You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Brand Awareness of AirtelDocument13 pagesBrand Awareness of AirtelShraddha SharmaNo ratings yet

- Final Zayredin AssignmentDocument26 pagesFinal Zayredin AssignmentAmanuelNo ratings yet

- Group 6 Environmental ScanningDocument9 pagesGroup 6 Environmental Scanningriza may torreonNo ratings yet

- A Review On Julie's Manufactring SDN BHD - Chika OgbuehiDocument8 pagesA Review On Julie's Manufactring SDN BHD - Chika OgbuehiChika100% (2)

- International Parity Relationship: Topic 4Document32 pagesInternational Parity Relationship: Topic 4sittmoNo ratings yet

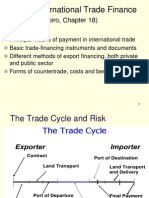

- Topic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)Document15 pagesTopic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)sittmoNo ratings yet

- AFC3240 Topic 01 S2 2010Document18 pagesAFC3240 Topic 01 S2 2010sittmoNo ratings yet

- AFC3240 Topic 08 S1 2011Document24 pagesAFC3240 Topic 08 S1 2011sittmoNo ratings yet

- Topic Determination of Exchange Rate: Balance of Payments (BOP)Document27 pagesTopic Determination of Exchange Rate: Balance of Payments (BOP)sittmoNo ratings yet

- Sec 04Document32 pagesSec 04sittmoNo ratings yet

- Section 2 Section 2 Intervention in Markets Intervention in MarketsDocument18 pagesSection 2 Section 2 Intervention in Markets Intervention in MarketssittmoNo ratings yet

- Solving Inhomogenous Recurrence RelationsDocument3 pagesSolving Inhomogenous Recurrence Relationssittmo0% (1)

- Solving Inhomogenous Recurrence Relations 2Document2 pagesSolving Inhomogenous Recurrence Relations 2sittmoNo ratings yet

- XYZ Investing INC. Trial BalanceDocument3 pagesXYZ Investing INC. Trial BalanceLeika Gay Soriano OlarteNo ratings yet

- Org. and ManagementDocument3 pagesOrg. and Managementvirginia taguiba0% (1)

- Types of Maintenance and Their Characteristics: Activity 2Document7 pagesTypes of Maintenance and Their Characteristics: Activity 2MusuleNo ratings yet

- Course Outline Vendor Selection and Development NewDocument10 pagesCourse Outline Vendor Selection and Development Newmajid aliNo ratings yet

- Peel Mining LTD Investor SheetDocument2 pagesPeel Mining LTD Investor SheetkaiselkNo ratings yet

- Section 2 Theories Chapter 20Document53 pagesSection 2 Theories Chapter 20Sadile May KayeNo ratings yet

- Chapter 3 InventoryDocument13 pagesChapter 3 Inventorypapajesus papaNo ratings yet

- Business Opportunity EvaluationDocument26 pagesBusiness Opportunity EvaluationAmirNo ratings yet

- Application of Information Technology in Insurance SectorDocument2 pagesApplication of Information Technology in Insurance Sectorjauharansari3No ratings yet

- Tesco 14 FullDocument4 pagesTesco 14 FullBilal SolangiNo ratings yet

- Ey Cafta Case Championship 2022 Chapter 2Document17 pagesEy Cafta Case Championship 2022 Chapter 2Wavare YashNo ratings yet

- Bangalore JustDial & OthersDocument56 pagesBangalore JustDial & OthersAbhishek SinghNo ratings yet

- Audit 2, PENSION-EQUITY-INVESTMENT-LONG-QUIZDocument3 pagesAudit 2, PENSION-EQUITY-INVESTMENT-LONG-QUIZShaz NagaNo ratings yet

- Blockholder Trading, Market E Ciency, and Managerial MyopiaDocument35 pagesBlockholder Trading, Market E Ciency, and Managerial MyopiamkatsotisNo ratings yet

- Subject: Welcome To Hero Fincorp Family Reference Your Used Car Loan Account No. Deo0Uc00100006379290Document4 pagesSubject: Welcome To Hero Fincorp Family Reference Your Used Car Loan Account No. Deo0Uc00100006379290Rimpa SenapatiNo ratings yet

- Working Capital Ultra Tech CementDocument91 pagesWorking Capital Ultra Tech CementGnaneswari GvlNo ratings yet

- Quiz Stocks and Their ValuationDocument3 pagesQuiz Stocks and Their ValuationBilly Vince AlquinoNo ratings yet

- Prowessiq Data Dictionary PDFDocument5,313 pagesProwessiq Data Dictionary PDFUtkarsh SinhaNo ratings yet

- Future and Option MarketDocument21 pagesFuture and Option MarketKunal MalodeNo ratings yet

- Aon Profile 2020Document16 pagesAon Profile 2020phanapa100% (1)

- A Balanced Scorecard For Small BusinessDocument8 pagesA Balanced Scorecard For Small BusinessmoussumiiNo ratings yet

- Report On Askari BankDocument64 pagesReport On Askari Bankzorish87% (15)

- Comparison of Consumer BehaviorDocument15 pagesComparison of Consumer BehaviorSubhayu MajumdarNo ratings yet

- Activiity 2 Investment in AssociateDocument3 pagesActiviity 2 Investment in AssociateAldrin Cabangbang67% (3)

- AISAN CanopyDocument46 pagesAISAN CanopyAmirul AdamNo ratings yet

- Chapter 1 EnterprDocument11 pagesChapter 1 EnterprSundas FareedNo ratings yet