo ratings yet

- Improving Fuel Quality by Whole Crude Oil HydrotreatingDocument10 pagesImproving Fuel Quality by Whole Crude Oil HydrotreatingAlexanderNo ratings yet

- EconomicsDocument62 pagesEconomicsGauravsir TradeniftyNo ratings yet

- Oil Price Elasticities and Oil Price Fluctuations: International Finance Discussion PapersDocument60 pagesOil Price Elasticities and Oil Price Fluctuations: International Finance Discussion PapersprdyumnNo ratings yet

- Performance Evaluation of Petroleum Refinery Wastewater Treatment PlantDocument6 pagesPerformance Evaluation of Petroleum Refinery Wastewater Treatment PlantInternational Journal of Science and Engineering InvestigationsNo ratings yet

- CH 2 Cost-Volume-Profit RelationshipsDocument24 pagesCH 2 Cost-Volume-Profit RelationshipsMona ElzaherNo ratings yet

- Use of PinchDocument24 pagesUse of PinchAnonymous jlLBRMAr3ONo ratings yet

- Asphatene Ppt. in Crude Oils PDFDocument19 pagesAsphatene Ppt. in Crude Oils PDFOguamahIfeanyiNo ratings yet

- AspenHYSYS YourveryfirstHYSYSSimulationDocument60 pagesAspenHYSYS YourveryfirstHYSYSSimulationkiranchemenggNo ratings yet

- Refinery and Petrochemical Processing DistillationDocument18 pagesRefinery and Petrochemical Processing Distillationrashid1986@hotmailNo ratings yet

- The Production of Biodiesel From Waste Frying Oils A Comparison of DifferentDocument7 pagesThe Production of Biodiesel From Waste Frying Oils A Comparison of DifferentmihaipvpNo ratings yet

- Density and Values of Crude Oil PDFDocument9 pagesDensity and Values of Crude Oil PDFRichard Amorin0% (1)

- FCC Fractionation For LCODocument10 pagesFCC Fractionation For LCOBehnam RahzaniNo ratings yet

- Pages From Cost Management For Engineers 01-2Document81 pagesPages From Cost Management For Engineers 01-2Lam NguyenNo ratings yet

- Multi-Objective Optimization of An Industrial Crude Distillation Unit Using The Elitist Nondominated PDFDocument13 pagesMulti-Objective Optimization of An Industrial Crude Distillation Unit Using The Elitist Nondominated PDFBahar MeschiNo ratings yet

- Talara Refinery Modernization ProjectDocument6 pagesTalara Refinery Modernization ProjectElizabeth Garcia HidalgoNo ratings yet

- BASF - New Resid FCC Technology For Maximum DistillatesDocument12 pagesBASF - New Resid FCC Technology For Maximum DistillatesedgarmerchanNo ratings yet

- The New LP: LP Modelling LP ModellingDocument5 pagesThe New LP: LP Modelling LP ModellingnanditadubeyNo ratings yet

- Troubleshooting FCC Unit Circulation and Fluidization ProblemsDocument4 pagesTroubleshooting FCC Unit Circulation and Fluidization Problemssaleh4060No ratings yet

- Hydrocarbon Storage Tank Settlement and Piping Support AnalysisDocument4 pagesHydrocarbon Storage Tank Settlement and Piping Support Analysisananyo_senguptaNo ratings yet

- 2.1-LP Formulation Examples - ExercisesDocument4 pages2.1-LP Formulation Examples - Exercisesaminzakaria89No ratings yet

- LP-Staffing & BlendingDocument15 pagesLP-Staffing & BlendingJobayer Islam TunanNo ratings yet

- Innovation For Refinery With ModellingDocument5 pagesInnovation For Refinery With ModellingJulio Adolfo López PortocarreroNo ratings yet

- Case Analysis On IOCLDocument12 pagesCase Analysis On IOCLRaoul Savio GomesNo ratings yet

- CAUSES AND MITIGATIONS OF SOOT IN THE OIL & GAS PROCESS PLANT. By: Evans Obasohan EgharevbaDocument78 pagesCAUSES AND MITIGATIONS OF SOOT IN THE OIL & GAS PROCESS PLANT. By: Evans Obasohan EgharevbaEvbaruNo ratings yet

- Critical Analysis of Petroleum Swap of Oil Giants in MaharashtraDocument8 pagesCritical Analysis of Petroleum Swap of Oil Giants in MaharashtraInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Experiment 3: Pressure Control: 3.1 Objective of The ExperimentDocument21 pagesExperiment 3: Pressure Control: 3.1 Objective of The ExperimentEdwin BautistaNo ratings yet

- Crude Oil Classification GuideDocument12 pagesCrude Oil Classification GuideRaoul ParasharNo ratings yet

- Refining Margin Supplement OMRAUG 12SEP2012Document30 pagesRefining Margin Supplement OMRAUG 12SEP2012Won JangNo ratings yet

- Refining Process (ARCHANA COMPLETE REFINING STUFF)Document96 pagesRefining Process (ARCHANA COMPLETE REFINING STUFF)Mahesh sinhaNo ratings yet

- 3-EPA Flare Activity Overview-Dickens, BrianDocument37 pages3-EPA Flare Activity Overview-Dickens, BrianAhmed MaaroofNo ratings yet

- Shrinkage Loses Resulting From Liquid Hydrocarbon BlendingDocument6 pagesShrinkage Loses Resulting From Liquid Hydrocarbon BlendingManuel AguilarNo ratings yet

- How To Leverage Market Contango and Backwardation - Futures MagazineDocument2 pagesHow To Leverage Market Contango and Backwardation - Futures Magazinethirusays29No ratings yet

- Standard Refinery Fuel TonsDocument2 pagesStandard Refinery Fuel TonsPinjala AnoopNo ratings yet

- PRPC NoteDocument61 pagesPRPC NoteRohan MehtaNo ratings yet

- Additional Delayed Coking Capacity Drivers in RefiningDocument4 pagesAdditional Delayed Coking Capacity Drivers in Refiningabhishek kumarNo ratings yet

- Linear Program 1Document52 pagesLinear Program 1ChaOs_Air75% (4)

- Applying flare monitoring to identify major flaring contributorsDocument3 pagesApplying flare monitoring to identify major flaring contributorsrvkumar61No ratings yet

- Zero Emissions Shipping FINALDocument128 pagesZero Emissions Shipping FINALpresh1989No ratings yet

- 00 Saip 13Document10 pages00 Saip 13Muhammad azeem AshrafNo ratings yet

- Benchmarking of Refinery CO2 EmissionsDocument4 pagesBenchmarking of Refinery CO2 EmissionsChKaldNo ratings yet

- SA Sugar Industry Energy ScenarioDocument6 pagesSA Sugar Industry Energy ScenarioAndy TpNo ratings yet

- Sweet Crude CompositionDocument278 pagesSweet Crude Compositionthermo_engineerNo ratings yet

- 381 HC ManagementDocument11 pages381 HC ManagementTru PinesNo ratings yet

- New Hydroprocessing Approaches Increase Petrochemical ProductionDocument11 pagesNew Hydroprocessing Approaches Increase Petrochemical ProductionnishilgeorgeNo ratings yet

- Improving refinery margins through crude selection and configuration upgradesDocument46 pagesImproving refinery margins through crude selection and configuration upgradesmujeebmehar100% (2)

- View Point: Work Overs For Production OptimizationDocument4 pagesView Point: Work Overs For Production OptimizationDaniel ChiriacNo ratings yet

- Operating and Financial LeverageDocument36 pagesOperating and Financial LeverageKiena AnthiaNo ratings yet

- Gross Profit Analysis Based On The Previous YearDocument8 pagesGross Profit Analysis Based On The Previous Yearreyzor12No ratings yet

- Carpio Morales Cases 2003Document39 pagesCarpio Morales Cases 2003miles1280No ratings yet

- Jollibee Financial AnalysisDocument4 pagesJollibee Financial Analysismiles1280No ratings yet

- Manuel Portugez vs. People Jan. 14, 2015Document7 pagesManuel Portugez vs. People Jan. 14, 2015miles1280No ratings yet

- Alex Tiongco Vbs. People Mar. 11, 2015Document5 pagesAlex Tiongco Vbs. People Mar. 11, 2015miles1280No ratings yet

- Sources of VariationDocument12 pagesSources of Variationmiles1280No ratings yet

- Civ Pro (Riano) PDFDocument110 pagesCiv Pro (Riano) PDFJude-lo Aranaydo100% (3)

- Civil Law Cases 2010-2011 (Uribe)Document988 pagesCivil Law Cases 2010-2011 (Uribe)miles1280No ratings yet

- Raza Vs DaikokuDocument1 pageRaza Vs Daikokumiles1280100% (1)

- Beralde Vs LapandayDocument4 pagesBeralde Vs Lapandaymiles1280No ratings yet

- A.M. No. 12-12-11-SC (Financial Rehabilitation Rules of Procedure)Document66 pagesA.M. No. 12-12-11-SC (Financial Rehabilitation Rules of Procedure)rocket_blue100% (5)

- The Prime Glossary - Sieve of Eratosthenes PDFDocument3 pagesThe Prime Glossary - Sieve of Eratosthenes PDFmiles1280No ratings yet

- 24 Effective Closing Tech - Brian TracyDocument30 pages24 Effective Closing Tech - Brian Tracyadi_vijNo ratings yet

- My Prayer To GodDocument1 pageMy Prayer To Godmiles1280No ratings yet

- LRA Circular No. 11-2002 - Schedule of Fess of The LRADocument16 pagesLRA Circular No. 11-2002 - Schedule of Fess of The LRAMelvin BanzonNo ratings yet

- Administrative Law ReviewerDocument73 pagesAdministrative Law ReviewerShiena Angela Aquino100% (9)

- Revised Ortega Lecture Notes IDocument132 pagesRevised Ortega Lecture Notes Imiles1280No ratings yet

- VII. CONSTITUTIONAL LAW –BILL OF RIGHTSDocument15 pagesVII. CONSTITUTIONAL LAW –BILL OF RIGHTSmiles1280No ratings yet

- The Obligations of Airlines and The Rights of PassengersDocument6 pagesThe Obligations of Airlines and The Rights of Passengersmiles1280No ratings yet

- Lecture 2 (Banking)Document108 pagesLecture 2 (Banking)miles1280100% (1)

- I. Administrative Laws: Scope of Power of Administrative AgenciesDocument8 pagesI. Administrative Laws: Scope of Power of Administrative Agenciesmiles1280No ratings yet

- Show RoomDocument1 pageShow Roommiles1280No ratings yet

- A.M. No. 12-12-11-SC (Financial Rehabilitation Rules of Procedure)Document66 pagesA.M. No. 12-12-11-SC (Financial Rehabilitation Rules of Procedure)rocket_blue100% (5)

- Barnotes 2011 PilDocument44 pagesBarnotes 2011 Pilmiles1280No ratings yet

- Legal Environment of Philiippine Business & Management ADM 220Document1 pageLegal Environment of Philiippine Business & Management ADM 220miles1280No ratings yet

- Mortimer vs. GoDocument3 pagesMortimer vs. Gomiles1280No ratings yet

- How To Fill Up The New Philippine Bir Itr For CorpDocument6 pagesHow To Fill Up The New Philippine Bir Itr For Corpmiles1280No ratings yet

- How To File Your Income Tax Return in The Philippines-COMPENSATIONDocument10 pagesHow To File Your Income Tax Return in The Philippines-COMPENSATIONmiles1280No ratings yet

- UP Bar Reviewer 2013 - TaxationDocument210 pagesUP Bar Reviewer 2013 - TaxationPJGalera89% (28)

- How To File Your Income Tax Return in The Philippines-COMPENSATIONDocument10 pagesHow To File Your Income Tax Return in The Philippines-COMPENSATIONmiles1280No ratings yet

- Mkibn20080317 0014eDocument20 pagesMkibn20080317 0014eberznikNo ratings yet

- Kunci Jawaban Soal Review InterDocument5 pagesKunci Jawaban Soal Review InterWinarto SudrajadNo ratings yet

- EconomicsDocument62 pagesEconomicsJerry WideNo ratings yet

- European Precast Concrete Factbook 2011 Final DraftDocument6 pagesEuropean Precast Concrete Factbook 2011 Final DraftKlark_KentNo ratings yet

- IRATA Training BrochoureDocument6 pagesIRATA Training BrochoureAlexandruStratilaNo ratings yet

- New Programs in The Closing OperationsDocument9 pagesNew Programs in The Closing OperationsAdriano MesadriNo ratings yet

- Drip Corp CompletoDocument36 pagesDrip Corp CompletoDaniel PerezNo ratings yet

- Turkey ImportDocument14 pagesTurkey ImportMani 1No ratings yet

- Hybrid and Derivative Securities: Learning GoalsDocument42 pagesHybrid and Derivative Securities: Learning GoalsRonna Mae Ferrer0% (1)

- CIMOS Annual Report 2010 WWWDocument150 pagesCIMOS Annual Report 2010 WWWsteelboy.indiaNo ratings yet

- The Crossings at Seigle PointDocument30 pagesThe Crossings at Seigle PointRyan SloanNo ratings yet

- Suntec REIT Achieves Record High DPU of 9.932 Cents in FY 2011Document127 pagesSuntec REIT Achieves Record High DPU of 9.932 Cents in FY 2011Nooreza PeerooNo ratings yet

- EDUCATIONAL LOANS AT SBH EdditedDocument103 pagesEDUCATIONAL LOANS AT SBH EdditedravikumarreddytNo ratings yet

- Services and PricesDocument28 pagesServices and PricesasndiasdnNo ratings yet

- IFRS 2, Share-Based Payment - DipIFR - Students - ACCA - ACCA GlobalDocument4 pagesIFRS 2, Share-Based Payment - DipIFR - Students - ACCA - ACCA GlobalayeshaNo ratings yet

- A World Divided: Understanding the Global North-South GapDocument20 pagesA World Divided: Understanding the Global North-South GapDanica AguilarNo ratings yet

- Barometer Brochure 18-09-27Document26 pagesBarometer Brochure 18-09-27ActuaLittéNo ratings yet

- Dokumenti I ODIHR Per Vezhguesit AfatshkurterDocument9 pagesDokumenti I ODIHR Per Vezhguesit Afatshkurtershqiptarja.comNo ratings yet

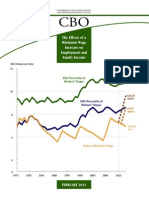

- The Effects of A Minimum-Wage Increase On Employment and Family IncomeDocument43 pagesThe Effects of A Minimum-Wage Increase On Employment and Family IncomeJeffrey DunetzNo ratings yet

- NZ Politics Daily - 4 October 2013Document244 pagesNZ Politics Daily - 4 October 2013Ben RossNo ratings yet

- Stock Market Return Expectations CalculatorDocument7 pagesStock Market Return Expectations Calculatorrocky_rocks_55No ratings yet

- Receivables Management FinalDocument33 pagesReceivables Management Finalrajesh15588No ratings yet

- POPSIS: Data PortalsDocument90 pagesPOPSIS: Data PortalsePSI PlatformNo ratings yet

- MT103 Saud Arabia 3,8MDocument2 pagesMT103 Saud Arabia 3,8Mterihinch87No ratings yet

- Commerzbank ForecastDocument16 pagesCommerzbank ForecastgordjuNo ratings yet

- Bond Price and Yield RelationshipDocument13 pagesBond Price and Yield Relationshipdscgool1232No ratings yet

- f9 02 The Financial Management EnvironmentDocument27 pagesf9 02 The Financial Management EnvironmentGAURAVNo ratings yet

- Advanced Financial Management PDFDocument6 pagesAdvanced Financial Management PDFSmag SmagNo ratings yet

- Foreign Exchange Risk ManagementDocument26 pagesForeign Exchange Risk ManagementAshwin RanaNo ratings yet

- 3.2 Treasury Procedures: Study Unit: Section: Date: SummaryDocument12 pages3.2 Treasury Procedures: Study Unit: Section: Date: SummaryAmal SultanNo ratings yet