You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Fashion Event Management SyllabusDocument2 pagesFashion Event Management SyllabusRitika KabraNo ratings yet

- T04 - Long-Term Construction-Type ContractsDocument11 pagesT04 - Long-Term Construction-Type Contractsjunlab0807No ratings yet

- Reconciliation of Cost and Financial Accounts PDFDocument14 pagesReconciliation of Cost and Financial Accounts PDFvihangimadu100% (2)

- Material Ledgers: Actual Costing - SAP BlogsDocument34 pagesMaterial Ledgers: Actual Costing - SAP Blogsvivaldikid0% (1)

- SupplyChain BenchmarkingDocument4 pagesSupplyChain BenchmarkingMohamad NovaldiNo ratings yet

- Burger King Strategic AnalysisDocument19 pagesBurger King Strategic AnalysisRamy Mehelba100% (3)

- Rupali Bank StatementDocument1 pageRupali Bank StatementMd YousufNo ratings yet

- CVP RelationshipDocument14 pagesCVP RelationshipSarith SagarNo ratings yet

- Porters 5 ForcesDocument10 pagesPorters 5 ForcesSarith SagarNo ratings yet

- CVP RelationshipDocument14 pagesCVP RelationshipSarith SagarNo ratings yet

- MonopolyDocument6 pagesMonopolySarith SagarNo ratings yet

- The Red-Bearded BaronDocument6 pagesThe Red-Bearded BaronSarith Sagar100% (2)

- Financial Statement Analysis Problem SetDocument7 pagesFinancial Statement Analysis Problem SetSarith SagarNo ratings yet

- Two Means TestDocument15 pagesTwo Means TestSarith SagarNo ratings yet

- DistributionDocument12 pagesDistributionSarith SagarNo ratings yet

- Accounting Primer Solutions for 4 CompaniesDocument43 pagesAccounting Primer Solutions for 4 CompaniesSarith SagarNo ratings yet

- Introduction To Cost Systems and BehaviousDocument46 pagesIntroduction To Cost Systems and BehaviousSarith SagarNo ratings yet

- Confidence Interval Estimates for Production Process Paper LengthDocument7 pagesConfidence Interval Estimates for Production Process Paper LengthSarith SagarNo ratings yet

- Confidence Interval Estimates for Production Process Paper LengthDocument7 pagesConfidence Interval Estimates for Production Process Paper LengthSarith SagarNo ratings yet

- Markov AnalysisDocument6 pagesMarkov AnalysisSarith SagarNo ratings yet

- Financial Statement Analysis Problem SetDocument7 pagesFinancial Statement Analysis Problem SetSarith SagarNo ratings yet

- CVP RelationshipDocument37 pagesCVP RelationshipSarith SagarNo ratings yet

- Broadening The Marketing ConceptDocument6 pagesBroadening The Marketing ConceptGhani ThapaNo ratings yet

- Retail Store Operations Report on Reliance Retail LtdDocument59 pagesRetail Store Operations Report on Reliance Retail LtdKadali Prasad0% (1)

- Understanding Financial Statements - A Basic OverviewDocument49 pagesUnderstanding Financial Statements - A Basic OverviewSarith SagarNo ratings yet

- What Business Are We In?: B.V.L.Narayana SPTM112-Apr-09Document11 pagesWhat Business Are We In?: B.V.L.Narayana SPTM112-Apr-09Sarith SagarNo ratings yet

- Accounting PrimerDocument21 pagesAccounting PrimerSarith SagarNo ratings yet

- Accounting Principles and ConceptsDocument14 pagesAccounting Principles and ConceptsSarith SagarNo ratings yet

- Sample Project 1Document18 pagesSample Project 1Sarith SagarNo ratings yet

- Assignment 1Document2 pagesAssignment 1Sarith SagarNo ratings yet

- Introduction and Overview of Financial SystemDocument25 pagesIntroduction and Overview of Financial SystemSarith SagarNo ratings yet

- Individual Assignment v1Document4 pagesIndividual Assignment v1Vie TrầnNo ratings yet

- Applications of Analytics to Overcome Marketing ChallengesDocument11 pagesApplications of Analytics to Overcome Marketing ChallengesJayson MercadoNo ratings yet

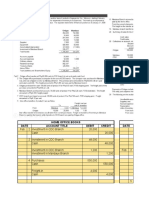

- Home Office Books Mandaue Books Date Account Title Debit Credit DateDocument27 pagesHome Office Books Mandaue Books Date Account Title Debit Credit DateVon Andrei MedinaNo ratings yet

- Multiple choice questions on product costing and manufacturing overhead allocationDocument36 pagesMultiple choice questions on product costing and manufacturing overhead allocationmikgomezNo ratings yet

- SAP CO PC Product Costing Q & ADocument14 pagesSAP CO PC Product Costing Q & AJit GhoshNo ratings yet

- InventoriesDocument3 pagesInventoriesJane TuazonNo ratings yet

- MFRS108 Kedah SDocument7 pagesMFRS108 Kedah SLENNY GRACE JOHNNIENo ratings yet

- Resume Randi Maulana Barkah q4 2021Document2 pagesResume Randi Maulana Barkah q4 2021Randi Maulana BarkahNo ratings yet

- Brand Equity On Purchase Intention Consumers' Willingness To Pay Premium Price JuiceDocument7 pagesBrand Equity On Purchase Intention Consumers' Willingness To Pay Premium Price JuiceThuraMinSweNo ratings yet

- 11 Barger PaintsDocument43 pages11 Barger PaintsKing Nitin AgnihotriNo ratings yet

- Matahari Job Vacancy Senior Merchandising Planner Head Business Development Merchandising ManagerDocument3 pagesMatahari Job Vacancy Senior Merchandising Planner Head Business Development Merchandising ManagerUuk Marginal CoastNo ratings yet

- Case Assignment 2Document5 pagesCase Assignment 2Ashish BhanotNo ratings yet

- Topic 4 PP&EDocument62 pagesTopic 4 PP&Efastidious_5100% (1)

- FAR05Document5 pagesFAR05Mitchie FaustinoNo ratings yet

- Big City Optical To Open 2 New Stores in Chicago Lakeview NeighborhoodDocument2 pagesBig City Optical To Open 2 New Stores in Chicago Lakeview NeighborhoodPR.comNo ratings yet

- Case Radiance Transaction Level PricingDocument10 pagesCase Radiance Transaction Level PricingSanya TNo ratings yet

- FIN 335 UNCW Phase III NotesDocument23 pagesFIN 335 UNCW Phase III NotesMonydit SantinoNo ratings yet

- Ma. Theresa R. TrinidadDocument3 pagesMa. Theresa R. TrinidadJoshua CalaNo ratings yet

- Principles of Accounting Chapter 12Document40 pagesPrinciples of Accounting Chapter 12myrentistoodamnhigh100% (2)

- Chandoo 07mar17Document2 pagesChandoo 07mar17Nanda CmaNo ratings yet

- Advertising - Gogi BBQDocument4 pagesAdvertising - Gogi BBQBảo TrânNo ratings yet

- SCM-310-Final Project (MHC) PDFDocument22 pagesSCM-310-Final Project (MHC) PDFMahmudul HasanNo ratings yet

- Dina Sri Hastuti 2203003 MRPDocument5 pagesDina Sri Hastuti 2203003 MRPsyaifaeza.jbgNo ratings yet