You might also like

- 024 - Full Disclosure - Concepts and PracticesDocument22 pages024 - Full Disclosure - Concepts and PracticesgameblerxNo ratings yet

- CH 24Document22 pagesCH 24meea_nur9451No ratings yet

- Full DisclosureDocument22 pagesFull DisclosurepanjiNo ratings yet

- CH 24Document64 pagesCH 24Wahyu IsmailNo ratings yet

- Kieso 14e PowerPoint Ch24Document59 pagesKieso 14e PowerPoint Ch24James LeeNo ratings yet

- Full Disclosure in Financial Reporting: Intermediate Accounting 12th Edition Kieso, Weygandt, and WarfieldDocument23 pagesFull Disclosure in Financial Reporting: Intermediate Accounting 12th Edition Kieso, Weygandt, and WarfielddeftrisyaNo ratings yet

- C24-Financial Reporting Full DisclosureDocument10 pagesC24-Financial Reporting Full Disclosureqhn9999_359999443No ratings yet

- Chapter 1Document33 pagesChapter 1mburford2006No ratings yet

- Financial Reporting Disclosure Requirements AND Ethical ResponsibilitiesDocument44 pagesFinancial Reporting Disclosure Requirements AND Ethical ResponsibilitiesSamuel AritonangNo ratings yet

- Financial Accounting and Accounting StandardsDocument31 pagesFinancial Accounting and Accounting StandardsIrwan JanuarNo ratings yet

- Financial Reporting Requirements and DisclosuresDocument42 pagesFinancial Reporting Requirements and DisclosuresBenjamin Engel100% (1)

- CH 24Document34 pagesCH 24BryanaNo ratings yet

- Intermediate AccountingDocument18 pagesIntermediate AccountingjtopuNo ratings yet

- Other Measurement and Disclosure Issues: Tenth Canadian EditionDocument53 pagesOther Measurement and Disclosure Issues: Tenth Canadian EditionEli SaNo ratings yet

- Meet 15 - Presentation & Disclosure in FRDocument19 pagesMeet 15 - Presentation & Disclosure in FRSalma HauraNo ratings yet

- Wiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesFrom EverandWiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesNo ratings yet

- Understanding industry dynamics and financial statementsDocument13 pagesUnderstanding industry dynamics and financial statementsArsalan RafiqueNo ratings yet

- 1A An Overview of Financial StatementsDocument6 pages1A An Overview of Financial StatementsKevin ChengNo ratings yet

- Financial Statement Analysis: MGT-537 Dr. Hafiz Muhammad Ishaq 32Document77 pagesFinancial Statement Analysis: MGT-537 Dr. Hafiz Muhammad Ishaq 32gazmeerNo ratings yet

- Financial Statements and Reporting: Accounting and Capital AllocationDocument21 pagesFinancial Statements and Reporting: Accounting and Capital AllocationBJNo ratings yet

- B215 AC01 - Numbers and Words - 6th Presentation - 17apr2009Document23 pagesB215 AC01 - Numbers and Words - 6th Presentation - 17apr2009tohqinzhiNo ratings yet

- CH 24Document67 pagesCH 24najNo ratings yet

- Chapter 17Document48 pagesChapter 17ruth_erlynNo ratings yet

- Financial and Accounting Guide for Not-for-Profit OrganizationsFrom EverandFinancial and Accounting Guide for Not-for-Profit OrganizationsNo ratings yet

- Wey AP 8e Ch01Document47 pagesWey AP 8e Ch01Bintang RahmadiNo ratings yet

- LM10 Financial Reporting Quality IFT NotesDocument16 pagesLM10 Financial Reporting Quality IFT NotesjagjitbhaimbbsNo ratings yet

- ch24 PDFDocument23 pagesch24 PDFAlvandy PurnomoNo ratings yet

- Framework For Analysis and ValuationDocument44 pagesFramework For Analysis and ValuationClaudia WangNo ratings yet

- Financial Accouning and ReportingDocument5 pagesFinancial Accouning and ReportingBúp CassieNo ratings yet

- Financial Accounting and Accounting StandardDocument18 pagesFinancial Accounting and Accounting StandardZahidnsuNo ratings yet

- International Accounting StandardsDocument10 pagesInternational Accounting Standardsgotambahrani2No ratings yet

- Environment and Theoretical Structure of Financial AccountingDocument57 pagesEnvironment and Theoretical Structure of Financial AccountinghanserNo ratings yet

- F3 Concepts Conventions PoliciesDocument29 pagesF3 Concepts Conventions PoliciesShashank DharNo ratings yet

- Learning Objectives: Slide 4-1Document43 pagesLearning Objectives: Slide 4-1Jadeja OdleNo ratings yet

- Chapter 17Document41 pagesChapter 17YolandaNo ratings yet

- ICAEW Financial Accounting Conceptual and Regulatory Frame WorkDocument40 pagesICAEW Financial Accounting Conceptual and Regulatory Frame WorkhopeaccaNo ratings yet

- Chapter 1 Financial AccountingDocument47 pagesChapter 1 Financial Accountingslipns1ideNo ratings yet

- ACT100-1 - Partnership Financial ReportingDocument37 pagesACT100-1 - Partnership Financial ReportingHannah TaduranNo ratings yet

- Financial Accounting and Accounting Standards: Intermediate Accounting, 12th Edition Kieso, Weygandt, and WarfieldDocument31 pagesFinancial Accounting and Accounting Standards: Intermediate Accounting, 12th Edition Kieso, Weygandt, and WarfieldKarunia Utami100% (1)

- Analysis of Financial Statements: Presented To: Mr. YaseenDocument12 pagesAnalysis of Financial Statements: Presented To: Mr. YaseenHaris MashoodNo ratings yet

- ch01-FinAcc AccStd - KiesoDocument31 pagesch01-FinAcc AccStd - Kiesorevyahmad81No ratings yet

- Presentation and Disclosure in Financial ReportingDocument8 pagesPresentation and Disclosure in Financial ReportingIndrianaNo ratings yet

- SKILLS Financial and Corporate Reporting MODULE-IVDocument257 pagesSKILLS Financial and Corporate Reporting MODULE-IVanon_636625652100% (1)

- Unit 6 SlidesDocument37 pagesUnit 6 Slidesjoseguticast99No ratings yet

- Intro to Financial StatementsDocument30 pagesIntro to Financial StatementsWilliam ZhouNo ratings yet

- Accounting in ActionDocument62 pagesAccounting in ActionbortycanNo ratings yet

- Financial Accounting Environment and StandardsDocument38 pagesFinancial Accounting Environment and StandardsNeil StechschulteNo ratings yet

- Intermediate Accounting: Full Disclosure in Financial ReportingDocument89 pagesIntermediate Accounting: Full Disclosure in Financial ReportingJoshua KhanNo ratings yet

- Modern Auditing 7th Edition: William C. Boynton Raymond N. Johnson Walter G. KellDocument45 pagesModern Auditing 7th Edition: William C. Boynton Raymond N. Johnson Walter G. KellRizky ZulmiNo ratings yet

- IAS No.1Document10 pagesIAS No.1Hamza MahmoudNo ratings yet

- FRA - Reading 22Document23 pagesFRA - Reading 22KiraNo ratings yet

- Chapter 1 and 2Document40 pagesChapter 1 and 2kirbydegay1028No ratings yet

- Financial Reporting StandardsDocument16 pagesFinancial Reporting StandardsAhMed MahMoudNo ratings yet

- Famba 8e Test Bank Mod01 TF MC 093020 1Document16 pagesFamba 8e Test Bank Mod01 TF MC 093020 1Trisha Mae BeltranNo ratings yet

- Chapter 2 WangwDocument29 pagesChapter 2 WangwTeo Ting TingNo ratings yet

- R25 Financial Reporting Quality IFT NotesDocument20 pagesR25 Financial Reporting Quality IFT Notesmd mehmoodNo ratings yet

- Financial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsFrom EverandFinancial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsNo ratings yet

- The Comprehensive Guide on How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandThe Comprehensive Guide on How to Read a Financial Report: Wringing Vital Signs Out of the NumbersRating: 2 out of 5 stars2/5 (1)

- Wiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsFrom EverandWiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsNo ratings yet

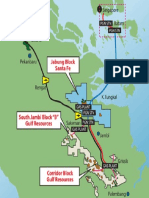

- IATMI Conference Day 1: Strategies for Achieving Indonesia's 1 Million BOPD Target by 2030Document16 pagesIATMI Conference Day 1: Strategies for Achieving Indonesia's 1 Million BOPD Target by 2030Irwan JanuarNo ratings yet

- MapillusDocument1 pageMapillusIrwan JanuarNo ratings yet

- FinancialStatement 2019Document298 pagesFinancialStatement 2019Tonga ProjectNo ratings yet

- Catalog - SS UOMODocument64 pagesCatalog - SS UOMOIrwan JanuarNo ratings yet

- Pages From Apr-Investor-PresDocument1 pagePages From Apr-Investor-PresIrwan JanuarNo ratings yet

- Country Analysis Brief: Australia: Last Updated: March 7, 2017Document24 pagesCountry Analysis Brief: Australia: Last Updated: March 7, 2017Lizeth CampoNo ratings yet

- Vdocuments - MX - Session 10 Technical Paul Davies Conocophillips PDFDocument38 pagesVdocuments - MX - Session 10 Technical Paul Davies Conocophillips PDFIrwan JanuarNo ratings yet

- Content Handbook of Energy Economic Statistics of Indonesia 2016 08989 PDFDocument70 pagesContent Handbook of Energy Economic Statistics of Indonesia 2016 08989 PDFshandyNo ratings yet

- Product Brochure DynaSlot XL Online ViewDocument6 pagesProduct Brochure DynaSlot XL Online ViewIrwan JanuarNo ratings yet

- Ipcc Wg3 Ar5 FullDocument1,454 pagesIpcc Wg3 Ar5 Fullchoonkiat.leeNo ratings yet

- Pages From 251912087-Talisman-Energy-KinabaluDocument1 pagePages From 251912087-Talisman-Energy-KinabaluIrwan JanuarNo ratings yet

- Energy Dependency and Energy Security - Role of NREDocument23 pagesEnergy Dependency and Energy Security - Role of NREIrwan JanuarNo ratings yet

- LeRoux Wavecalc (2010)Document28 pagesLeRoux Wavecalc (2010)Irwan JanuarNo ratings yet

- EnergyPoliciesofIEACountriesDenmark2017Review PDFDocument213 pagesEnergyPoliciesofIEACountriesDenmark2017Review PDFIrwan JanuarNo ratings yet

- NRE ContributionDocument74 pagesNRE ContributionIrwan JanuarNo ratings yet

- 2010 Esp Geothermal ApplicationsDocument7 pages2010 Esp Geothermal ApplicationsIrwan JanuarNo ratings yet

- Key World 2017Document97 pagesKey World 2017Kien NguyenNo ratings yet

- PT SMI's Role in Geothermal Energy Development - For Public - v2Document8 pagesPT SMI's Role in Geothermal Energy Development - For Public - v2Irwan JanuarNo ratings yet

- INAGA Ins For Geothermal Expl 201306 SlidesDocument14 pagesINAGA Ins For Geothermal Expl 201306 SlidesIrwan JanuarNo ratings yet

- INAGA Ins For Geothermal Dev Proj 201306 PaperDocument7 pagesINAGA Ins For Geothermal Dev Proj 201306 PaperIrwan JanuarNo ratings yet

- 07 Mar 2017 111739167GF5FKTEUFeasibilityStudyReportbyIITChennai PDFDocument26 pages07 Mar 2017 111739167GF5FKTEUFeasibilityStudyReportbyIITChennai PDFYbud0% (1)

- UKC CalculationDocument2 pagesUKC CalculationIrwan Januar0% (1)

- Thermo IsopentaneDocument51 pagesThermo IsopentaneIrwan JanuarNo ratings yet

- Titik Karang AsemDocument9 pagesTitik Karang AsemIrwan JanuarNo ratings yet

- UKC CalculationDocument2 pagesUKC CalculationIrwan JanuarNo ratings yet

- Force Field AnalysisDocument4 pagesForce Field AnalysisIrwan JanuarNo ratings yet

- Two Phase FlowDocument3 pagesTwo Phase FlowIrwan JanuarNo ratings yet

- Kerjasama PT Pelindo I Indonesia Dengan Port of RotterdamDocument12 pagesKerjasama PT Pelindo I Indonesia Dengan Port of RotterdamIrwan JanuarNo ratings yet

- META Model For Electricity Technology AssessmentDocument6 pagesMETA Model For Electricity Technology AssessmentIrwan JanuarNo ratings yet

- Sustainable Geothermal Power - The Life Cycle of A Geothermal PlantDocument5 pagesSustainable Geothermal Power - The Life Cycle of A Geothermal PlantIrwan JanuarNo ratings yet

- AME Invoice Line LevelDocument41 pagesAME Invoice Line LevelHimanshu MadanNo ratings yet

- Atomos Limited - Investor Presentation - Oct19 FinalDocument30 pagesAtomos Limited - Investor Presentation - Oct19 FinalMaryJane WermuthNo ratings yet

- M.H. Alshaya: An International Retail Franchise OperatorDocument4 pagesM.H. Alshaya: An International Retail Franchise OperatorSaurabh DwivediNo ratings yet

- Arrow Electronics Case Study on Distribution Partnership with Express PartsDocument25 pagesArrow Electronics Case Study on Distribution Partnership with Express PartsMuskan Soni75% (4)

- PGS Public Revalida Guide Questions For The InterviewDocument1 pagePGS Public Revalida Guide Questions For The Interviewiamaj8No ratings yet

- EMCompass Note 69 Role of AI in EMsDocument8 pagesEMCompass Note 69 Role of AI in EMsRajnish Ranjan PrasadNo ratings yet

- Uts Ab 2007Document5 pagesUts Ab 2007AhmadAdiSuhendraNo ratings yet

- History of StarbucksDocument10 pagesHistory of StarbucksSundus ButtNo ratings yet

- Trading With The RSI: Bharat Jhunjhunwala CMT, Mfta, Cfte, MstaDocument107 pagesTrading With The RSI: Bharat Jhunjhunwala CMT, Mfta, Cfte, Mstabharathkumar.smg90% (10)

- Management ConceptDocument24 pagesManagement Conceptprasad0% (1)

- ISO 20121 Presentation by Sustainable Event Alliance Australia VersionDocument21 pagesISO 20121 Presentation by Sustainable Event Alliance Australia VersionErick Leones100% (3)

- M1439-GHD-MCL-MSS-056 Lockout and Tag Out For Islolation ActivityDocument24 pagesM1439-GHD-MCL-MSS-056 Lockout and Tag Out For Islolation ActivityAnandu AshokanNo ratings yet

- Introduction to SAP Global Trade Services (GTSDocument3 pagesIntroduction to SAP Global Trade Services (GTSGuru PrasadNo ratings yet

- Template Surat Perintah LemburDocument1 pageTemplate Surat Perintah LemburchoirolisNo ratings yet

- ISO 9001 Checklist GuidanceDocument42 pagesISO 9001 Checklist GuidanceHelton75% (4)

- Nike FootwearDocument8 pagesNike FootwearMaruthi TechnologiesNo ratings yet

- CCL Pharmaceuticals (PVT.) LTD Key Performance Indicators - Product Manager 2017-18Document1 pageCCL Pharmaceuticals (PVT.) LTD Key Performance Indicators - Product Manager 2017-18Atif MajeedNo ratings yet

- Stock MarketDocument16 pagesStock MarketHades RiegoNo ratings yet

- Management Accounting (Mba002) Assignment 4Document2 pagesManagement Accounting (Mba002) Assignment 4John Michael Yu100% (1)

- Algorithmic Trading Directory 2010Document100 pagesAlgorithmic Trading Directory 201017524100% (4)

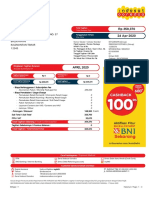

- RP 359,370 24 Apr 2020: Merlin Rahnawaty Kel. Batu Ampar Kalimantan Timur 12345 Perum Ramayana Gg. Rahayu No. 57Document3 pagesRP 359,370 24 Apr 2020: Merlin Rahnawaty Kel. Batu Ampar Kalimantan Timur 12345 Perum Ramayana Gg. Rahayu No. 57Muhammad ardanNo ratings yet

- Harvard MentorManage 10 Resources and Tools by ModuleDocument24 pagesHarvard MentorManage 10 Resources and Tools by ModulendxtradersNo ratings yet

- Case RecruitingDocument2 pagesCase RecruitingSalsabilaNo ratings yet

- The False Expectations of Michael Porter's Strategic Management Framework / Omar AktoufDocument33 pagesThe False Expectations of Michael Porter's Strategic Management Framework / Omar AktoufBiblioteca CHGMLNo ratings yet

- Year 9 Lesson Plan (Ex 2.4, 2.5)Document4 pagesYear 9 Lesson Plan (Ex 2.4, 2.5)Oliver YNo ratings yet

- Occupational Health Safety Management SystemDocument4 pagesOccupational Health Safety Management SystemSalNo ratings yet

- Zoom: An Analysis in Covid PandemicDocument2 pagesZoom: An Analysis in Covid PandemicPoda PattiNo ratings yet

- Market Factor That Affect PriceDocument18 pagesMarket Factor That Affect PriceMazharul KarimNo ratings yet

- Assignment 2 HRMN 300Document12 pagesAssignment 2 HRMN 300Sheraz HussainNo ratings yet

- Internship Report On Meezan BankDocument11 pagesInternship Report On Meezan Bankkomal mathraniNo ratings yet