You might also like

- Process Costing Systems ExplainedDocument74 pagesProcess Costing Systems ExplainedKhairul ImamNo ratings yet

- Process Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinDocument39 pagesProcess Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinkasebNo ratings yet

- Process Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinDocument39 pagesProcess Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinFlorensia RestianNo ratings yet

- Systems Design: Process Costing: Chapter FourDocument114 pagesSystems Design: Process Costing: Chapter Fourayesha125865No ratings yet

- Ch3 Process CostingDocument4 pagesCh3 Process CostingmahendrabpatelNo ratings yet

- PROCESS COSTING SYSTEM EXPLAINEDDocument85 pagesPROCESS COSTING SYSTEM EXPLAINEDGian Carlo RamonesNo ratings yet

- Process Costing CompleteDocument84 pagesProcess Costing CompleteGian Carlo RamonesNo ratings yet

- AFAR-16 (Process Costing)Document16 pagesAFAR-16 (Process Costing)Jamaica ManilaNo ratings yet

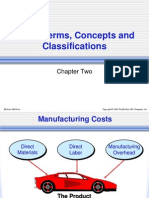

- Costs Terms, Concepts and Classifications: Chapter TwoDocument34 pagesCosts Terms, Concepts and Classifications: Chapter TwounobtainableNo ratings yet

- Miranda, Sweet (Joint Products)Document3 pagesMiranda, Sweet (Joint Products)Sweet Jenesie MirandaNo ratings yet

- Cost Accumulation For Job-Shop & Batch Production OperationsDocument60 pagesCost Accumulation For Job-Shop & Batch Production Operationstrillion5No ratings yet

- Chap 016Document24 pagesChap 016Amrik SinghNo ratings yet

- Process CostingDocument17 pagesProcess CostingKhing Dragon ManlangitNo ratings yet

- 2 Product Costing Systems Concepts and Design Issues Compatibility ModeDocument73 pages2 Product Costing Systems Concepts and Design Issues Compatibility ModeIamRuzehl VillaverNo ratings yet

- Topic 6: Job Order CostingDocument51 pagesTopic 6: Job Order CostingNa RaunaNo ratings yet

- Basic Cost Management Concepts and Accounting For Mass Customization OperationsDocument55 pagesBasic Cost Management Concepts and Accounting For Mass Customization OperationsBelajar MembacaNo ratings yet

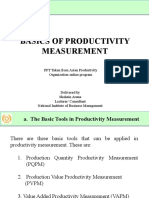

- Productivity PART 11Document36 pagesProductivity PART 11Achi ThiwankaNo ratings yet

- Costs Terms, Concepts and Classifications: Chapter TwoDocument78 pagesCosts Terms, Concepts and Classifications: Chapter TwoJesus Alberto MarquezNo ratings yet

- Rei - Process CostingDocument12 pagesRei - Process CostingSnow TurnerNo ratings yet

- Process Costing Short QuizDocument5 pagesProcess Costing Short QuizGenithon PanisalesNo ratings yet

- Chapter 4 Cost and Management AcctDocument31 pagesChapter 4 Cost and Management AcctDebebe DanielNo ratings yet

- Chapter 16 FilI-In NotesDocument10 pagesChapter 16 FilI-In Noteslowell MooreNo ratings yet

- Variable Costing: A Tool For Management: Chapter SevenDocument40 pagesVariable Costing: A Tool For Management: Chapter SevenUsman JavedNo ratings yet

- GNB 07 12eDocument40 pagesGNB 07 12eAtif SaeedNo ratings yet

- Managerial Accounting and Cost ConceptsDocument85 pagesManagerial Accounting and Cost ConceptsCatherine DelRayNo ratings yet

- Chap 004 Process CostingDocument116 pagesChap 004 Process CostingdhominicNo ratings yet

- Managerial Accounting Discussion Set 2 (Answers)Document16 pagesManagerial Accounting Discussion Set 2 (Answers)julsmlarkNo ratings yet

- Activity-Based Costing and Customer Profitability AnalysisDocument44 pagesActivity-Based Costing and Customer Profitability AnalysisKim DedicatoriaNo ratings yet

- Process Cost System: University of Santo Tomas Ust - Alfredo M. Velayo College of Accountancy SECOND TERM AY 2019-2020Document17 pagesProcess Cost System: University of Santo Tomas Ust - Alfredo M. Velayo College of Accountancy SECOND TERM AY 2019-2020allNo ratings yet

- Principles of Accounting Chapter 18Document36 pagesPrinciples of Accounting Chapter 18myrentistoodamnhighNo ratings yet

- Chapter 4Document15 pagesChapter 4Arun Kumar SatapathyNo ratings yet

- Chap 03 NotesDocument79 pagesChap 03 NotesaesculapiusNo ratings yet

- CH 17 QuizkeyDocument4 pagesCH 17 Quizkeybigk2010No ratings yet

- Managerial Accounting Concepts and Principles: Irwin/Mcgraw-HillDocument29 pagesManagerial Accounting Concepts and Principles: Irwin/Mcgraw-HillAmrik SinghNo ratings yet

- Process CostingDocument46 pagesProcess CostingRasyikah FitriaNo ratings yet

- Industrial Management IPE 481: Tanveer Hossain Bhuiyan Assistant Professor, Dept. of IPE BuetDocument63 pagesIndustrial Management IPE 481: Tanveer Hossain Bhuiyan Assistant Professor, Dept. of IPE BuetNaimul Hoque ShuvoNo ratings yet

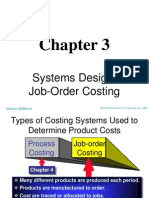

- Systems Design: Job-Order CostingDocument60 pagesSystems Design: Job-Order Costingrachim04No ratings yet

- Cost Accounting W11Document4 pagesCost Accounting W11Christine Rufher FajotaNo ratings yet

- Tutorial 3 - Process CostingDocument5 pagesTutorial 3 - Process Costingsouayeh wejdenNo ratings yet

- Analisis Biaya: Semester Gasal TA 2016 - 2017 Process CostingDocument48 pagesAnalisis Biaya: Semester Gasal TA 2016 - 2017 Process CostingMaulana HasanNo ratings yet

- Costing and Pricing L3 Process CostingDocument23 pagesCosting and Pricing L3 Process CostinglagurosangelicaNo ratings yet

- Ronald Hilton Chapter 3Document25 pagesRonald Hilton Chapter 3Swati67% (3)

- Chap 004Document56 pagesChap 004palak32100% (5)

- Systems Design: Job-Order CostingDocument25 pagesSystems Design: Job-Order CostingSafriza AhmadNo ratings yet

- 4.3 Tutorial Questions 3Document6 pages4.3 Tutorial Questions 3Lee XingNo ratings yet

- Process Cost System: Part I. Lecture and IllustrationDocument22 pagesProcess Cost System: Part I. Lecture and IllustrationMildred Angela DingalNo ratings yet

- CH 15Document29 pagesCH 15ReneeNo ratings yet

- ACCG200 Lectures 2-11 HandoutDocument108 pagesACCG200 Lectures 2-11 HandoutNikita Singh DhamiNo ratings yet

- Revision For Final ExamDocument110 pagesRevision For Final ExamWolf's RainNo ratings yet

- Garrison Lecture Chapter 4Document83 pagesGarrison Lecture Chapter 4Yen100% (1)

- NOTE CHAPTER 8 - Process CostingDocument20 pagesNOTE CHAPTER 8 - Process CostingNUR ANIS SYAMIMI BINTI MUSTAFA / UPMNo ratings yet

- BBA211 Vol7 ProcessCostingDocument11 pagesBBA211 Vol7 ProcessCostingAnisha SarahNo ratings yet

- Job Order Costing Accounting 2Document86 pagesJob Order Costing Accounting 2Faizan TafzilNo ratings yet

- Process Costing Tutorial SheetDocument3 pagesProcess Costing Tutorial Sheets_camika7534No ratings yet

- Exam Review Unit I - Chapters 1-3Document24 pagesExam Review Unit I - Chapters 1-3Aaron DownsNo ratings yet

- Topic 6 - Process Costing ADocument5 pagesTopic 6 - Process Costing AFaizah MKNo ratings yet

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesFrom EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesRating: 4.5 out of 5 stars4.5/5 (3)

- Practical Guide To Production Planning & Control [Revised Edition]From EverandPractical Guide To Production Planning & Control [Revised Edition]Rating: 1 out of 5 stars1/5 (1)

- 15 Technical Catalog Casting Steel eDocument52 pages15 Technical Catalog Casting Steel elbo330% (1)

- Buffoli Booklet - USA PhoscoatingDocument138 pagesBuffoli Booklet - USA PhoscoatingMark GarrettNo ratings yet

- Naveen Jose - Resume PDFDocument2 pagesNaveen Jose - Resume PDFmansih457No ratings yet

- ESC General Catalogue 2017 2018 1st EditionDocument82 pagesESC General Catalogue 2017 2018 1st EditionArief Rachman0% (1)

- PT Montis Energy Welding Procedure SpecificationDocument4 pagesPT Montis Energy Welding Procedure SpecificationMuhammad Fitransyah Syamsuar PutraNo ratings yet

- Machine Tools Lab Manual (13-14)Document39 pagesMachine Tools Lab Manual (13-14)Krishna Murthy100% (1)

- Frontier School Division Job Safety Analysis for Milling Machine OperationsDocument5 pagesFrontier School Division Job Safety Analysis for Milling Machine OperationsAshok SureshNo ratings yet

- 110 Series Ordering GuideDocument4 pages110 Series Ordering GuideElectromateNo ratings yet

- An Overview of Pakistan Pharma IndustryDocument2 pagesAn Overview of Pakistan Pharma IndustryAnam ShoaibNo ratings yet

- Ashish NBC ReportDocument14 pagesAshish NBC ReportBidurGujjarNo ratings yet

- Corrosion Prevent at Ion TechnologyDocument12 pagesCorrosion Prevent at Ion TechnologyandraspappNo ratings yet

- Government of India Ministry of Railways: Infrastructure Requirements For Manufacturing, Testing & Supply ofDocument3 pagesGovernment of India Ministry of Railways: Infrastructure Requirements For Manufacturing, Testing & Supply ofkapilparyaniNo ratings yet

- Bidriware JayuDocument3 pagesBidriware JayuAnupurvi JainNo ratings yet

- SojitzDocument8 pagesSojitzPratik GuptaNo ratings yet

- Quality Control - Wikipedia, The Free EncyclopediaDocument3 pagesQuality Control - Wikipedia, The Free EncyclopediaBaguma Grace GariyoNo ratings yet

- ANEXO 5 - Catalogo Sumideros JR Smith PDFDocument22 pagesANEXO 5 - Catalogo Sumideros JR Smith PDFCamilo VelásquezNo ratings yet

- Simufact - Professional Forming SimulationDocument12 pagesSimufact - Professional Forming SimulationMrLanternNo ratings yet

- Corrosion Protection of the 21st CenturyDocument14 pagesCorrosion Protection of the 21st CenturylymacsausarangNo ratings yet

- Chemtech Pharmacon - Engineering ServicesDocument2 pagesChemtech Pharmacon - Engineering ServicesDilip KatekarNo ratings yet

- AssignmentDocument3 pagesAssignmentAviral Sansi0% (1)

- Introduction To The Industry: Indian Oil Corporation Limited, or Indianoil, Is An Indian StateDocument4 pagesIntroduction To The Industry: Indian Oil Corporation Limited, or Indianoil, Is An Indian StateAbhishek GuptaNo ratings yet

- Chemical Engineering Process Design: Mody and Marchildon: Formation and Processing of SolidsDocument5 pagesChemical Engineering Process Design: Mody and Marchildon: Formation and Processing of SolidsHarshaNo ratings yet

- Plastics For Orthotics and ProstheticsDocument4 pagesPlastics For Orthotics and ProstheticslarjcaNo ratings yet

- BASF - BR PUE Catalysts AnsichtDocument20 pagesBASF - BR PUE Catalysts Ansichtvasucristal0% (2)

- Brochure SuperSettlerDocument8 pagesBrochure SuperSettlerJesús RiberaNo ratings yet

- Madura CoatsDocument53 pagesMadura CoatsGanga Dharan100% (5)

- Shell Gadus S5 T460:: Shell Stamina Grease HDSDocument2 pagesShell Gadus S5 T460:: Shell Stamina Grease HDSPablo Soler SalazarNo ratings yet

- Fundermax Exterior Technic 2011gb WebDocument88 pagesFundermax Exterior Technic 2011gb WebarchpavlovicNo ratings yet

- Packaging Logistics Design PDFDocument8 pagesPackaging Logistics Design PDFShamsulfahmi ShamsudinNo ratings yet

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-2-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)